- Shipping disruptions stall fresh trade

- Strait risks unsettle aluminium flows

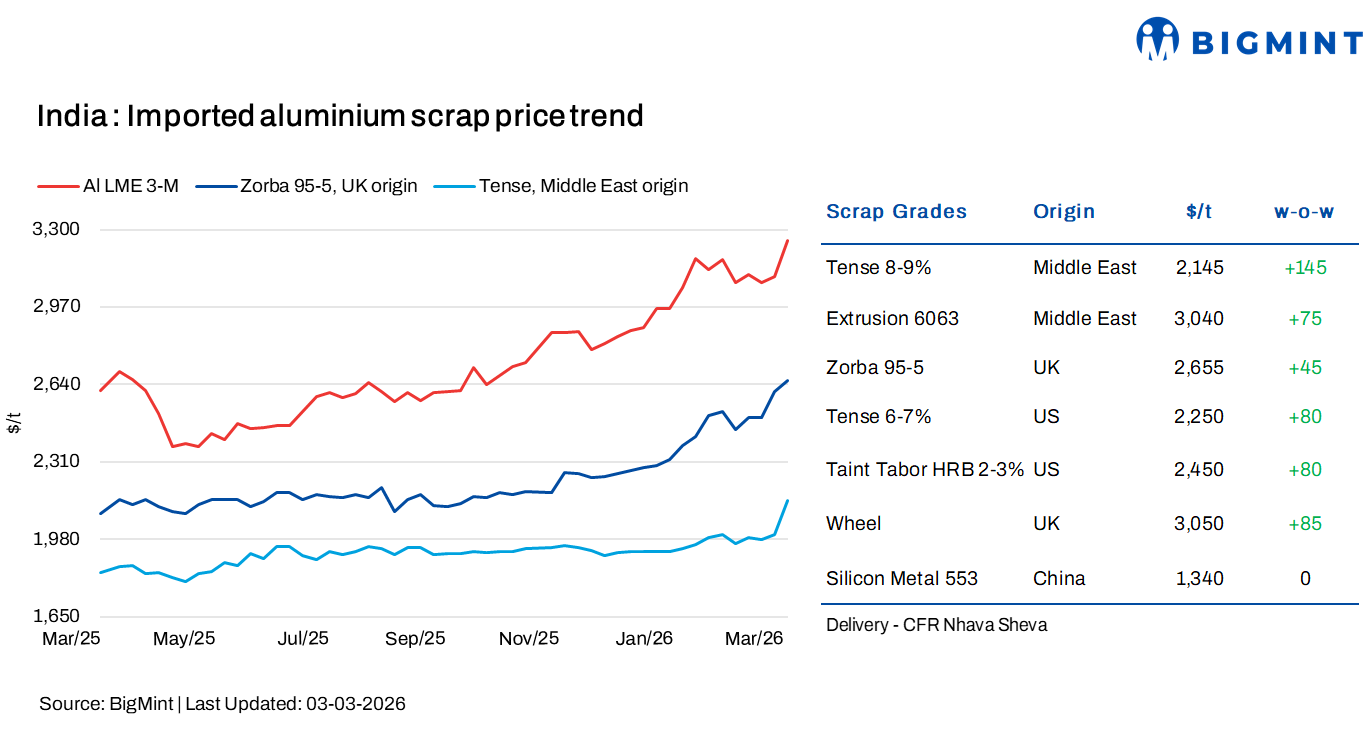

India’s imported aluminium scrap prices recorded a sharp week-on-week rise on 3 March 2026, supported by gains in LME aluminium prices and ongoing geopolitical tensions, while domestic Tense scrap prices also remained firm amid tight local supply conditions.

As per BigMint’s assessment for CFR Nhava Sheva deliveries, Middle East-origin Tense 8-9% surged by $145/t w-o-w to $2,145/t, while UK-origin Wheel scrap increased by $85/t to $3,050/t.

LME aluminium sharp gains w-o-w

LME aluminium three-month closing prices rose by 4.4% w-o-w to $3,233/t on 2 March 2026 from $3,097/t on 23 February 2026. Meanwhile, LME aluminium inventories declined by 2.1% or 10,000 t over the same period, easing from 473,550 t to 463,550 t.

LME aluminium prices climbed sharply on 2 March amid escalating geopolitical tensions and declining inventories, as the intensifying US-Iran conflict heightened concerns over potential disruptions to Middle East aluminium exports. Prices surged during early trading, reflecting market anxiety over possible shipping constraints through the strategically critical Strait of Hormuz, a key route for aluminium exports and alumina imports.

With key Gulf producers such as Saudi Arabia, the UAE and Bahrain exposed to regional instability in a region accounting for a notable share of global capacity, fears of supply tightening have raised the prospect of fresh price shocks in the US and Europe, while broader base metals traded on a mixed note.

Market insights

India’s imported aluminium scrap market reflected a firm week-on-week trend, largely tracking the sharp rally in LME aluminium prices amid intensifying geopolitical tensions. However, the strength in global benchmarks has not translated into active physical trade, as the domestic market remains constrained by severe logistical disruptions and heightened uncertainty.

Port operations are currently impacted, and major shipping lines are not accepting fresh bookings. Containers loaded toward the end of last week are yet to be assigned vessels, while rerouting of cargoes is expected to extend transit timelines for inbound shipments across carriers. With Jebel Ali and the wider Middle East acting as critical transhipment hubs, any prolonged instability in the region could significantly delay cargo flows into India.

Compounding the situation is the marine insurance challenge. Several policies are reportedly under review, and market sources indicate that war-risk premiums could rise sharply, potentially doubling. This has increased hesitation among exporters and shipping lines, effectively freezing fresh offers in the market. As a result, there are currently no clear price indications, with most suppliers refraining from quoting material.

Despite the surge in LME prices, bid levels in India remain largely unchanged from last week, underscoring a clear disconnect between exchange-driven sentiment and ground-level trading realities. Market participants noted that while asking prices to have firmed, actual transactions are minimal. With the Holi holidays further limiting activity, most buyers and sellers have adopted a cautious wait-and-watch approach until there is greater clarity on logistics and vessel movement.

On the domestic front, supply tightness has intensified. Scrap availability has been declining over the past week despite elevated price levels. Tense scrap in Chennai has moved up to around INR 227,000-230,000/t, maintaining a premium over other regions. Casting scrap and Tense grades in both Delhi and Chennai have increased by approximately INR 2,00003,000/t, with local prices rising by about INR 2/kg amid ongoing shortages. Market participants warned that further transit delays could deepen supply constraints.

In the near term, prices may remain supported if supply chain disruptions persist. However, the larger concern is not merely price momentum but the actual physical availability of material. Any sustainable recovery in trade will depend on the normalization of shipping operations, insurance clarity, and improved visibility on cargo movements.

Chinese silicon prices

According to BigMint, China-origin silicon metal 553 prices stood stable at $1,340/t w-o-w on a CFR Nhava Sheva basis.

Outlook

In the near term, the market is expected to remain volatile and sentiment-driven, with prices likely to stay firm if geopolitical tensions and logistics disruptions persist. However, actual trade activity will hinge on the restoration of shipping operations, clarity on marine insurance premiums, and vessel availability. While supply tightness may continue to support domestic scrap prices, meaningful recovery in volumes will depend on improved cargo movement and easing uncertainty in global supply routes.

Leave a Reply