- OEM settlements hit record highs

- Automotive demand lifts alloy sentiment

India’s aluminium ADC12 prices rose in January 2026, supported by higher raw material costs in domestic and global markets. Strong demand from the automotive sector offered further support, with record-high retail vehicle sales in January boosting consumption of secondary aluminium alloys. The price spread between ADC12 and scrap remained steady during the month, as scrap prices increased sharply alongside ingot price gains. This parallel movement helped maintain stable margins for producers despite overall cost pressures. Import conditions stayed favourable after the easing of ADC12 restrictions, although volumes declined on both a m-o-m and y-o-y basis. This reflected measured procurement activity and relatively balanced domestic availability.

ADC12 prices in Feb’26

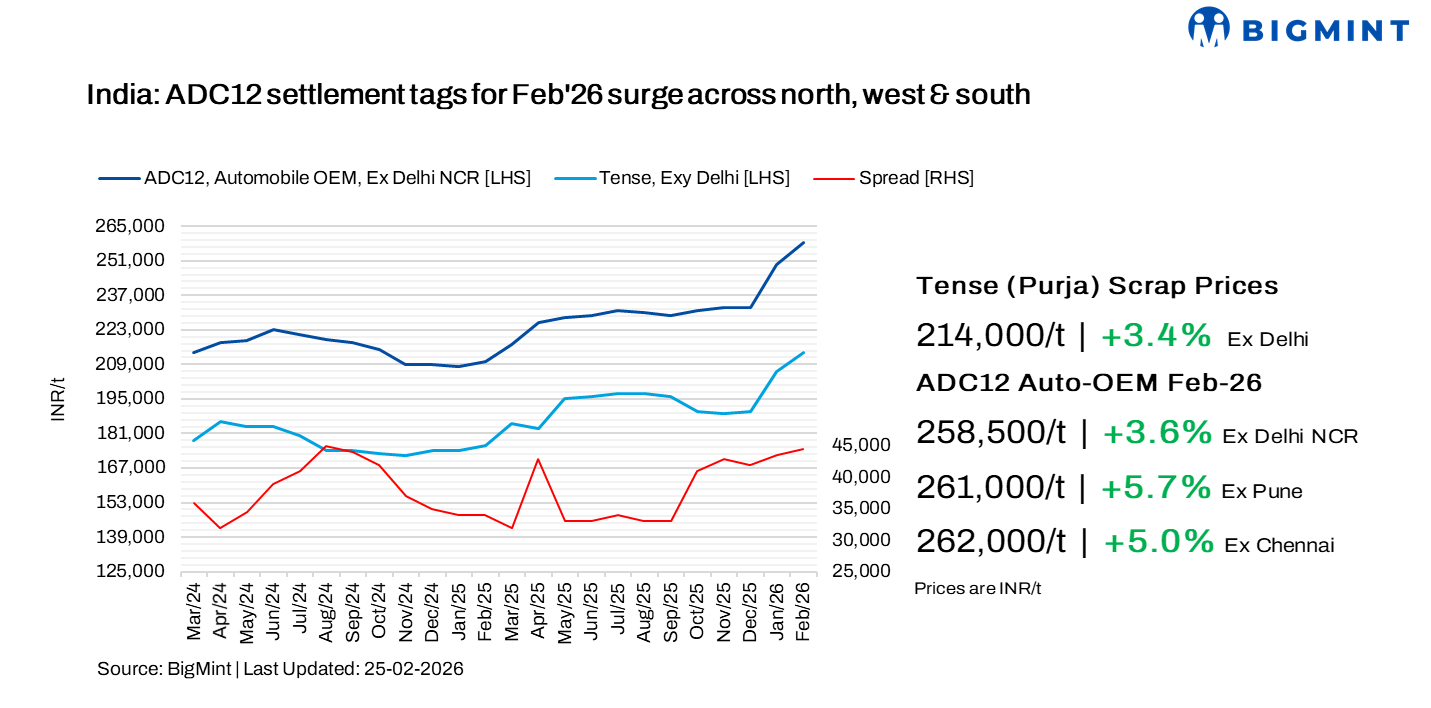

India’s aluminium ADC12 market maintained its upward trajectory in February 2026, driven by rising raw material costs and sustained strength in automotive sector demand. Prices across the northern, western, and southern regions increased by as much as INR 14,000/t during the month. Chennai recorded the sharpest rise, with prices climbing by INR 12,500/t to INR 262,000/t. Pune followed with an increase of INR 14,000/t to INR 261,000/t, while Delhi saw prices rise by INR 9,000/t to INR 258,500/t, according to BigMint’s bi-monthly assessments.

