- HZL zinc prices remain slightly above domestic spot market levels

- Trade remains need-based despite supportive global fundamentals

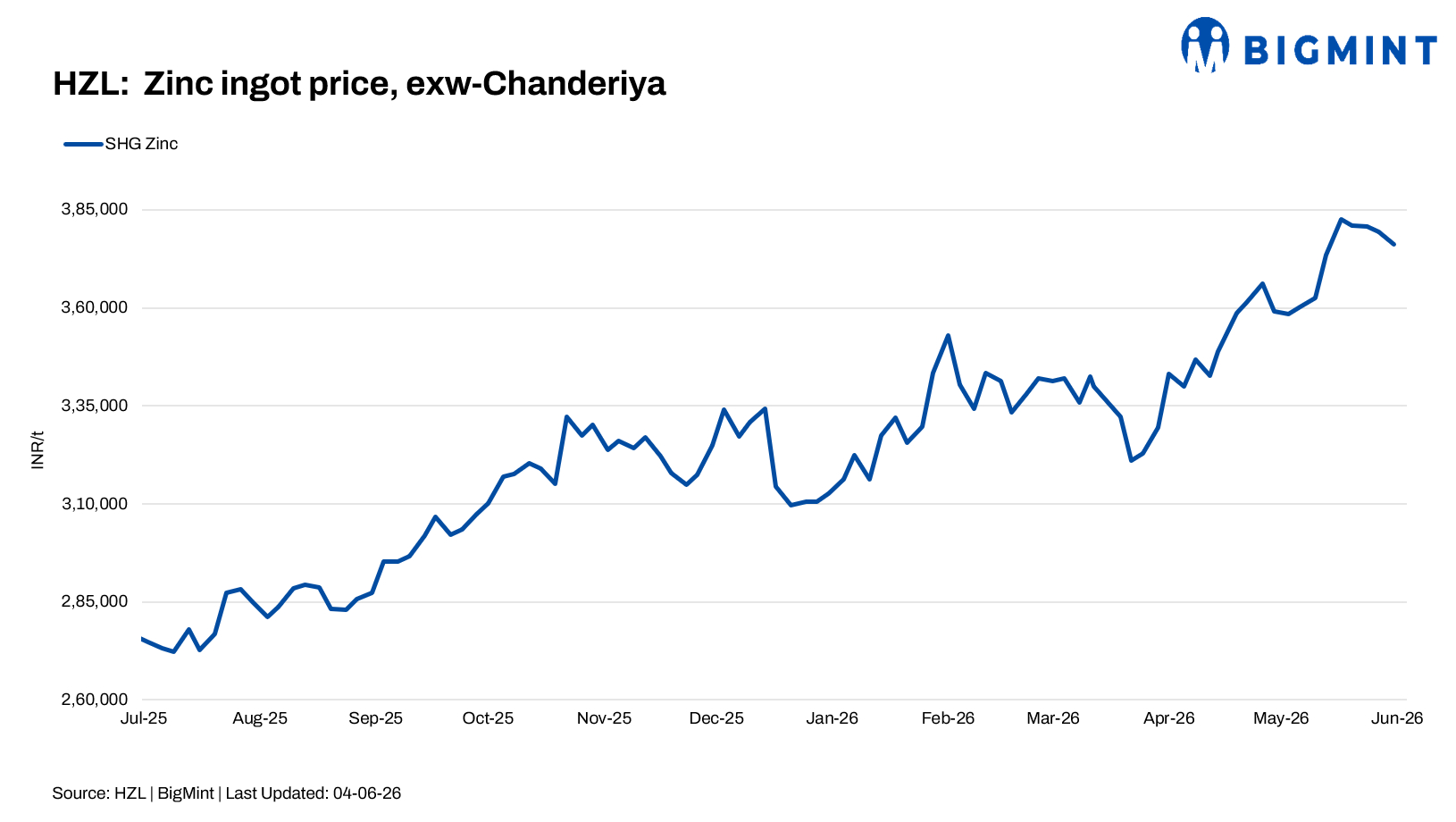

Hindustan Zinc Ltd (HZL) on 4 June 2026 increased zinc ingot prices by INR 7,400/t ($87/t) and lead ingot prices by INR 1,900/t ($22/t) compared with its previous revision announced on 1 June.

HZL’s benchmark Special High Grade (SHG) zinc ingot prices were raised to INR 383,600/t ($4,476/t), while lead ingot prices increased to INR 228,800/t ($2,670/t).

Other revised zinc grades were:

- Special High Grade-Continuous Galvanising Grade (SHG-CGG): INR 385,100/t

- Special High Grade Jumbo (SHG-Jumbo): INR 384,100/t

- High Grade (HG): INR 383,100/t

- Prime Western (PW): INR 381,600/t

On the London Metal Exchange (LME), zinc prices were trading at $3,580/t, down 0.64%, while lead prices declined by 0.67% to $2,010/t as of 12:45 PM IST.

Following the latest revision, HZL’s SHG zinc prices remained marginally above domestic spot market levels. According to BigMint’s latest assessment on 3 June, spot zinc ingot prices stood at around INR 383,000/t, ex-Delhi. Market participants indicated that procurement activity continued to be largely need based, with buyers preferring to purchase only against immediate requirements amid elevated price levels and volatile global cues.

Meanwhile, the broader outlook for zinc remained supported by ongoing supply-side concerns despite near-term pressure from a stronger US dollar. International zinc prices recently came under pressure after robust US labour market data strengthened expectations that the US Federal Reserve may maintain higher interest rates for longer, weighing on industrial metals sentiment.

However, downside risks remain limited due to persistent supply disruptions. Nexa Resources temporarily suspended operations at its 344,400 t/year Cajamarquilla zinc smelter in Peru following a fire, while an earlier explosion at Glencore-owned Kazzinc facilities in Kazakhstan also raised concerns over refined metal availability. These disruptions have added to an already tight market environment, with the International Lead and Zinc Study Group (ILZSG) projecting a refined zinc deficit of around 19,000 t in 2026.

At the same time, global inventories remain historically low, supporting market sentiment. Although expectations of improving mine supply from producers such as Boliden and Mitsui Mining and Smelting may cap further gains, analysts expect the zinc market to remain relatively tight. Goldman Sachs continues to forecast a small zinc surplus in 2026 but expects tighter market conditions beyond 2027 as mine supply growth slows while demand expands steadily.

Leave a Reply