- Refined output grows, ex-China production declines

- LME zinc prices gain 3.3% year-on-year

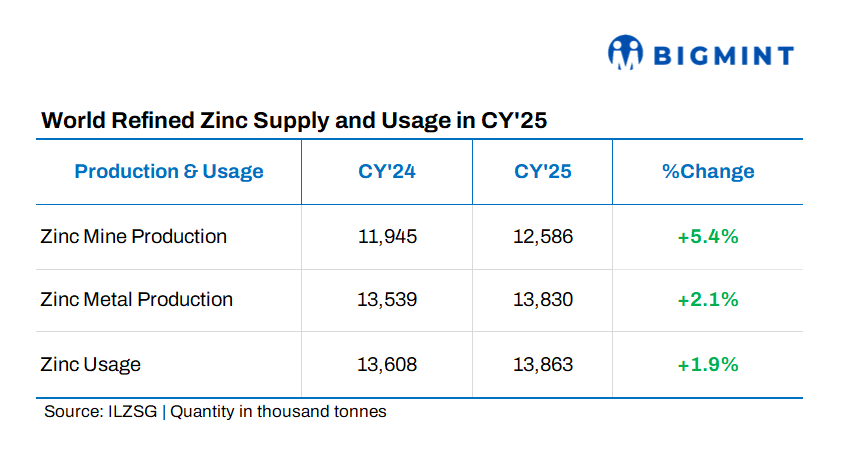

According to preliminary data from the International Lead and Zinc Study Group (ILZSG), the global refined zinc market moved into deficit in 2025, while inventories declined sharply amid tightening fundamentals.

Market deficit

In 2025, the global refined zinc market recorded a 33,000 t deficit. Reported inventories across the London Metal Exchange (LME), Shanghai Futures Exchange (SHFE) and market participants declined by 77,000 t, ending the year at 739,000 t.

Mine production updates

World zinc mine production rose by 5.4%, despite output reductions in Brazil, Eritrea, Kazakhstan and the United States.

Growth was driven by higher production in Australia, China, India, Iran, Peru, South Africa and the Democratic Republic of Congo, following the commissioning of the Kipushi mine in mid-2024.

European production also increased, supported by Bosnia and Herzegovina’s Vares operation, new capacity in Russia and the restart of Ireland’s Tara mine.

Refined output diverges regionally

Global refined zinc metal production increased by 2.1%, primarily due to a 6.1% rise in Chinese output.

However, production outside China declined by 1.6%, despite gains in Europe, Canada and Uzbekistan. Output reductions in Brazil, Kazakhstan, Mexico and Japan – including the closure of Toho Zinc’s Annaka operation – weighed on supply. Production also fell in South Korea due to a temporary suspension at the Seokpo smelter.

Demand supply scenario

Global refined zinc demand grew by 1.9%, supported by stronger consumption in China, India, Saudi Arabia, Thailand, the United States and Europe. These gains were partly offset by weaker demand in Brazil, South Korea, Peru and South Africa.

China’s imports of zinc contained in concentrates surged 29.8% to 2,575,000 t, while net imports of refined zinc declined sharply by 51.1% to 210,000 t, reflecting stronger domestic refined production.

Prices strengthen on LME

In CY’25, LME zinc cash prices strengthened, averaging around $2,867/t, up about 3% y-o-y from the prior year, while the 3-month contract averaged roughly $3,093/t. This resilience came amid sharply contracting visible inventories – LME stocks fell about 54% y-o-y to 113,670 t, with on-warrant stocks dropping over 80% through the year, driving pronounced backwardation and elevated cash premiums. Low inventory levels supported price resilience despite mixed demand signals globally.

Outlook

Refined zinc is likely to remain in a marginal deficit in the near term, supported by lower exchange inventories and steady galvanised steel demand. Smelter constraints outside China may keep supply tight despite higher mine output. LME prices are expected to stay firm around current levels, with upside capped unless demand strengthens further or inventories decline sharply.

Leave a Reply