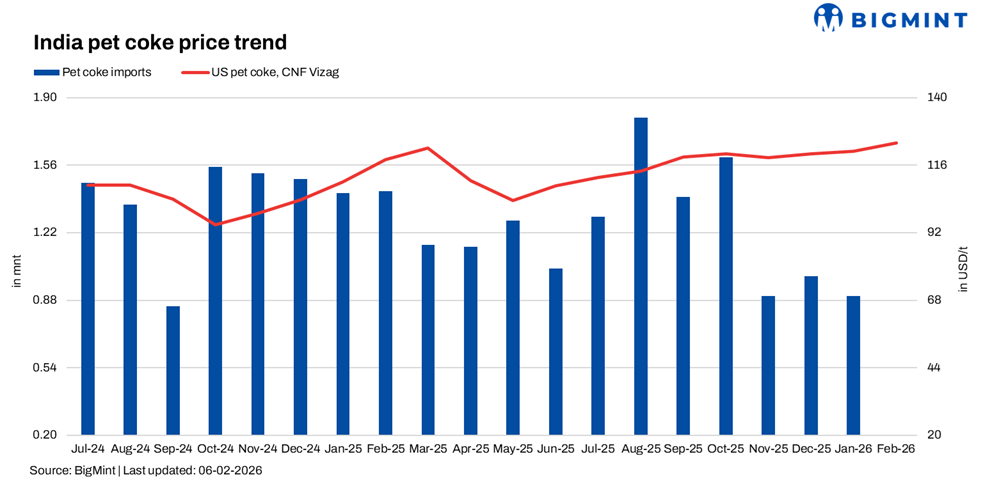

- India highest-priced major destination for petcoke

- Low-sulphur material availability remains tight in US

Global petroleum coke markets remained firm in early February, with mid- and high-sulfur grades (5.5-6.5% S) supported by steady buying from the Mediterranean and India. Price discovery improved across regions, while India continued to anchor the upper end of the global price curve, reflecting freight economics, regulatory constraints, and resilient cement-sector demand.

At the margin, fuel-mix optimisation by Indian cement producers is influencing coal-petcoke substitution decisions, but has not weakened petcoke pricing, as capacity additions, firm cement demand, and limited near-term supply keep offers elevated.

Typical cargo size: ~50,000-55,000 tonnes (t); predominantly US-origin

Market updates

India remained the highest-priced major destination for fuel-grade petcoke. CNF India indications and offers consistently clustered between $121-122/t, with bids largely at $116-118/t, both in late January and again in early February, indicating price stability rather than retracement.

Multiple cement buyers reported no change in offers over the period, with sellers maintaining levels despite some buyers attempting to test lower bids. Market feedback suggested that US-origin petcoke offers remained firm, with East Coast cargoes typically priced at a premium to west coast material.

Importantly, buyers did not point to any visible softening in market sentiment, despite tactical fuel-mix adjustments toward thermal coal. Some participants noted that geopolitical risks and freight uncertainty were reinforcing seller discipline, while others flagged that any potential US-India tariff developments could influence prices later in the year, but not in the near term.

In the Mediterranean, Turkiye remained the most liquid market, with repeated trades and converging bids for 5.5% sulfur petcoke around $108-110/t CIF, confirming this level as the current clearing range. Offers testing the mid-$110s reflect attempts to extend the rally, though buyer resistance remains visible above that range.

FOB USGC prices firmed across sulfur grades, supported by steady export pull, while low-sulfur petcoke remained structurally tight, with 2% sulfur material near $145/t FOB USWC, highlighting ongoing supply constraints.

Petcoke markets between firm and range-bound:

- CNF India prices likely to hold within $118-122/t, with offers staying sticky

- Turkiye to remain the marginal clearing market for US-origin cargoes

- Low-sulfur petcoke to retain a steep premium due to structural tightness

Downside risks appear limited unless there is a sharp correction in freight or cement demand.

The global petcoke market is being shaped less by outright demand swings and more by cost optimisation within a growing cement sector. While Indian producers are tactically adjusting fuel mixes in response to coal pricing, capacity expansion, firm cement demand, and disciplined supply are keeping petcoke prices elevated. Petcoke continues to function as a strategic cost lever, not merely a residual fuel, with India firmly anchoring the global price curve.

Leave a Reply