- Global demand grows 1.5% y-o-y, refined lead output up 1.6%

- LME lead prices decline by 5% y-o-y as inventories surge 19%

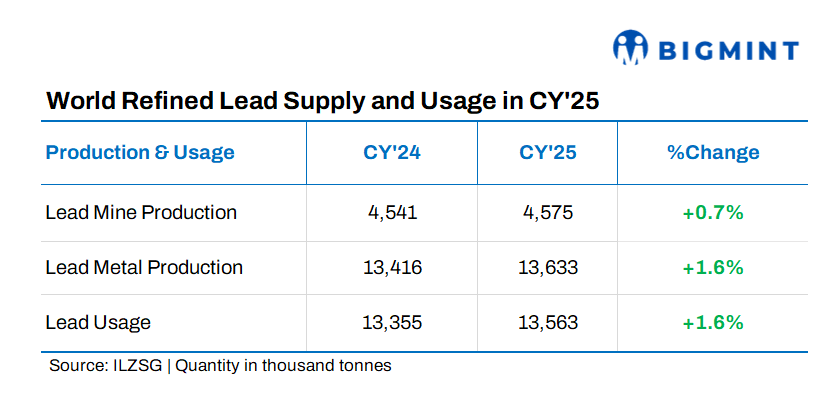

The global refined lead market remained in surplus in CY’25, shows preliminary data released by the International Lead and Zinc Study Group (ILZSG). Inventories edged higher amid slidely higher supply growth. However, despite a moderate surplus, the global lead market remained broadly balanced in 2025. Steady demand growth limited inventory accumulation and prevented sharper price declines, though upside momentum remained constrained.

Market surplus

In 2025, the global refined lead market recorded a surplus of 70,000 t. Reported inventories held by the London Metal Exchange (LME), Shanghai Futures Exchange (SHFE), as well as producers, merchants and consumers, rose by 6,000 t to reach 555,000 t at year-end.

Mine output rises modestly

Global lead mine production increased by 0.8% y-o-y. Higher output in China, India, Peru, Turkiye and Europe was largely offset by declines in Australia, Kazakhstan and the United States, resulting in only marginal overall growth.

Refined output supported by secondary capacity

Global refined lead metal production rose by 1.6%, driven by stronger output in Canada, China, India, Mexico and Brazil, where new secondary (recycled) capacities were commissioned during 2025.

Production declined in Japan and Kazakhstan, while European output remained broadly stable. Gains in Bulgaria and Sweden balanced weaker shipments at the UK’s Northfleet smelter.

Secondary raw materials accounted for 67.4% of global refined lead production in 2025, slightly down from 67.8% in 2024, highlighting the market’s continued dependence on recycling flows.

Demand-supply scenario

Global refined lead usage increased by 1.5% in 2025. Growth was led by Brazil, Taiwan (China), Turkiye, the US, and Vietnam.

European demand also strengthened, particularly in France, Germany, Poland, and the UK. However, consumption declined in Argentina and Mexico compared with 2024.

China’s net imports of lead contained in concentrates rose 14.1% to 1,243,000 t, while net imports of refined lead fell to 52,000 t, down significantly from 126,000 t in the previous year.

Pricing and LME influence

Lead prices on the LME softened on a y-o-y basis in CY’25 amid ample global availability and a steady build-up in exchange inventories. The LME 3-month lead price averaged around $1,994/t, down nearly 5% y-o-y from $2,105/t in CY’24, with prices largely trading below the $2,000/t mark for most of the year. This contrasted with CY’24, when prices frequently stayed above $2,100/t. The weaker price trend coincided with a 19% y-o-y rise in LME lead stocks, which averaged close to 247,000 t in CY’25.

Leave a Reply