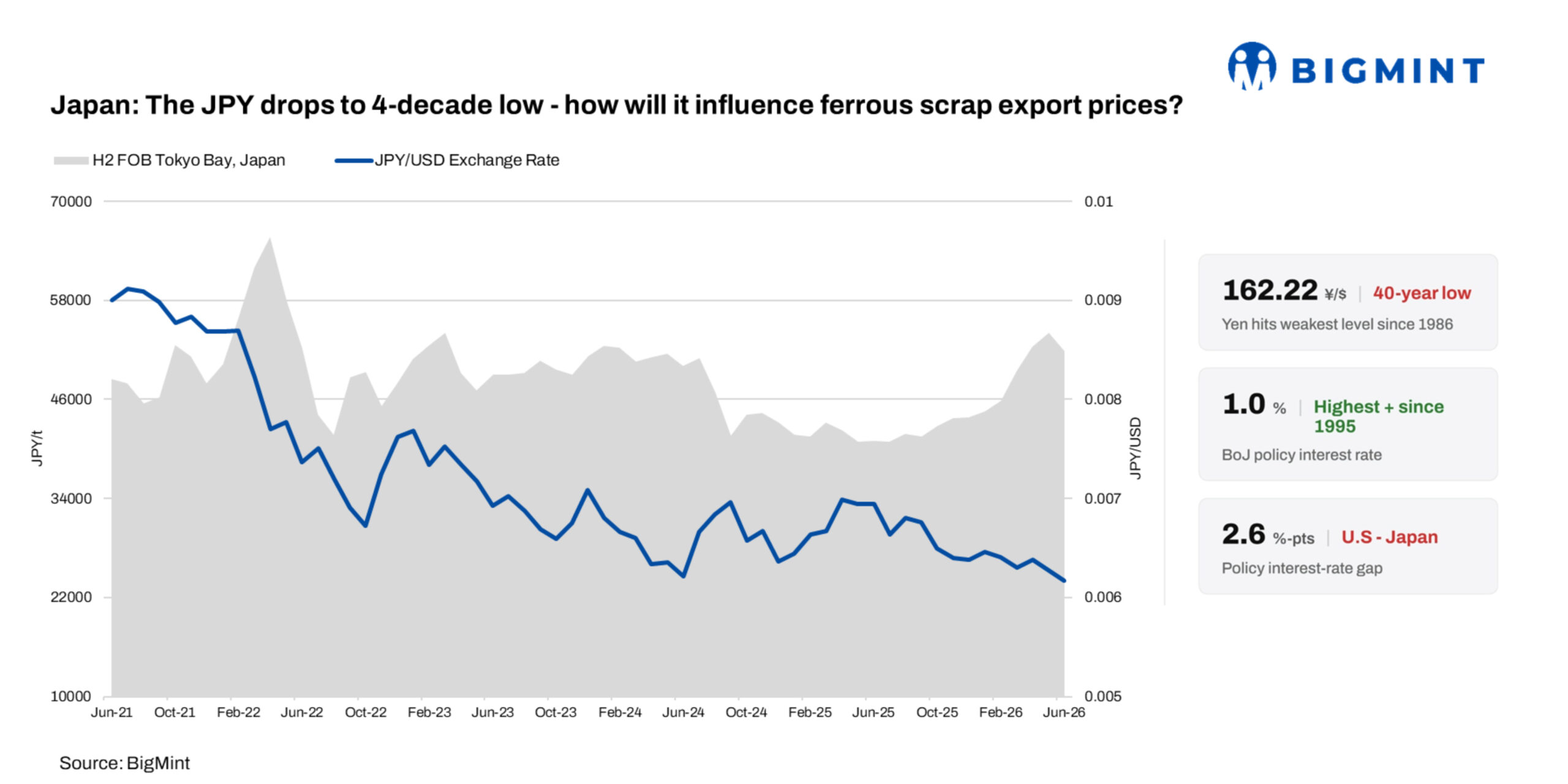

- JPY falls to its weakest level since 1986, improving exporters’ pricing flexibility

- Domestic mill procurement remains biggest determinant of scrap export prices

The Japanese yen has weakened beyond JPY 162 per US dollar, its lowest level since 1986, renewing expectations that Japanese ferrous scrap could become increasingly competitive across Asian import markets. Conventional market wisdom suggests a weaker currency should translate into lower dollar-denominated FOB offers and stronger exports. However, BigMint’s analysis indicates that the relationship is far more nuanced.

