- Risk-off sentiment drags base metals lower across LME

- Oil eases as Israel-Lebanon ceasefire cools supply concerns

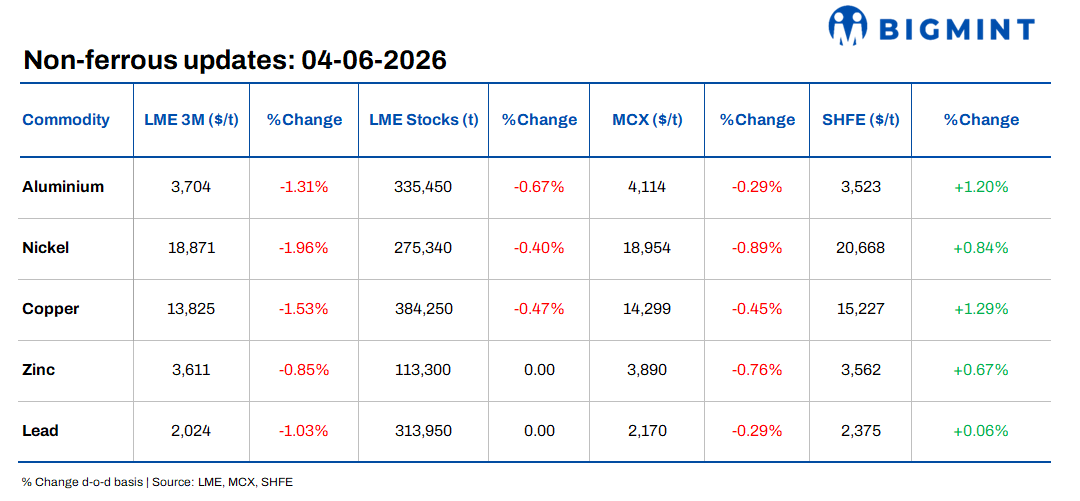

Base metals prices on the London Metal Exchange (LME) traded lower on 3 June amid prevailing risk-off sentiment. Nickel recorded the steepest decline, falling 1.96% d-o-d to $18,871/t, followed by copper, which slipped 1.53% to $13,825/t. Aluminium and lead also declined by 1.31% and 1.03% to $3,704/t and $2,024/t, respectively, while zinc edged lower by 0.85% to $3,611/t.

On the inventory side, aluminium stocks registered the sharpest decline of 0.67% d-o-d to 335,450 t, followed by copper inventories, which declined 0.47% to 384,250 t. Nickel inventories also edged lower by 0.40% to 275,340 t, while zinc and lead stocks remained unchanged at 113,300 t and 313,950 t, respectively, indicating mixed trends across LME warehouses.

Domestic market overview

India’s non-ferrous scrap market displayed mixed trends d-o-d. Aluminium tense scrap (loose), ex-Delhi, remained unchanged at INR 304,000/t, while ex-Chennai prices declined by INR 1,000/t or 0.3% d-o-d to INR 307,000/t from INR 308,000/t, indicating slightly softer regional market sentiment.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, increased by INR 10,000/t or 0.8% d-o-d to INR 1,280,000/t from INR 1,270,000/t, supported by firm copper market trends and improved spot buying activity.

Other market updates

Base metals ease amid Middle East uncertainty and tech sector weakness

Base metals prices declined on 4 June as renewed Middle East tensions and weakness across global technology stocks weighed on broader market sentiment. Copper retreated from a three-week high, while aluminium and other industrial metals also edged lower amid cautious investor positioning.

Market participants continued to monitor developments surrounding the Iran conflict, oil price volatility and potential disruptions to Strait of Hormuz shipping routes, while profit-booking and broader risk-off sentiment pressured commodity markets despite continued supply-side concerns across the metals complex.

Zambia extends duty-free copper concentrate export waiver amid smelter outages

Zambia has extended the suspension of its 10% export duty on copper concentrates until 30 September to help clear rising stockpiles of unprocessed material caused by prolonged smelter maintenance and technical disruptions. The waiver, first introduced in August, covers around 271,742 t of copper concentrate exports.

The move is expected to support mining operations and maintain export flows as Africa’s second-largest copper producer continues facing processing bottlenecks. Zambia exported around 890,346 t of copper in 2025 and is targeting annual production of 3 mnt by 2031.

Oil prices ease as Israel-Lebanon ceasefire cools supply concerns

Global oil prices declined on 4 June after Israel and Lebanon agreed to implement a ceasefire, easing immediate concerns over potential disruptions to Middle East energy supplies. Brent Crude fell near $96.9/bbl, while US WTI slipped to around $95.2/bbl.

Market sentiment, however, remained cautious amid continued uncertainty surrounding US-Iran negotiations and Strait of Hormuz shipping risks.

Fed uncertainty, geopolitical tensions keep aluminium market volatile

Global aluminium markets remained volatile as uncertainty over the US Federal Reserve’s interest rate trajectory and continued geopolitical tensions disrupted short-term price momentum. Delayed expectations for US rate cuts and persistent inflation concerns continued to pressure broader metals sentiment.

Meanwhile, Middle East tensions and ongoing risks surrounding Strait of Hormuz shipping routes continued supporting ex-China aluminium prices and tightening physical market conditions. Continued LME inventory drawdowns and elevated Cash-3M premiums also reflected persistent tightness in prompt metal availability.

Leave a Reply