- Higher coking coal prices production costs

- Safeguard duty keeps landed costs of imports uncompetitive

Leading Indian steelmakers have increased list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-16/t) for early March 2026 sales. List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 53,750-55,500/t ($587-606/t) ex-Mumbai. Moreover, CRCs (0.9 mm, IS513 CR1) were listed at INR 60,400-62,750/t ($659-685/t). The price hikes could be attributed primarily to rising raw material costs and reduced imports.

Notably, after the release of February sales prices, list prices were revised again. As a result, in early March, the cumulative m-o-m increase in list prices stood at INR 1,200-1,500/t ($13-16/t).

M-o-m, trade-level HRC prices increased by INR 750/t ($8/t) to INR 54,500/t ($595/t) in March 2026 compared with INR 53,750/t ($587/t) in February 2026. Meanwhile, CRC prices rose INR 800/t ($8/t) to INR 60,500/t ($660/t) from INR 59,700/t ($652/t) in the same period.

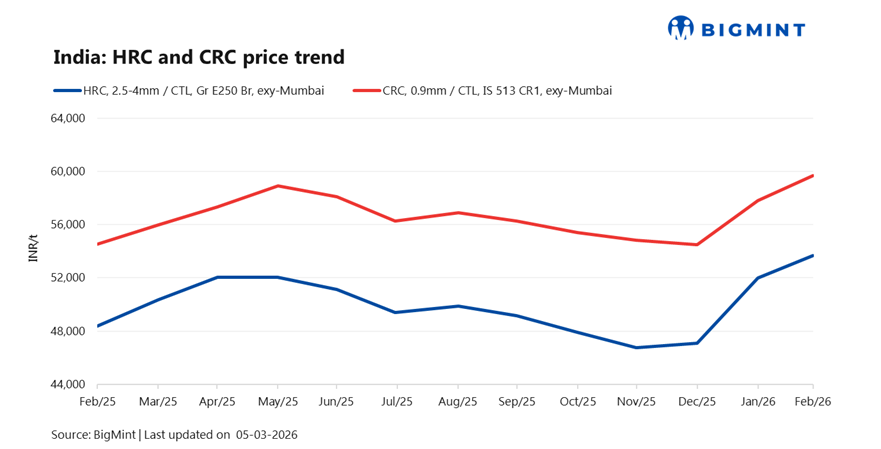

W-o-w price assessment

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices increased by INR 800/t ($9/t) w-o-w to INR 54,500/t ($592/t) on 3 March against INR 53,700/t ($583/t) in the same period last week.

CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 60,500/t ($657/t), up by INR 1,000/t ($11/t) w-o-w against INR 59,500/t ($646/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

What convinced mills to raise prices for March’26?

1. Higher raw material costs

Domestic steelmakers continue to face rising input cost pressures, particularly from coking coal, a key steelmaking raw material. Imported coking coal prices increased by $10/t m-o-m to $260/t in February, compared with $250/t in January. Meanwhile, Odisha iron ore lumps prices remained stable m-o-m at around INR 7,325/t ($80/t).

2. Safeguard duty on imports

The imposition of a 12% safeguard duty on steel imports has significantly increased the landed cost of overseas material, particularly from China and other affected countries. Consequently, the price gap between imported and domestic steel has widened, reducing competitive pressure from imports and providing domestic producers greater scope to revise prices upward.

Additional updates

Import volumes: India’s bulk imports of HRCs totalled 361,248 t in February 2026, based on vessel line-up data.

Export volumes: India’s bulk exports of HRCs totalled 227,150 t in February 2026. This marks a sharp 47% drop from 430,090 t in Dec’25, indicating softer outbound shipments at the start of the year.

Outlook

Looking ahead, India’s HRC and CRC trade prices are expected to rise, supported by recent mill price hikes and higher raw material costs. Geopolitical conflict in the Middle East has added an extra layer of volatility; if energy prices soar and logistics disruptions follow in the event of a prolonged conflict, then steel prices are expected to increase. However, market participants remain cautious, closely watching broader market trends post Holi and demand conditions to assess the sustainability of these hikes.

Leave a Reply