Meanwhile, the price gap between scrap and semi-finished products remained stable at INR 43,000-47,000/t. This reflected a concurrent rise in ADC12 prices and domestic scrap rates, which helped maintain steady spreads despite overall market firming.

Additionally, a leading Indian automaker has raised its ADC12 settlement price by INR 13,900/t m-o-m to a record INR 257,000/t for March 2026, marking the highest level settled to date. The March settlement was concluded in late February, earlier than the typical mid-month finalization, after prolonged negotiations, as producers and suppliers continued to quote higher offers and hold firm at elevated levels.

The upward revision reflects persistently high raw material costs and firm demand from the automotive sector. Market sources also indicated that ADC12 requirements among major automakers have increased by 10-12% compared to 2025, broadly in line with the growth in vehicle sales volumes.

Market dynamics in early Mar’25

Market feedbacks across regions indicated that supplier offers for ADC12 during late February were on the higher side, ranging between INR 262,000-270,000/t across regions. However, OEMs were actively negotiating lower settlement levels for March 2026 deliveries, typically in the range of INR 257,000-265,000/t on standard 30-day payment terms.

In the Delhi market, supplier offers were heard at INR 261,000-263,000/t, while buyer bids were reported below INR 257,000/t levels. Meanwhile, in Pune, offers stood at INR 263,000-268,000/t, with OEMs negotiating transactions in the range of INR 260,000-264,000/t.

In the southern region, suppliers were reportedly offering ADC12 at INR 265,000-270,000/t, whereas buyers were bidding levels stood at around INR 258,000-263,000/t.

Raw material trends

In February, imported aluminium scrap prices moved higher, despite a drop in average LME aluminium prices to $3,086/t, reflecting a 2.1% m-o-m drop.

However, in line with imported scrap trends, domestic aluminium scrap prices, particularly casting grade scrap used in ADC12 production, also strengthened as availability tightened, especially in the southern region.

Notably, tight scrap supply in the Delhi market led to a price increase of INR 7,000/t, with levels reaching INR 214,000/t, while Chennai prices rose by INR 15,500/t to INR 219,000/t during February. The rise in domestic scrap prices closely mirrored reduced procurement of imported aluminium scrap in the final month of 2025, driven by higher landed costs due to elevated LME aluminium prices and exchange rate pressures. As a result, secondary alloy producers increasingly turned to the domestic market for raw material sourcing, exacerbating local supply constraints.

Among key imported grades, US-origin Tense stood firm at $2,155/t, while UK-origin Wheels increased by $70/t to $2,915/t.

Meanwhile, Chinese silicon 553 prices remained largely stable at $1,345/t CFR Mundra amid steady demand.

Tracking India’s scrap & ingot import flow in Jan’26

India’s aluminium scrap imports fell m-o-m in January 2026, settling at only 0.13 mnt, a decrease of 27% compared to 0.18 mnt in the December 2025.

Post-October 2025, import volumes dropped consistently m-o-m as rising LME aluminium prices, supply disruptions, and currency volatility prompted buyers to delay purchases. India’s aluminium scrap imports fell from 0.20 mnt in October 2025 to 0.13 mnt by January 2026.

The United States remained the largest supplier, shipping 28,095 t to India, although there was a marginal drop as compared against the previous month.

ADC12 imports

In contrast, India’s ADC12 alloy imports saw a steep decline. In January 2026, inbound ADC12 volumes fell by 64% y-o-y, totalling only 441 t compared with 1,240 t in December 2025.

Auto sector performance

India’s January 2026 retail data indicated strong sequential growth across segments. Passenger vehicle sales rose 35% m-o-m to 513,475 units, while two wheelers increased 41% m-o-m to 1.85 million units. Commercial vehicle sales climbed 28% m-o-m, with three wheelers and tractors remaining largely stable. Overall retail sales grew 34% m-o-m to 2.72 million units, marking a record January performance and reflecting healthy consumer demand, improved affordability, and better inventory levels.

Auto fundamentals also remained firm. January 2026 production increased 11% m-o-m to 2.92 million units and 15% y-o-y, while retail sales rose 19% y-o-y. Support from GST 2.0 rate cuts and Union Budget 2026 measures focused on EV supply chains, localisation, battery manufacturing, PLI incentives, and public capex continues to strengthen sector sentiment and sustain price momentum.

Outlook

ADC12 prices are expected to remain bullish in March 2026, supported by continued tight domestic scrap availability, elevated import costs, and exchange rate pressures. March settlement discussions are seen in the range of INR 260,000-267,000/t across regions, reflecting sustained cost-side support. Despite buyer resistance of INR 4,000-5,000/t, strong seller confidence, firm scrap prices, and steady OEM demand are likely to keep prices well-supported throughout the month.

Leave a Reply