- Supramax rates soften on Paradip-Qingdao route on limited enquiries

- Strong Australia-China demand offsets weak Atlantic activity

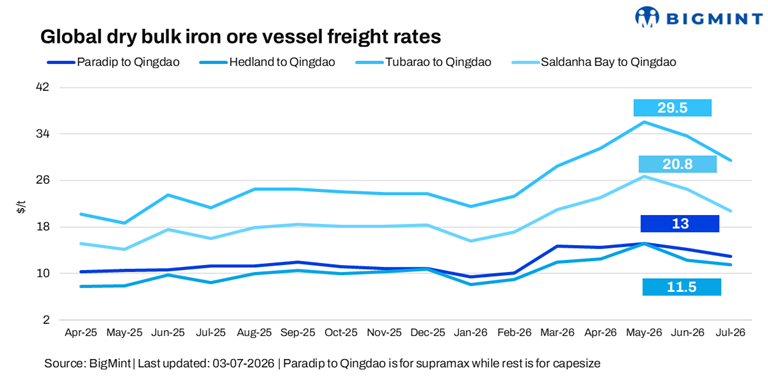

Dry bulk iron ore freight sentiment remained under pressure in the week ended 3 July. Supramax rates softened on the Paradip-Qingdao route amid limited cargo enquiries, subdued chartering activity, and fixtures concluded at lower levels.

Ample vessel availability and muted demand for minor bulks kept freight rates under pressure, while market participants largely adopted a wait-and-watch approach due to uncertain cargo flows.

Capesize freight sentiment remained mixed during the week. Freight rates on the Australia-China route were largely stable w-o-w as stronger iron ore cargo enquiries and improved charterer bids supported the Pacific market.

In contrast, the Tubarao-Qingdao and Saldanha Bay-Qingdao routes softened w-o-w due to wider bid-offer spreads, cautious fixture negotiations, and limited cargo demand, despite steady iron ore export volumes.

Overall, the market remained underpinned by healthy Australia and Brazil iron ore shipments, although selective buying by Chinese steel mills continued to cap freight upside.

Route-wise update

Factors influencing freight rates

- Baltic Dry Index (BDI) records weekly recovery: The BDI advanced 2.3% (59 points) w-o-w to 2,650 on 2 July, as firmer iron ore fixtures improved overall dry bulk sentiment. Nevertheless, the Capesize index remained 2.5% (94 points) lower w-o-w at 3,921, while the Supramax segment slipped 0.2% (3 points) to 1,675, reflecting relatively soft activity in the minor bulk market.

- Bunker prices decline w-o-w: Bunker prices fell by $52/tonne (t) w-o-w to $661/t as of 3 July, reflecting weaker crude oil prices and easing fuel market sentiment, providing cost support to vessel operators.

- Brent crude futures drop w-o-w: Brent crude oil (September 2026 contract) declined by $1.04/barrel (bbl) w-o-w to $72.78/bbl on 3 July, pressured by expectations of ample global supply and softer demand outlook, which weighed on energy markets.

- DCE iron ore futures retreat w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) dropped RMB 14/t w-o-w to RMB 734/t ($108/t) on 3 July, as cautious Chinese steel mill procurement and comfortable supply expectations continued to pressure market sentiment.

Outlook

The dry bulk iron ore freight market is expected to maintain a positive trend in the near term, driven by improving Capesize fundamentals, healthy seaborne iron ore exports, and stronger chartering activity on the key Australia-China route. While Atlantic activity is likely to remain mixed, cautious Chinese steel mill procurement and balanced fleet availability may prevent a sharp rally in rates.

Leave a Reply