- Inventory drawdown fails to offset macroeconomic pressures

- EGA reroutes cargoes, easing immediate supply fears

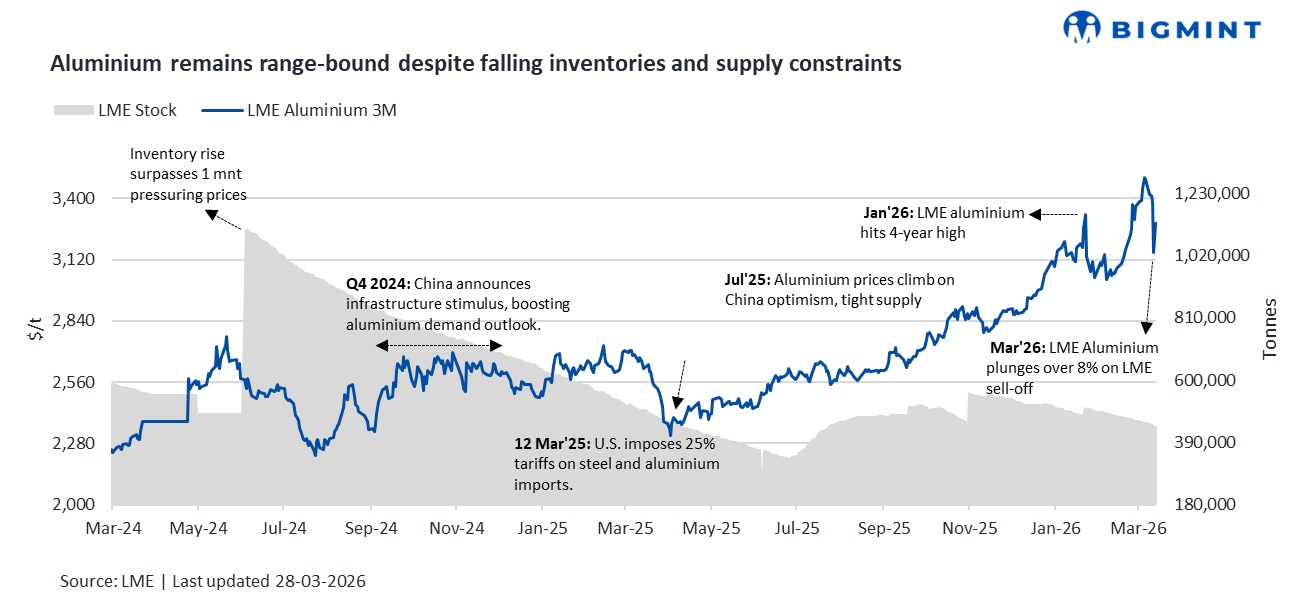

Benchmark aluminium prices on the London Metal Exchange (LME) declined marginally by 0.4% in the week ended 27 March 2026, reflecting cautious market sentiment amid macroeconomic headwinds. While supply-side concerns continued, they eased slightly due to producers exploring alternative routes.

Pricing, inventory trends

LME aluminium prices averaged around $3,250/t during the week, decreasing by $15/t or 0.4% w-o-w from last week’s $3,288/t. Prices opened the week near $3,288/t, eased to around $3,444/t mid-week, and closed at $3,273/t.

Meanwhile, LME aluminium inventories declined by 1.5% w-o-w to 423,075 t from 429,675 t, indicating tightening exchange stocks, which provided underlying support but were insufficient to drive prices higher.

Factors impacting prices

LME aluminium prices eased slightly last week, averaging around $3,250/t, down $38/t or 0.4% w-o-w, reflecting cautious market sentiment despite ongoing supply-side concerns. Prices remained range-bound through the week, moving between $3,218/t and $3,288/t, as market participants adopted a wait-and-watch approach amid mixed signals from macro factors and supply dynamics.

Supply concerns persisted in the Middle East amid logistics disruptions linked to the Strait of Hormuz. Disruptions in the Middle East, including reduced smelter operating rates and shipping delays, continued to tighten regional availability and influence global trade flows.

Declining LME inventories, which fell 1.5% w-o-w to 423,075 t, reflected tightening physical availability; however, the impact remained limited, with prices continuing to trade range-bound amid prevailing macroeconomic uncertainties.

Additionally, rising premiums in Europe reflected tightening physical supply and elevated costs, driven by both geopolitical uncertainty and higher energy prices, indicating continued stress in regional markets.

However, supply concerns were partially mitigated after Emirates Global Aluminium (EGA) rerouted shipments via alternative routes, easing immediate supply fears and contributing to a softening in LME prices. Rerouting of alumina cargoes toward China increased supply in Asian markets, leading to regional imbalances while partially offsetting broader supply tightness.

Outlook

Aluminium prices are likely to remain largely stable next week as macro headwinds and cautious demand sentiment continue to weigh on the market, despite support from declining LME inventories and ongoing supply-side risks. Persistent constraints, including reduced smelter output and shipping disruptions across Gulf trade routes, may sustain supply concerns but are unlikely to drive a strong upward trend. However, any further weakness in demand or macroeconomic conditions could exert downward pressure, with markets closely tracking inventory trends and developments in Middle East supply routes.

Leave a Reply