- Asian coal imports are rising as countries shift away from expensive LNG

- High gas prices are driving utilities back to coal for reliable power supply

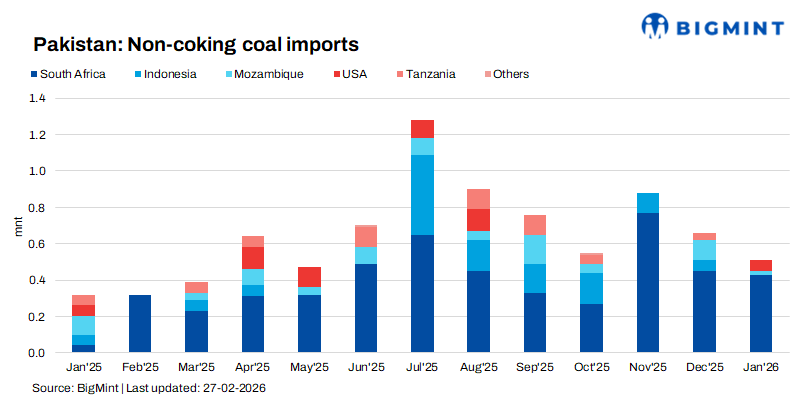

Even before the recent geopolitical tensions in the Middle East, key Asian economies were already pulling in significantly more coal. Customs data released in late March shows Pakistan’s thermal coal imports more than doubled in February compared to the same month last year, reaching 710,000 metric tons. Thailand followed a similar pattern, with total coal imports rising 5.6 percent year-on-year to 1.79 million metric tons. Australia emerged as a major beneficiary, more than doubling its shipments to both countries.

Perhaps most striking is Taiwan, where analysts have revised their coal consumption forecast upward. After months of steady decline, Taiwanese coal-fired generation is now expected to grow by 600,000 metric tons over the coming months compared to last year. This reversal comes at a time when the global benchmark for high-grade coal, the FOB Newcastle index, has fallen by roughly five dollars per metric ton from its recent peak.

Long-term planning and pragmatic choices

The surge in Asian coal demand has roots that run deeper than the current geopolitical moment. For Pakistan, the story is one of energy planning. The country has been steadily increasing its use of coal-fired power plants over the past two years, built specifically to reduce dependence on expensive imported LNG. South Africa has emerged as the main supplier, with shipments to Pakistan growing nearly fourfold compared to the same period last year. This is less about reacting to a crisis and more about executing a long-term strategy to stabilize electricity costs.

Thailand’s increased imports tell a similar story. Gas-fired generation still accounts for over half of the country’s power mix, but coal has been quietly gaining share for two consecutive years. The country’s power planners are gradually diversifying away from gas, and Australian coal, with its higher energy content, has become the preferred choice for filling this gap. The February data simply confirms a trend that has been building for months.

Taiwan represents a more recent shift. The island’s coal consumption had been declining for over a year as part of a deliberate policy to clean up the power sector. However, the sustained high price of LNG throughout late 2025 and early 2026 has forced a reassessment. With gas remaining expensive and winter power demand requiring reliable baseload generation, utilities have begun turning back to coal. The forecast revision reflects this pragmatic adjustment.

Demand to stay strong through second quarter

Asian coal demand is likely to remain robust through the second quarter, but for reasons that have little to do with the Middle East. Pakistan and Thailand are executing multi-year energy strategies that favor coal regardless of global price movements. Taiwan’s reversal may prove temporary if gas prices moderate, but for now, the economic logic favors coal.

The one uncertainty is China. While the country’s industrial power consumption remains strong, its domestic coal production is also high, which limits import demand. If Chinese utilities continue to rely on domestic supply, the impact on seaborne prices will be muted. However, for Southeast and South Asian buyers, the calculus is clear: coal remains the most reliable and affordable option for meeting growing electricity demand, and the February import data suggests they are acting on that conviction.

Leave a Reply