- Scrap-led cost push lifts semis; Turkiye buying surges after delayed restocking

- Recent airstrikes on Iran’s major steelmakers keep steel sector under pressure

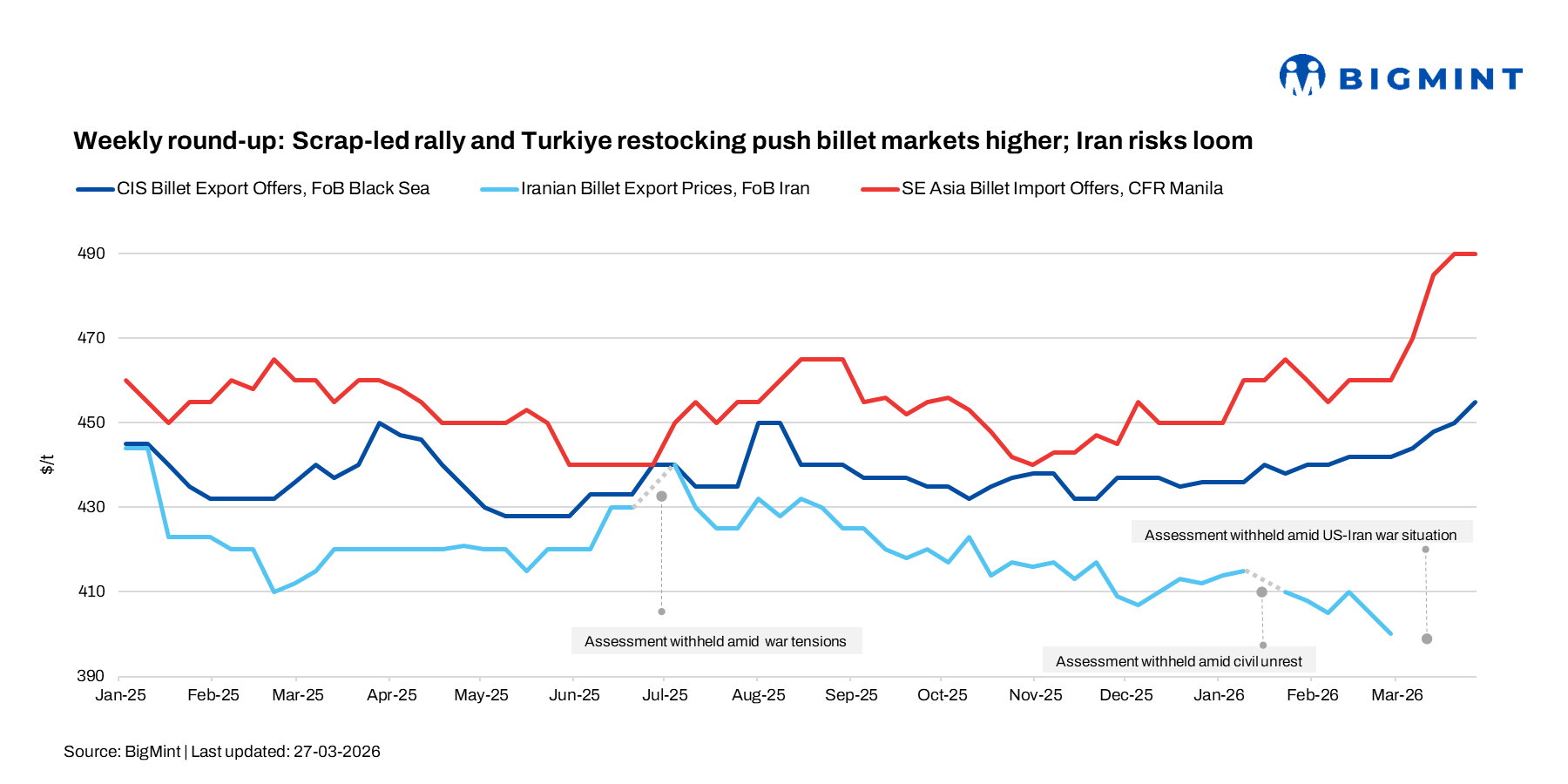

Global billet markets strengthened sharply in the week ended 27 March, as a rally in ferrous scrap prices triggered a cascading rise across billet and long steel segments. Turkish mills led market activity, aggressively booking scrap cargoes after a delayed restocking cycle, while supply disruptions, freight constraints, and geopolitical risks tightened billet availability across the CIS, Middle East, and Asia.

