- Mill hikes lift HRC, CRC prices

- Holi lull keeps demand cautious

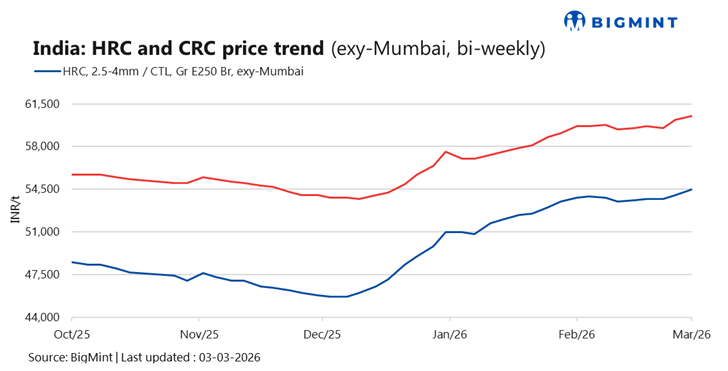

The trade-level prices of hot-rolled coils (HRC) in India show uptick across key regions amid price hike announcement during the week ending on 3 March with HRC prices assessed in the range of INR 52,500-55,600/t ($570-604/t) and cold-rolled coil (CRC) prices assessed at INR 57,000-63,200/t ($619-686/t).

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices increased by INR 800/t ($9/t) w-o-w to INR 54,500/t ($592/t) on 3 March against INR 53,700/t ($583/t) in the same period last week.

CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 60,500/t ($657/t), surged by INR 1,000/t ($11/t) w-o-w against INR 59,500/t ($646/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

The Indian trade-level HRC market is currently in a wait-and-watch phase, caught between mill-led optimism and buyer hesitation. Over the past week, two leading steelmakers lifted HRC prices by INR 750-1,000/t, setting a firmer tone across the supply chain. Traders quickly aligned their offers with the revised mill benchmarks, reflecting confidence at the producer level.

Yet, on the ground, buying enthusiasm has not mirrored this optimism. With market participants informed Bigmint, “market is largely shut over the past two days due to Holi holidays, activity has thinned and negotiations have slowed”. For now, the market remains in a holding pattern, with participants awaiting post-Holi clarity to assess whether higher offers can translate into confirmed bookings.

Meanwhile, as March-end approaches, mills are visibly focused on closing the financial year on a strong footing, reinforcing an upward price bias.

Beyond domestic factors, geopolitical developments are also under close watch. Some market participants believe that “any prolonged escalation may be limited beyond April without broader international backing”. If stability returns sooner than anticipated, confidence in trade flows and buying sentiment could improve rapidly.

Import volumes: India’s bulk imports of HRCs touched 290,543 t as of 27 February, based on vessel line-up data. Around 109,707 t of additional cargoes are expected by mid-March.

Export volumes: India’s bulk exports of HRCs touched 227,150 t as of 27 February. Around 7,692 t of additional cargoes are in transit.

Outlook

In the upcoming week, market participants are expected to maintain a cautious stance, closely monitoring the market’s ability to absorb the recent mill-led price hikes. With the Holi festival approaching and demand conditions remaining subdued, buying interest is likely to stay selective. Additionally, most traders are expected to reassess their procurement strategies only after the post-Holi reopening, when clearer indications of transactional momentum and price sustainability emerge.

Leave a Reply