- Weak industrial demand weighs on lower-grade coal prices

- Ample port inventories in India keep prices largely stable

Indian portside prices of Indonesian-origin thermal coal remained largely stable week-on-week as of 27 March 2026, after witnessing mild firmness earlier in the week. Market sentiment turned cautious toward the end of the week as industrial demand weakened, prompting buyers to adopt a wait-and-watch approach despite adequate availability of material at major ports.

Industrial slowdown weighs on lower-grade coal demand

Market participants reported that demand for lower-grade Indonesian coal softened notably during the week. The slowdown was primarily attributed to temporary shutdowns of several industrial units in Gujarat due to an LNG supply shortage, which reduced fuel consumption from sectors such as ceramics, chemicals, and small-scale manufacturing.

As a result, procurement activity slowed, particularly for lower calorific value coal. Although availability of such material remained ample at portside locations, muted buying interest exerted mild downward pressure on prices.

Portside price movement across key grades

According to BigMint’s latest assessment as of 27 March, portside prices across most Indonesian coal grades remained stable w-o-w. Prices of 5,000 GAR Indonesian coal were assessed at around INR 9,400/t at Kandla and INR 9,300/t at Visakhapatnam, unchanged from the previous week amid balanced supply-demand conditions.

Similarly, 4,200 GAR coal prices held steady at INR 7,700/t at Kandla and INR 7,600/t at Visakhapatnam, reflecting limited buying activity and adequate availability.

In contrast, prices of lower-grade 3,400 GAR coal declined slightly by around INR 100/t w-o-w to about INR 5,500/t at Navlakhi Port, mainly due to weaker industrial demand and cautious procurement by traders.

Port inventories in India record mild build-up

Thermal coal inventories at Indian ports registered a modest increase during the week. Total portside stocks rose by 1.9% week-on-week to 12.38 million tonnes in Week 12, compared with 12.15 million tonnes in Week 11.

The stock build-up was largely supported by fresh cargo arrivals at key west coast ports such as Mundra and Kandla, which more than offset continued inventory drawdowns at several east coast ports. The increase in stocks indicates improved availability of imported coal across major trading hubs.

Power sector coal stocks remain comfortable

Coal inventories at Indian thermal power plants also improved during the week. As of 25 March 2026, total coal stocks at power plants stood at around 58.4 million tonnes, equivalent to roughly 19 days of consumption, indicating a relatively comfortable supply position at the national level.

However, supply distribution remains uneven across the sector. Currently, around 21 thermal power plants are operating with critical coal inventory levels. Among these, 11 plants rely on domestic coal supply, seven depend on imported coal, and three operate using washery rejects, highlighting logistical and supply chain challenges within the power sector.

Indonesian policy signals supply discipline

Minister of Energy and Mineral Resources (ESDM) Bahlil Lahadalia declared his party has not changed any policy on Job Plans and Cost Budget (RKAB) coal and nickel 2026. The production of two Indonesian mining commodities initially wanted to be improved for the revenue of the country from taxes and other collections. Bahlil underscored governments to control coal and nickel supply to keep prices up in the market. If the supply is too much price can fall, then the production must be maintained.

The minister emphasized that the government continues to monitor supply levels to prevent oversupply that could weaken global prices. According to him, maintaining a balance between production and demand remains crucial to sustaining market stability and protecting national revenue from mining-related taxes.

Benchmark prices and currency movements influence import parity

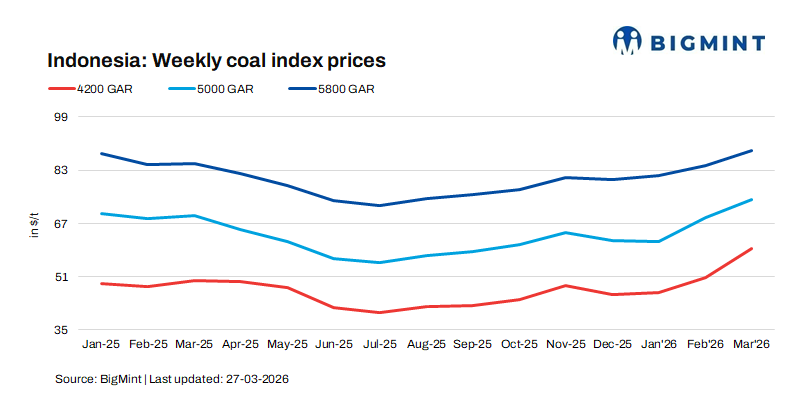

In the international market, Indonesian benchmark coal prices displayed a mixed trend during the week. Prices of 5,800 GAR coal increased marginally by around $1-1.5/t w-o-w, while 4,200 GAR coal prices edged lower by approximately $0.5/t.

Meanwhile, 3,400 GAR coal prices recorded a slight increase of $0.1-0.5/t, indicating marginal firmness in lower-grade material in the seaborne market.

Freight rates for shipments to India also softened during the week. According to BigMint’s freight assessment, Supramax freight from East Kalimantan to Navlakhi remained stable at around $19.2/t, offering limited relief to import costs.

However, the depreciation of the Indian rupee, which weakened to around INR 94.8 against the US dollar, partially offset the benefit of lower freight rates and continued to keep import parity prices relatively elevated for Indian buyers.

Outlook: Prices likely to remain range-bound in near term

Portside prices of Indonesian thermal coal in India are expected to remain mute due to ample inventories and subdued industrial demand. However, Indonesia’s supply controls may support global prices, while rupee movement and freight rates will continue to influence import parity.

Leave a Reply