- Prices rebound sharply towards week-end amid firmer base metals complex

- Exchange stocks jump above 314,000 t, limiting upside momentum

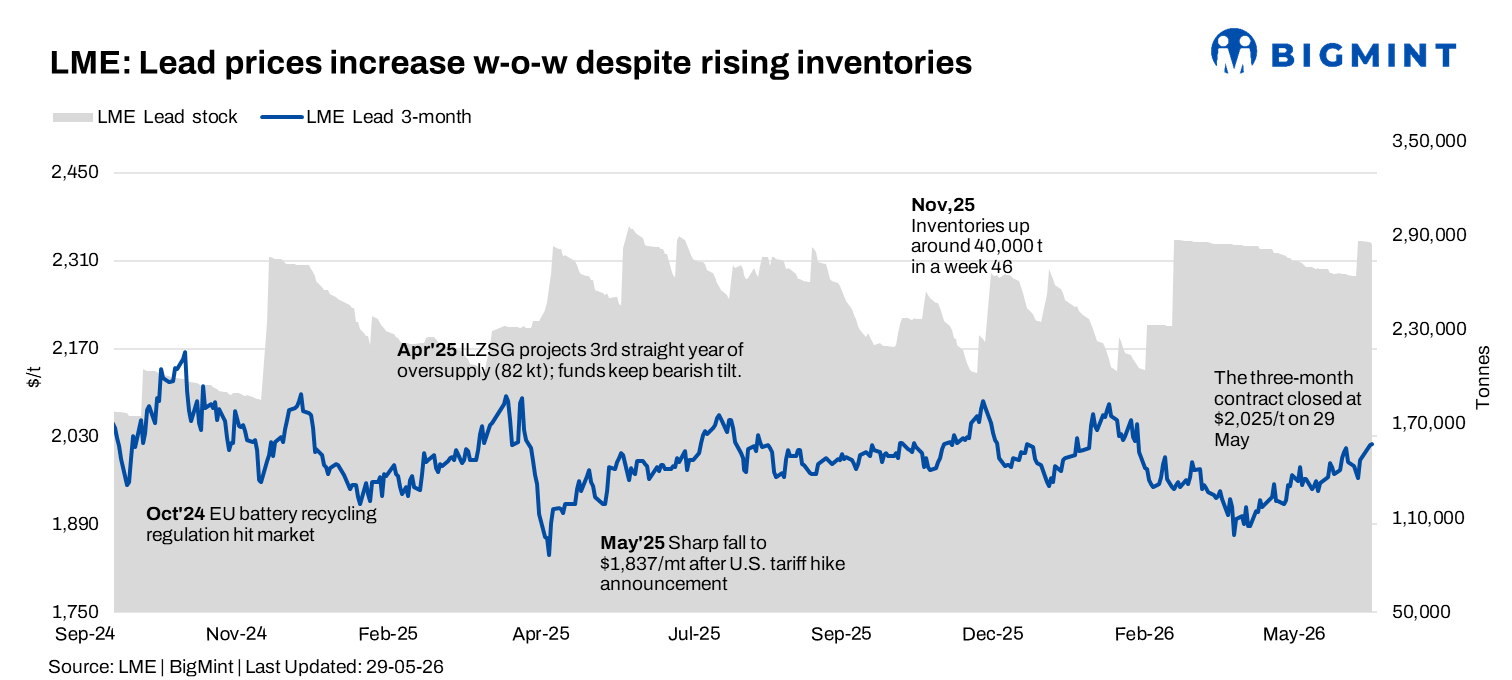

Lead prices on the London Metal Exchange (LME) strengthened during the week ended 29 May 2026, supported by improved sentiment across the broader base metals complex and renewed buying interest following the previous week’s weakness. The market reclaimed the psychological $2,000/t level towards the close of the week, although a sharp increase in exchange inventories limited bullish momentum and kept participants cautious.

Trading activity remained volatile, with prices initially firm before easing mid-week amid inventory-related concerns. However, stronger buying interest emerged towards the latter half of the week, helping prices recover and close near weekly highs.

Price trends

The LME three-month lead contract opened the shortened trading week at $2,016/t on 26 May following the Spring Bank Holiday closure on 25 May.

Prices traded within a relatively narrow range during the week, touching a weekly low of $1,991/t on 28 May before rebounding sharply to settle at $2,024.5/t on 29 May, the highest level of the week.

LME cash lead prices followed a similar trajectory. Cash settlement prices eased from $2,020/t on 26 May to $1,985/t on 28 May before rallying to $2,016/t on 29 May.

On a w-o-w basis, the three-month contract gained around $26.5/t from the previous week’s close of $1,998/t, while cash prices advanced by $10/t from $2,006/t, indicating an improvement in spot market sentiment.

The market successfully regained the key $2,000/t threshold, with immediate resistance now seen around $2,030-2,050/t and support emerging near $1,990/t.

Inventory analysis

LME lead inventories witnessed a significant increase during the week, highlighting improved material availability in exchange warehouses.

Stocks rose from 285,700 t on 26 May to 314,000 t by 28 May, representing a net increase of 28,300 t over the week. Inventories remained unchanged at 314,000 t on 29 May.

The sharp inventory build-up offset part of the positive impact from rising prices and suggests that the global lead market remains adequately supplied despite the recent recovery in sentiment.

Higher warehouse availability could continue to act as a cap on aggressive upside moves unless accompanied by stronger physical demand.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices remained largely stable throughout the week, reflecting balanced market conditions in China.

SHFE lead prices were assessed at around $2,397/t on 26 and 27 May, softened marginally to $2,392/t on 28 May, and recovered to $2,397/t on 29 May.

The absence of significant price movement suggests that downstream demand in China remained steady but lacked sufficient strength to trigger a sustained rally.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures edged higher during the week, tracking gains in the overseas market.

The May 2026 lead contract opened at INR 203.35/kg on 25 May and climbed to a weekly high of INR 205.60/kg on 27 May. The contract eventually settled at INR 205.05/kg on 29 May.

Trading volumes remained modest towards contract expiry, while open interest declined sharply from 98 lots on 25 May to just 2 lots by 29 May, indicating substantial long unwinding and position closures ahead of expiry.

Market participants largely remained cautious, preferring to square off positions despite improving international price trends.

Outlook

Lead prices are expected to remain moderately firm in the near term after successfully reclaiming the $2,000/t mark.

However, the substantial increase in LME inventories above 314,000 t suggests ample exchange supply and could restrict further upside unless physical demand improves meaningfully. Market participants will continue to monitor inventory movements, macroeconomic developments, and demand trends from the battery and automotive sectors.

Immediate resistance is seen near $2,030-2,050/t, while support is likely to emerge around $1,990/t. The overall market tone remains cautiously positive, although inventory overhangs may continue to temper bullish sentiment.

Leave a Reply