- Indian buyers prefer hand-to-mouth scrap procurement

- Motors scrap demand stays firm despite softer LME

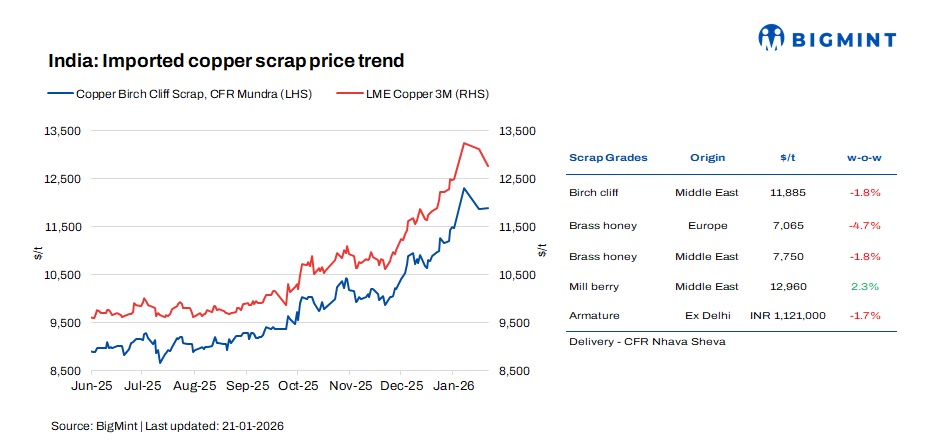

Imported copper scrap prices in India showed mixed trends w-o-w, as assessed on 21 January, even as London Metal Exchange (LME) copper futures corrected further from recent highs. Domestic copper scrap prices also showed limited movement, supported by steady underlying demand.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $11,885/t, declined nearly by 1.8% w-o-w, whereas US motors mix prices gained notably, increasing by around 2.11% w-o-w to $1,450/t w-o-w (both CFR Mundra).

LME copper extends correction

LME three-month copper prices extended their correction during the week, settling at $12,754/t on 21 January, down 2.7% from $13,106/t on 16 January and about 3.7% below the all-time high of $13,238/t recorded earlier this month. Despite the pullback, copper prices remain significantly above early-January levels, with market participants attributing the recent decline to profit-taking rather than any major shift in fundamentals.

Imported market scenario

Imported copper scrap prices in India stayed mostly rangebound this week, supported by firm demand for higher grades despite the softer LME. Market participants noted that demand for premium-quality material remained strong, with higher grades continuing to command premiums over prevailing market levels.

Motors scrap demand was reported to be robust, with trades heard even at $1,500/t levels in some cases. Participants indicated that inventories remain adequate; however, elevated LME prices continue to keep overall scrap values high.

European-origin brass scrap deals were reported at around 54-55% of LME, while Spanish-origin material was heard near 50%. US-origin brass scrap discussions were reported in the 52.5-53% range. In the domestic secondary market, CCR deals in Mumbai were heard around INR 1,170,000/t.

From the supply side, Middle East-origin copper ingots were reportedly being diverted towards China, amid rising Chinese demand. Market participants also highlighted that a few new copper plants have fully commenced operations in Palghar, Maharashtra, adding to domestic consumption interest.

Indian market updates

Domestic copper scrap market activity remained steady, supported by demand from wire rod, cable, and secondary processing units. While liquidity constraints and delayed receivables continue to pose challenges, buying sentiment has improved marginally, particularly for higher-grade material.

Traders noted that Indian buyers remain selective and cautious on pricing, preferring hand-to-mouth procurement rather than aggressive stocking. Nonetheless, stable plant-level demand has helped prevent any sharp downside in domestic prices, even as global benchmarks ease.

India’s copper scrap imports declined m-o-m in December. Imports stood at 29,760 t in December, down from 38,360 t in November, reflecting year-end logistical slowdowns and cautious buying amid elevated prices. Despite the monthly dip, total copper scrap imports for 2025 remained strong at 433,700 t, underlining sustained demand from secondary copper producers over the year.

Outlook

Indian copper scrap prices are expected to remain rangebound in the near term. While LME copper has corrected from recent highs, strong demand from China and Northeast Asia, coupled with steady domestic consumption, continues to lend underlying support. High-grade scrap is likely to trade at a premium, though liquidity constraints and cautious buying behaviour may cap any sharp upside.

Leave a Reply