- Need-based procurement persists as prices hold above $3,500/t

- Rising inventories cap upside, market sentiment remains supportive

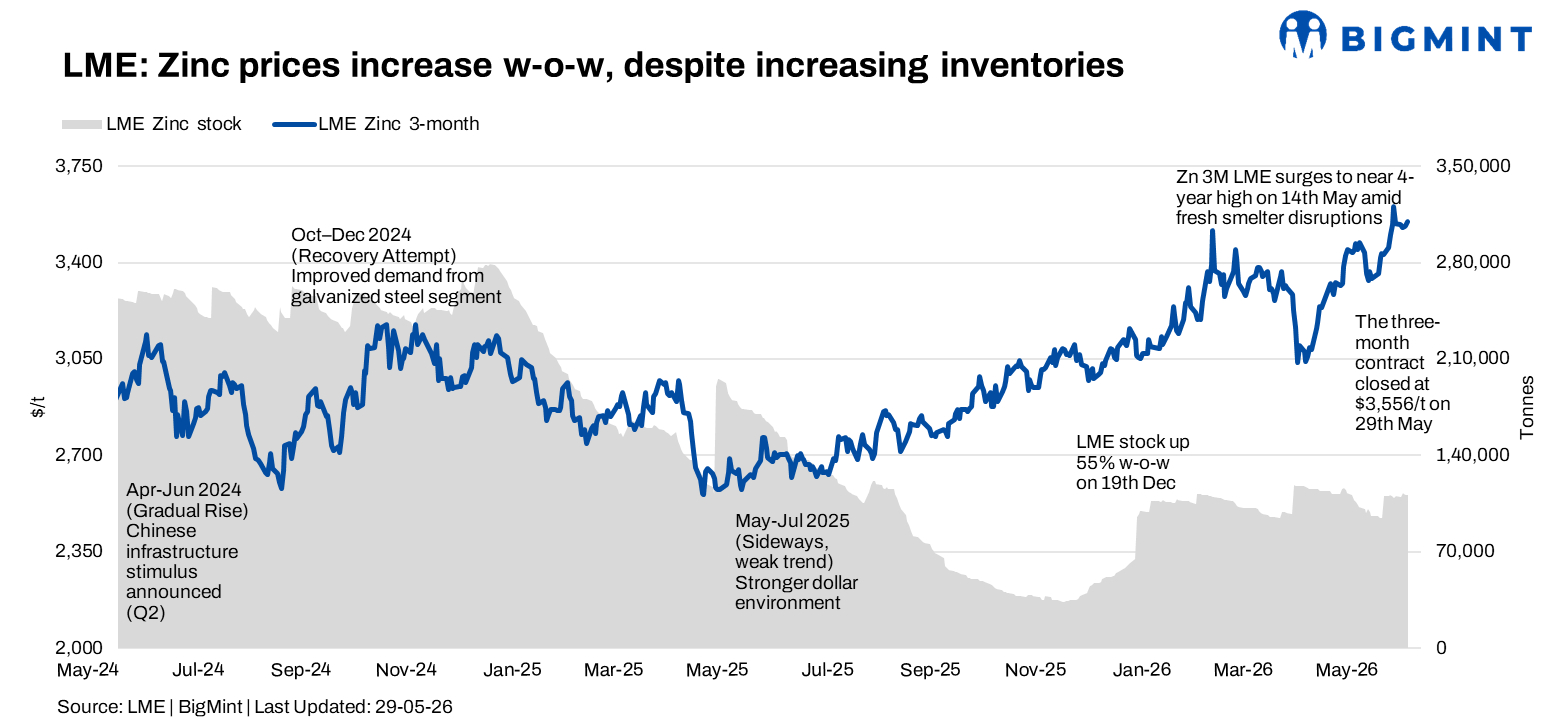

London Metal Exchange (LME) zinc prices remained broadly firm in the week ended 29 May 2026, supported by resilient sentiment across the base metals complex despite heightened volatility and fluctuating inventory levels. While prices witnessed sharp intra-week movements amid profit-booking and cautious downstream procurement, the market managed to maintain support above the $3,500/t mark, reflecting balanced near-term fundamentals.

Price trends

LME zinc cash settlement prices opened the week at $3,567/t on 26 May following the Spring Bank Holiday on 25 May. Prices came under pressure during the week, declining to $3,516/t on 27 May and further to a weekly low of $3,486/t on 28 May amid cautious buying activity and softer market sentiment.

However, buying interest improved towards the end of the week, allowing prices to recover to $3,549/t on 29 May. Despite the mid-week correction, LME zinc cash settlement prices registered a marginal w-o-w increase from $3,544.5/t recorded on 22 May, indicating continued resilience in the market.

The three-month contract followed a similar trend, easing from $3,578/t on 26 May to $3,504/t on 28 May before rebounding to close at $3,556/t on 29 May. The firm close suggests that market participants continue to maintain confidence in near-term zinc fundamentals despite intermittent volatility.

Inventory analysis

LME zinc inventories fluctuated significantly during the week, reflecting changing warehouse movements and evolving supply dynamics.

Stocks declined from 109,950 t on 26 May to 108,400 t on 27 May and edged lower to 108,325 t on 28 May. However, inventories witnessed a sharp increase on 29 May, rising to 113,800 t.

The sizeable inventory build towards the week’s close indicates improved visible availability and may limit aggressive upside momentum in the near term. Nevertheless, overall stock levels remain relatively moderate compared with historical averages, preventing a significant deterioration in sentiment.

MCX zinc trends (25-29 May)

On the Multi Commodity Exchange (MCX), zinc futures traded in a volatile but largely firm range during the week, tracking movements in the international market.

The May contract settled at INR 374,650/t on 25 May before rising to an intra-week high of INR 373,900/t on 26 May. Prices subsequently softened amid profit-booking, touching a weekly low of INR 369,650/t on 27 May. After a brief recovery to INR 373,450/t on 28 May, the contract weakened again and settled at INR 368,450/t on expiry day, 29 May.

Open interest declined sharply from 1,552 lots on 25 May to just 53 lots by expiry, reflecting routine position unwinding and cautious participation at elevated price levels. Trading activity remained active through most of the week, while domestic consumers largely continued need-based procurement amid prevailing price uncertainty.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices remained largely rangebound during the week, suggesting stable but cautious sentiment in the Chinese market.

SHFE zinc stood at $3,553/t on both 26 and 27 May before strengthening to $3,574/t on 28 May. Prices subsequently eased marginally to $3,555/t on 29 May.

The relatively stable SHFE performance indicates balanced market conditions in China, although buying interest remained measured amid ongoing uncertainty surrounding downstream demand recovery.

Outlook

BigMint expects LME zinc prices to remain supported by resilient broader market sentiment and balanced supply-demand fundamentals in the near term. However, elevated inventory levels, cautious downstream procurement, and periodic profit-booking may continue to restrict aggressive upward movement.

Prices are likely to find support in the $3,500-3,520/t range, while immediate resistance is seen around $3,580-3,620/t. Market participants are expected to closely monitor inventory trends and macroeconomic developments for further directional cues.

Leave a Reply