Turkiye & CIS Region

Turkish mills concluded at least 20 deep-sea scrap cargoes during the week, including 10-12 bookings on 27 March alone. HMS (80:20) prices were largely stable across origins, with US-origin cargoes booked at $397-398/t CFR, Baltic (Finland, Denmark) at $394-395/t CFR, UK-origin at $390-392/t CFR, and other EU-origin material within $390-392/t CFR.

The surge in bookings reflects delayed procurement cycles, with mills still short of coverage. Scrap exporters maintained firm offers, targeting up to $395/t CFR from Europe and $405/t CFR from the US.

Improved rebar demand supported sentiment, with domestic prices rising $20-25/t w-o-w to $590-610/t exw, and export offers increasing to $590-600/t FOB. Market participants noted that rising scrap costs remain the primary driver of finished steel pricing.

CIS billet prices strengthened, supported by higher scrap costs, firm Turkish demand, and rising freight rates. Russian billet offers increased to $460-462/t FOB Black Sea for May shipment, compared to $455-460/t previously. Export assessments were raised by $5/t to $455/t FOB.

Into Turkiye, tradable levels were heard at $480-485/t CFR (nearly $455/t FOB), while offers at $490-495/t CFR (around $460/t FOB) were largely unworkable.

Market insiders suggested limited deals near $485/t CFR. A weaker rouble is expected to keep export offers firm, with some suppliers indicating potential hikes of $5-10/t.

China & SEA Region

Chinese billet export offers were reported at $460-470/t FOB for May-June shipment, slightly higher w-o-w, supported by rising production costs and geopolitical tensions. Deals into Southeast Asia were concluded in the range of $475-490/t CFR, with around 35,000-40,000 t sold to Thailand during March. Offers to the Philippines were heard near $490/t CFR, though fresh transactions remained limited.

Chinese mills continued to hold firm pricing, supported by cost pressures and reduced competition from Iranian suppliers.

Regional buying interest improved, primarily driven by Thailand and Taiwan, as mills turned to alternative sourcing amid the absence of Iranian supply and elevated scrap costs. Thailand remained the most active of Chinese 5sp billet at above $490/t CFR, with prices rising from $480-485/t CFR in recent weeks due to tightening availability.

A Southeast Asian exporter said that around 5,000-10,000 t of Chinese 3sp billet was recently booked at $485/t CFR Thailand, with buyers still willing to secure volumes despite elevated prices.

Taiwan also re-entered the market, with premium-grade billet heard near $500/t CFR and 3sp material around $490/t CFR — similar cost-driven procurement needs. In contrast, the Philippines market remained subdued following earlier deals, with buyers largely adopting a wait-and-watch approach amid weak downstream demand.

GCC Region

The GCC billet market remained under pressure amid ongoing logistical disruptions linked to geopolitical tensions. Limited vessel availability, rerouting challenges, and rising freight costs continued to restrict material inflows.

In Saudi Arabia, negotiations for around 30,000 t of Russian billet were ongoing, with some cargoes being routed via Red Sea ports. Domestic billet prices were heard at $540-545/t exw, with sentiment pointing towards further increases.

In Oman, about 50,000 t of Indonesian billet was booked at $480-485/t FOB, with freight levels yet to be confirmed. Meanwhile, UAE import offers from China were reported at $530-550/t CFR, although deal activity remained uncertain.

The UAE market is facing a sharp billet shortage, with re-rollers reporting very limited availability for April. Despite the addition of new ECAS-certified suppliers, actual inflows remain constrained due to ongoing logistical challenges and supply disruptions.

Inventories have dropped to critically low levels, raising concerns of continued tightness through Q2–Q3. Irregular cargo arrivals and limited visibility on incoming shipments are making it difficult for downstream players to plan production effectively.

Iran: Iran’s steel sector has come under pressure following reported airstrikes on key producers, including Mobarakeh Steel Company and Khouzestan Steel Company, which together account for around 16 mnt/year of crude steel capacity. While the extent of the damage remains unclear, the situation has added uncertainty to billet and semi-supply. Reduced availability from Iran has already begun to tighten supply in Asia and Southeast Asia, offering support to Chinese and other regional exporters.

Outlook

Outlook

The global billet market is expected to remain firm, supported by elevated scrap prices, tightening supply, and rising freight and bunker costs. However, volatility is likely to persist amid geopolitical risks, logistical disruptions, and cautious buying behaviour.

Upside potential remains if scrap prices continue to strengthen and war-related supply disruptions persist, although sustained gains will depend on the pace of recovery in finished steel demand across Southeast Asia, the CIS, and the Gulf region.

Leave a Reply