- Private miners start aligning offers with auction levels

- Monsoon restocking enquiries yet to pick up

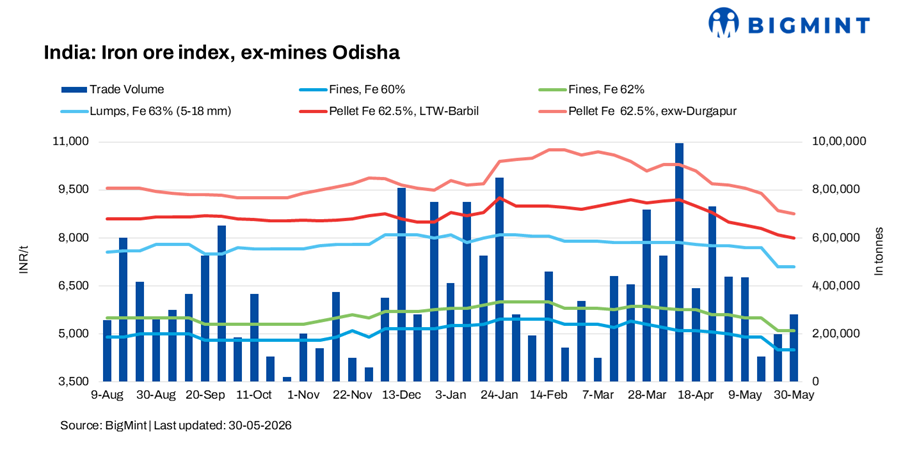

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,100/t ($53/t) ex-mines on 30 May 2026. Trading activity remained cautious following the recent Odisha Mining Corporation (OMC) auction, as buyers and sellers continued to assess post-auction price levels. While a few private miners revised offers downward in line with auction bids, several others were yet to announce fresh prices, resulting in mixed market signals.

Odisha iron ore prices largely remained rangebound during the week, with limited spot market activity. Although some bulk deals were concluded with regular buyers, market participants noted that monsoon restocking by steelmakers is yet to commence actively, restricting stronger demand in the market.

Rationale

- T1- One (1) deals for Fe 62% fines were recorded in the publishing window, and was considered for price computation. This was given 50% weightage for index calculation.

- T2 – BigMint received seventeen (17) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Fourteen (14) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Market highlights:

Market participants stated that trading activity remained cautious after the recent OMC auction, as buyers continued to assess the impact of lower auction bids on the broader market. Sources noted that the market currently lacks a clear direction, offering limited clarity to buyers on near-term price trends and procurement strategies. As a result, most purchases remained requirement-based, while participants awaited stronger signals from downstream steel markets.

A steelmaker mentioned that a few private miners had already revised their offers following the auction outcome, while several others were yet to announce fresh prices.

A miner commented, “Enquiries are still slow as market sentiment remains weak. However, we concluded some bulk deals with regular buyers during the week.”

Market sources added that steelmakers have yet to begin monsoon restocking, keeping procurement largely requirement-based. At the same time, some participants are waiting for a recovery in sponge iron and semi-finished steel prices before increasing purchases, as improved downstream realizations could help boost trade volumes and strengthen market confidence.

Factors affecting iron ore prices

Pellet prices softening: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil dropped by INR 100/t w-o-w to INR 8,000/t ($84/t) loaded to wagon on 29 May. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 100/t to INR 8,750/t ($91/t) exw.

Sponge iron showed slight recovery w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela rose by INR 500/t ($5/t) w-o-w to INR 26,000/t ($273/t) on 30 May.

Billet prices edged up w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela rose by INR 800/t ($8/t) w-o-w to INR 39,100/t ($412/t) on 30 May.

Outlook

As per BigMint’s analysis, Odisha iron ore prices are expected to remain largely stable during the first week of June. Pending monsoon restocking requirements and the gradual alignment of private miners’ offers with prevailing market levels may support fresh deals. However, a meaningful rise in trade volumes is likely to depend on a recovery in sponge iron and semi-finished steel prices.

Leave a Reply