While a weaker yen improves exporters’ margins by increasing the local currency value of dollar-denominated sales, domestic scrap procurement costs and regional supply-demand fundamentals remain the primary drivers of Japanese FOB prices. Rather than triggering lower export offers, the weaker currency has mainly strengthened Japan’s export competitiveness while allowing suppliers to maintain firm FOB levels.

Why has the yen remained under pressure?

The yen’s depreciation reflects the widening monetary policy gap between Japan and the US. Although the Bank of Japan has raised its benchmark interest rate to 1%, higher US interest rates, resilient economic growth, elevated energy costs and continued carry-trade activity have kept demand firmly in favour of the US dollar.

Despite spending around JPY 11.7 trillion to support the currency during April-May, Japanese authorities have been unable to reverse the broader weakening trend. For scrap exporters, this improves pricing flexibility, but domestic procurement costs –not exchange rates– continue to determine export prices.

Currency improves competitiveness

A weaker yen improves the competitiveness of Japanese scrap exports by increasing the amount of yen exporters receive from every dollar-denominated sale. In theory, this gives suppliers room to reduce FOB offers while preserving domestic margins.

However, export prices are not determined by currency movements alone. Japanese exporters first procure scrap from domestic suppliers and mills, making local procurement prices the primary cost benchmark. When domestic scrap prices rise, exporters must increase FOB offers to protect margins, regardless of exchange-rate gains.

This trend has been evident in recent months. Although the yen weakened from around JPY 155/$ to above JPY 162/$ during early 2026, domestic H2 procurement prices climbed from approximately JPY 44,000/t to more than JPY 51,000/t. Consequently, BigMint’s H2 FOB Tokyo Bay assessment increased from around $280/t to above $315/t, rather than declining.

Regional demand has also played an important role. Strong buying interest from Vietnam, Bangladesh and Indonesia, coupled with tighter availability of obsolete scrap, allowed exporters to retain the additional currency benefit instead of passing it on through lower FOB prices.

According to a representative of a Japan-based trading company, “A weaker yen is definitely supportive for Japanese scrap exports. Exporters get more yen for every dollar earned, giving them greater flexibility on FOB offers when required. However, domestic mill buying remains the biggest pricing driver. If mills continue raising scrap purchase prices or export demand strengthens, FOB offers are unlikely to decline significantly despite the weaker currency. Any intervention by the Bank of Japan or Japanese authorities that strengthens the yen could quickly erode this export advantage. So, while the weaker yen supports exports, it is far from being the only driver of Japanese scrap pricing.”

Japan’s steel slowdown is creating structural scrap surplus

The larger structural driver behind Japan’s growing export presence is the continued contraction in domestic steel production rather than the depreciation of the yen.

Japan’s crude steel production declined 4% y-o-y to around 81 mnt in CY’25, marking the fourth consecutive annual decline and the country’s lowest output since 1968. During the same period, scrap consumption fell to 29.7 mnt, while scrap generation eased more gradually to 37.1 mnt.

Because domestic scrap consumption declined faster than generation, a structural exportable surplus emerged.

The decline reflects persistent labour shortages, subdued construction activity, elevated energy costs and the gradual relocation of manufacturing capacity overseas. Production across almost every steel segment weakened during 2025, with BOF steel output declining 3.4% y-o-y, EAF steel production falling 5.5%, plate output dropping 4.5% and sections and bars declining 5%. These structural challenges continue to suppress domestic steel demand while leaving scrap availability relatively stable.

The result has been a gradual shift in Japan’s scrap market from domestic consumption towards export-oriented trade.

Regional trade flows reshaping export market

Japan’s changing domestic fundamentals have been clearly reflected in regional trade flows.

