- Iron ore supply surplus expected to widen further

- China summer slowdown weakens iron ore demand

Mysteel Global: Global iron ore shipments are entering their traditional peak season this month, while China’s steel consumption is expected to gradually weaken due to the summer lull, weighing on iron ore demand. As a result, a potential supply glut, combined with lower freight rates driven by a likely retreat in oil prices, could depress China’s imported iron ore prices in June, Mysteel predicts in its latest monthly report on the commodity.

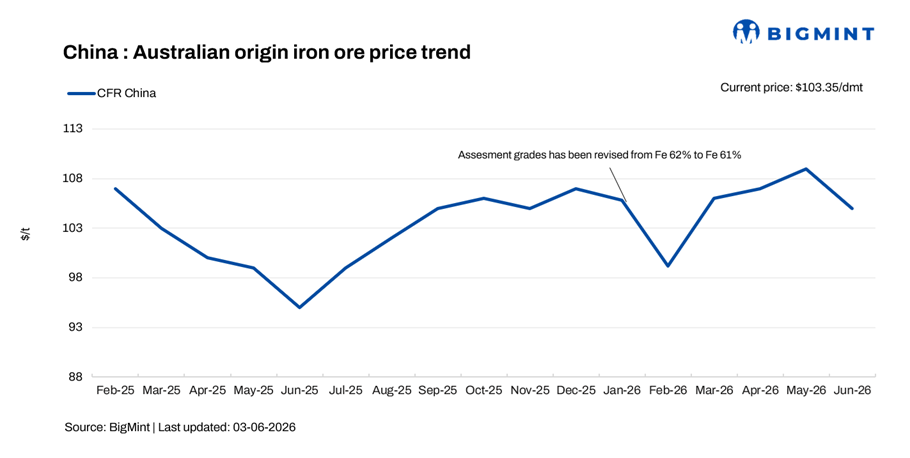

Although iron ore prices pulled back in the second half of May after a strong increase earlier in the month, the monthly average ended higher overall. For example, Mysteel assessed the SEADEX 62% Australian Fines at an average of $110.2/dmt CFR Qingdao in May, up $1.4/dmt from April’s average of $108.8/dmt.

The support for iron ore prices in recent months is mainly attributed to the ongoing geopolitical crisis in the Middle East, as elevated oil prices have kept freight rates high.

However, the upcoming peak shipping season for iron ore has raised concerns about oversupply in June, the report notes.

Australian miners are expected to significantly ramp up shipments this month to meet mid-year or fiscal year-end targets. Meanwhile, June also marks a seasonal high for Brazilian iron ore exports, as disruptions from the rainy season have fully subsided.

Global iron ore shipments totaled 146.94 million tonnes in May, up 10.43 million tonnes or 7.6% on month, according to Mysteel’s tracking. Shipments in June could rise by a further 5 million tonnes, it estimates.

On the demand side however, iron ore lacks sufficient momentum to bolster prices, as mill production is expected to peak soon. China’s steel consumption typically weakens in summer, when outdoor construction activities are hampered by high temperatures and frequent rains, the report explains.

The 247 Chinese blast-furnace steelmakers Mysteel regularly checks produced an average of 2.41 million tonnes/day of during May 22-28, 0.38% lower than during the same period last year, according to the latest data.

Mysteel expects the average daily output of these mills to top out at around 2.42 million t/d sometime this month. In comparison, last year’s peak was achieved earlier in May and at a higher level of 2.46 million t/d.

A growing iron ore supply surplus means that sustained blast furnace activity will provide only limited price support for the raw material, the report argues. Furthermore, a likely decline in freight rates is expected to add to the downward pressure on prices, it adds.

Freight rates are generally expected to decline from mid-June onward as the shipping season winds down. In fact, they have already pulled back from multi-year highs recently, amid signs of easing US-Iran hostilities and falling oil prices.

If freight rates and mining production costs continue to drop alongside oil prices, iron ore prices could face more downside risks, the report warns. Mysteel expects the SEADEX 62% Australian Fines index to trade within a lower range of $95-107/dmt in June, in comparison to a range of $106.5-113.6/dmt in May.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply