- Italian steel slowdown pressures European scrap consumption

- Strong US mill utilisation limits domestic price declines

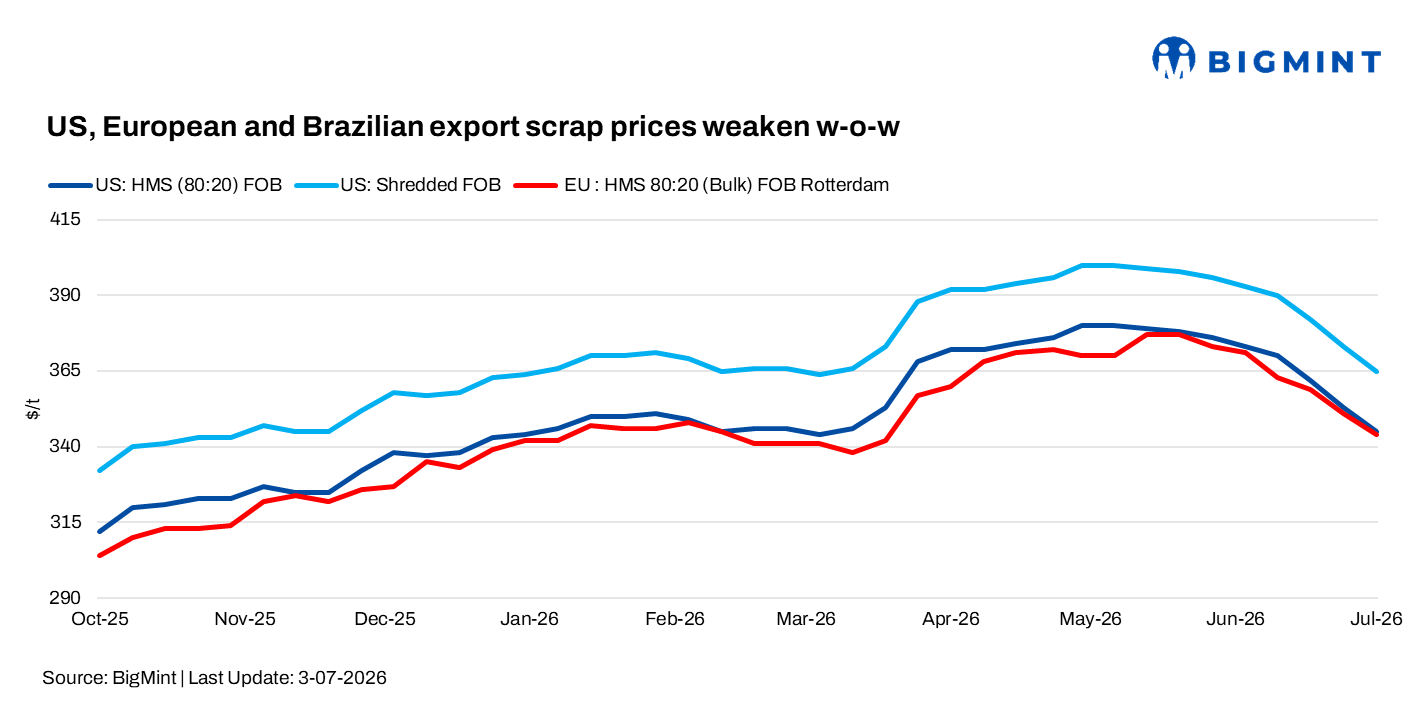

Global ferrous export scrap markets showed mixed trends during the week, with prices remaining broadly stable in the US and Brazil, while European markets continued to face downward pressure from weak export demand and softer Turkish import prices.

Strong domestic steel production and high mill operating rates supported the US market, whereas Brazil’s domestic prices held steady despite expectations of mill purchase price cuts. In contrast, weakening Turkish demand and slower steel production weighed on sentiment across the UK and mainland Europe, keeping the near-term outlook cautious.

US

In US domestic market, busheling held at $460-465/t DAP, shredded scrap at $430-435/t, plate and structural scrap at $405/t, and HMS 80:20 at $375/t DAP. Market participants expect mostly rollover settlements, although busheling could see a slight increase if high-grade scrap supply tightens.

Some Ohio Valley mills reportedly received nearly 20% less scrap than ordered in June, while logistical constraints also supported demand. Export sentiment remained weak, with Turkish HMS 80:20 falling to $380/t CFR. Meanwhile, FOB US East Coast export prices continued to soften, with shredded scrap assessed at $365/t and HMS at $345/t amid weak overseas demand.

The US ferrous scrap market is expected to remain largely stable in July, supported by strong domestic steel production and mill operating rates above 80%, despite continued weakness in export markets.

Europe

The UK export scrap market remained under pressure in early July as weak buying interest from Turkiye and Asia continued to weigh on export sentiment. Reflecting softer export demand, UK dockside prices have declined sharply since mid-June. Purchase prices for HMS 80:20 scrap fell by GBP 20-25/t ($27-33/t) to GBP 200-210/t ($266-279/t) DAP. Market participants expect prices to remain under pressure, with some anticipating a further correction of around GBP 10/t if export demand fails to improve.

Baltic dockside HMS 80:20 prices also declined by around EUR 5/t ($6/t) to EUR 375/t ($429/t), reflecting subdued overseas buying. Market participants said further corrections are possible if demand from key import markets remains weak.

Across mainland Europe, domestic scrap prices remained broadly stable in June, supported by balanced supply and demand. E3 (HMS 80:20) traded at EUR 330-340/t ($376-388/t) DAP, E8 (Shredded) at EUR 350-355/t ($399-405/t) DAP, and E40 (PNS) at EUR 350-360/t ($399-410/t) DAP.

However, market sentiment has weakened heading into July following a $20-30/t decline in Turkish imported scrap prices since early June. Lower steel production in Italy during the summer is also expected to curb scrap consumption, adding further downward pressure to European scrap prices.

Brazil

Brazil’s ferrous scrap market remained largely stable during the week despite expectations that mills will reduce domestic scrap purchase prices by BRL 80-100/t ($15-19/t) amid weak rebar demand and sluggish steel sales. Market participants expect further price direction to depend on pig iron values.

HMS 80:20 at BRL 925-930/t ($178-179/t) FOT, turnings at BRL 825-830/t ($159-160/t) FOT, and clean steel scrap at BRL 1,005-1010/t ($193-194/t) FOT, all unchanged. Export prices also held steady, with HMS 80:20 at $300/t FOB and shredded scrap at $320/t FOB, following a $5/t decline earlier in June due to weak overseas demand.

Leave a Reply