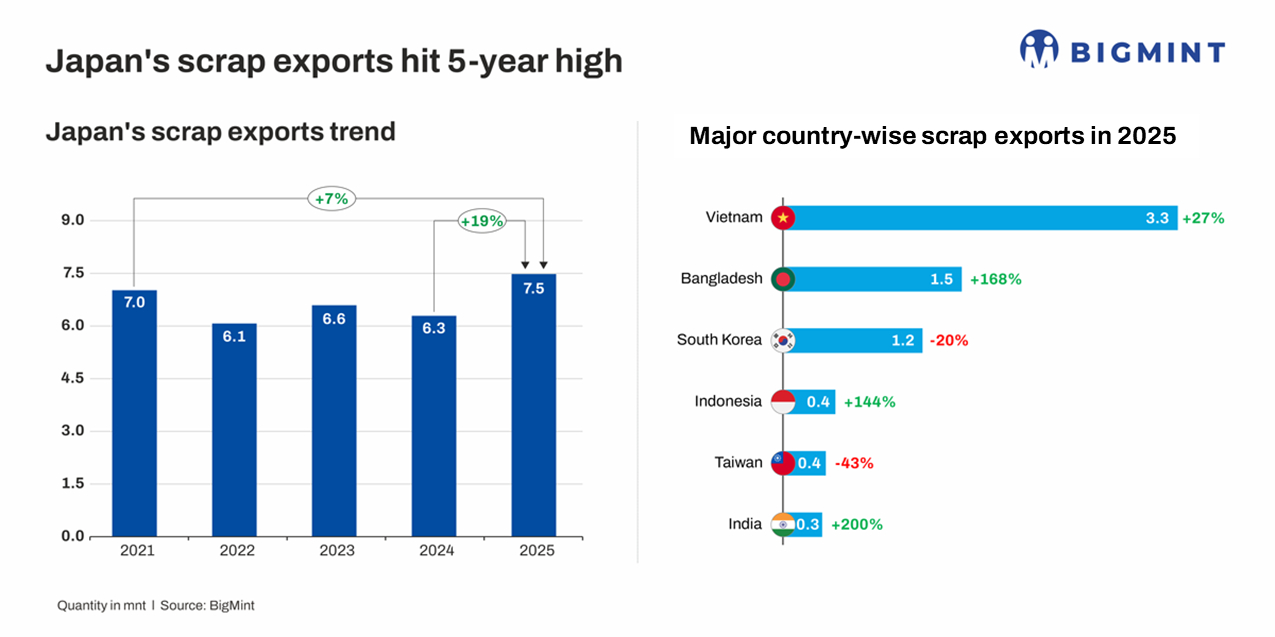

Ferrous scrap exports increased 19% year on year to 7.5 mnt in CY’25, the highest level in five years. Vietnam remained the largest destination, while Bangladesh overtook South Korea and Taiwan to become the second-largest importer as expanding electric arc furnace capacity, favourable freight economics and consistent cargo availability encouraged stronger buying.

Meanwhile, imports by South Korea and Taiwan weakened amid softer steel demand, elevated inventories and growing competition from cheaper Chinese steel.

Market participants believe the weaker yen has strengthened Japan’s competitiveness but has not fundamentally altered export behaviour.

A Singapore-based trading company told BigMint: “Japan’s mills generally retain higher-quality scrap for domestic consumption, while lower grades continue to be exported. Those export flows are unlikely to change significantly because of the exchange rate alone.”

Can weaker yen sustain Japan’s export advantage?

The weaker yen is expected to remain supportive for Japanese scrap exports by improving exporters’ pricing flexibility and reinforcing competitiveness against suppliers from Europe and North America. However, its influence on export prices is likely to remain secondary to domestic procurement trends.

Looking ahead, Japan is expected to remain one of Asia’s most reliable ferrous scrap suppliers as domestic steel production remains subdued and surplus scrap continues flowing into export markets. Demand from Vietnam, Bangladesh and Indonesia is expected to provide the principal support for exports, while the availability of high-quality H2 and shredded grades is likely to remain relatively tight.

The main uncertainty lies in policy intervention. Japanese authorities have already spent approximately JPY 11.7 trillion intervening in currency markets during April and May. Any sustained appreciation of the yen could narrow exporters’ pricing flexibility, although it is unlikely to alter the structural surplus underpinning Japan’s export market.

The weak yen has undoubtedly strengthened Japan’s export competitiveness, but it should be viewed as a pricing advantage rather than the primary driver of the scrap market. The evidence suggests that export prices remain anchored by domestic mill procurement, while the sustained increase in shipments reflects a structural surplus created by four consecutive years of declining crude steel production and weaker domestic scrap consumption.

For buyers across Asia, the more important indicators are domestic procurement prices, scrap generation, crude steel output and demand from Southeast Asia–not simply the USD/JPY exchange rate. As long as these structural fundamentals remain unchanged, Japan is likely to retain its position as one of the region’s most competitive and reliable ferrous scrap suppliers, regardless of short-term currency volatility.

Leave a Reply