- LNG shortage limits scrap generation in Chennai, prices rise INR 500/t

- Elevated pellet, coal prices keep Bellary sponge iron prices stable w-o-w

Steel prices in southern India remained stable to firm w-o-w on 27 March 2026, supported by steady to slightly higher raw material costs, particularly sponge iron and melting scrap. Scrap availability was constrained due to reduced cutting activities amid LNG scarcity, leading to lower generation. At the same time, sponge iron manufacturers faced pressure on conversion margins due to elevated raw material costs, limiting further price flexibility.

Raw materials

Sponge iron prices in the Bellary cluster remained stable w-o-w at around INR 27,500/t as of 27 March 2026. Despite the steady trend w-o-w, prices continue to hover near a 19-month high on a monthly average basis.

On a m-o-m basis, prices increased by around 5% (INR 1,300/t) in March. This growth is comparatively stronger than key central and eastern markets such as Raipur and Durgapur, indicating better price resilience in the southern region.

Bellary sponge iron manufacturers remain heavily dependent on imported coal, primarily due to strong port connectivity and the lack of nearby coal fields. This dependency makes production costs highly sensitive to fluctuations in imported coal prices.

To partially mitigate rising input costs, manufacturers have increased the blending of domestic coal with imported coal, currently estimated at around a 70:30 ratio (imported to domestic). While this strategy provides some cost relief, its overall impact remains limited.

Standalone sponge iron producers continued to face pressure on conversion spreads due to elevated raw material costs, particularly iron ore pellets and non-coking coal, though both declined w-o-w. Iron ore pellet prices were at around INR 10,950/t ex-Bellary, down by INR 50/t w-o-w, while RB2 coal prices are approximately INR 10,800/t ex-Gangavaram port, declining by INR 100/t w-o-w.

Meanwhile, in the Chennai region, ferrous scrap (HMS 80:20) prices increased by INR 500/t, reaching INR 34,500/t as of 27 March 2026. The rise is driven by tight supply conditions due to limited fresh import bookings, leading to higher reliance on domestic scrap.

“The raw material mix may shift from melting scrap to sponge iron in the short term if scrap shortages persist. In such a scenario, steel manufacturers are likely to increasingly rely on sponge iron as an alternative, aiming to manage and optimise production costs in Chennai,” a source stated.

MS billets

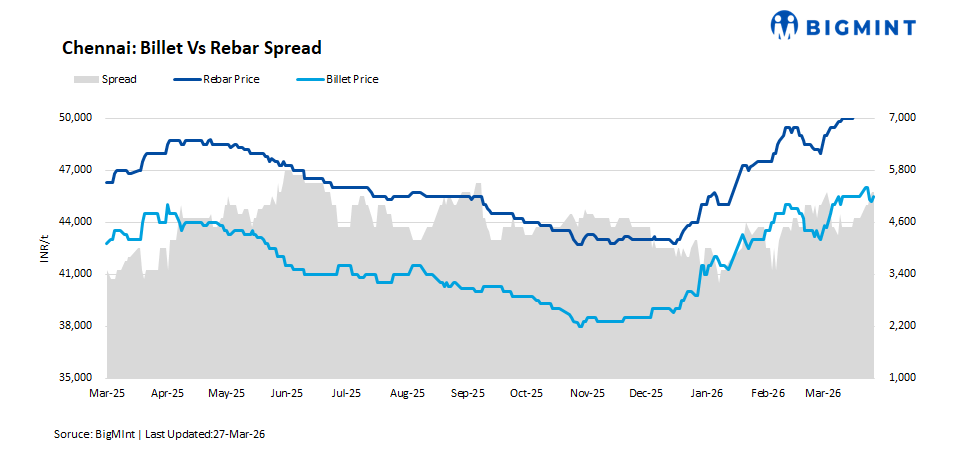

Mild steel (MS) billet prices in Chennai remained stable w-o-w at around INR 45,500/t as of 27 March 2026, primarily due to buyer resistance at higher offers, despite firm scrap prices in the region.

On the supply side, steel makers are actively liquidating their material, largely driven by the financial year-end. With limited fresh bookings, producers are focusing on clearing inventories and improving cash flow.

Additionally, market liquidity remains tight, as slower fund inflows have impacted overall trading activity. This has resulted in lower transaction volumes and cautious buying behaviour across the market.

Rebars

Finished steel demand in the southern markets remained moderately strong, with prices increasing by around INR 500/t, particularly in Chennai.

A significant portion of supply is being directed towards project-driven segments, including NHAI projects, high-rise construction, industrial corridors, Bangalore housing developments, Namma Metro and Chennai Metro expansions, and mega township projects. These segments continue to ensure steady material offtake.

Currently, there is no visible impact of LNG supply constraints in the southern market, and rolling mill operations remain unaffected. However, any prolonged geopolitical disruptions could pose supply risks in the longer term.

Rebar inventory levels at mills were maintained at around 10-15 days, indicating a balanced supply position. There was also no significant inventory pressure among induction route rebar manufacturers.

Meanwhile, blast furnace route rebar prices were at around INR 60,500/t ex-works, increasing by INR 800-1,000/t w-o-w.

Outlook

Steel prices are expected to remain stable next week due to subdued trading activity ahead of the financial year-end, as market participants limit fresh bookings. However, with the start of the new fiscal year, demand is likely to improve, supported by fresh budgets and procurement activity, which may lead to a positive price trend.

Leave a Reply