- Export demand weak, may pick up fresh crop becomes available

- Increased mandi arrivals to weigh on prices during Mar-Apr’26

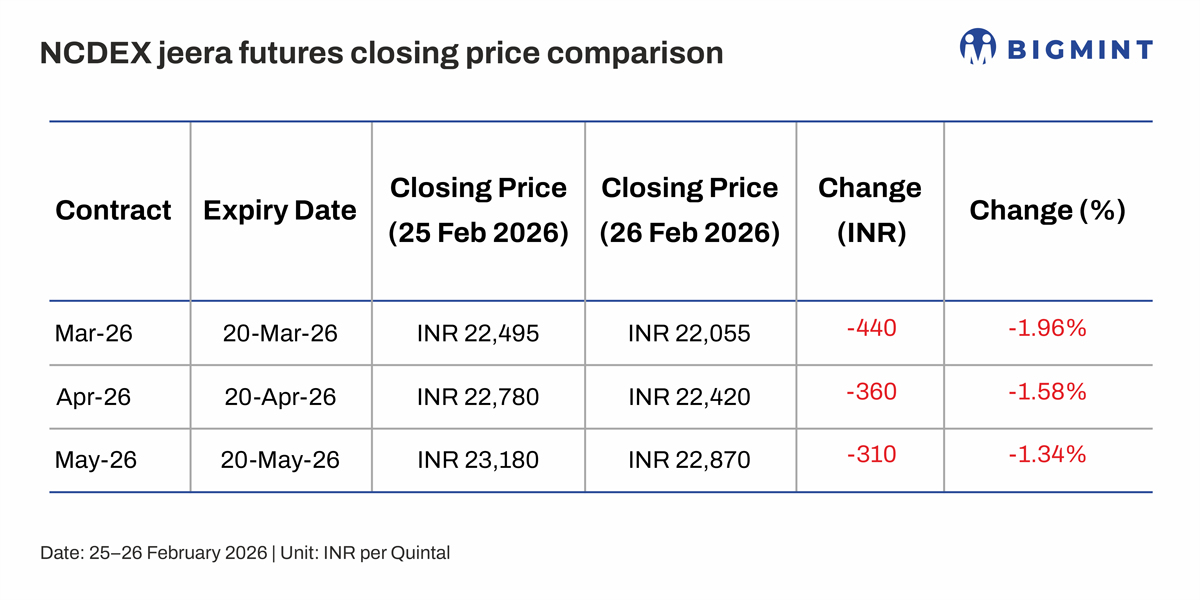

India’s jeera prices softened in late February 2026, as fresh arrivals from the new 2026 crop began entering key mandis, particularly Unjha and Rajkot. NCDEX jeera futures (most active contract) declined by 1.96% w-o-w on 26 February 2026 to INR 22,055 per quintal, reflecting early harvest pressure and cautious buyer participation. Similarly, Unjha spot prices eased by 0.26% on 26 February 2026 to around INR 22,192 per quintal, indicating mild weakness in physical markets.

Traders expect mandi arrivals to increase further during March-April 2026, which may temporarily improve supply availability and cap immediate price upside. Export demand during January-February 2026 has remained slow, as overseas buyers continue sourcing from existing inventories rather than placing aggressive forward orders.

Broader supply outlook remains tight

Despite the short-term pressure, the broader supply outlook for the 2026 crop season (harvest period: February-April 2026) remains tighter compared with the previous year. Gujarat jeera sowing for the Rabi 2025-26 season (sowing period: October-November 2025) declined by about 14.34% y-o-y to 4.08 lakh hectares, reflecting acreage correction after lower prices during the 2024-25 marketing season. Rajasthan sowing also remained slower, with emerging aphid infestation risks reported during January-February 2026, increasing uncertainty over final yields.

As a result, India’s total jeera production for the 2026 harvest season is estimated at around 85-90 lakh bags (approximately 495,000-506,000 tonnes), significantly lower (around 16-18%) than the 2025 production of about 1.10 crore bags (approximately 605,000 t). Gujarat is expected to produce around 35-40 lakh bags, while Rajasthan production may reach 45-50 lakh bags during the 2026 harvest cycle.

Carryover stock availability at the start of the 2026 marketing season (February 2026 onward) remains limited in effective tradable terms. Although farmers are estimated to hold around 20 lakh bags as of February 2026, only about 3-4 lakh bags are expected to enter the market during the early arrival phase between February and March 2026, as farmers are holding stocks in anticipation of higher prices. This behaviour may restrict immediate supply availability despite the ongoing harvest.

Export demand may pick up

Export demand trends have also influenced sentiment. India’s cumulative jeera exports during the April-December 2025 period (first nine months of FY’26) declined by 12.08% y-o-y to 145,137 tonnes (t), compared with the same period in the previous year. Weak demand from key importing countries persisted during late 2025 and early 2026, despite lower production in competing origins such as China, Syria, and Turkiye. However, global buyers may return once Indian prices stabilise and fresh crop becomes fully available during March-May 2026.

Outlook

From a technical perspective, as of 26 February 2026, NCDEX jeera futures showed fresh selling pressure, with open interest rising by 2.38% to 4,392 lots, indicating increased short-term bearish positioning. Immediate technical support is seen at INR 21,890-21,710 per quintal for the near-term trading period (late February-early March 2026), while resistance is placed at INR 22,370-22,670 per quintal.

Overall, while increased arrivals during March-April 2026 may keep prices largely stable in the short term, the combination of lower acreage, reduced production, pest risks, and tight farmer stock release suggests a stronger medium-term outlook for the 2026 marketing season (February 2026-January 2027). For exporters, traders, and stockists, price dips during the peak arrival phase may present accumulation opportunities, as supply fundamentals indicate a tighter balance compared with the surplus conditions seen during the 2024-25 season.

Leave a Reply