- Short-term bullishness from supply squeeze

- Underlying demand remains weak

US high-NAR non-coking coal prices ex Kandla and Tuna rose sharply in January, marking one of the steepest short-term price increases seen in India’s retail coal market in recent years. Spot prices at Tuna port climbed from around INR 10,300-10,700/t in early January to INR 12,000-12,050/t by 19-20 January, according to market sources. The speed of the move over 12% in less than two weeks, points to a supply squeeze driven by market structure and positioning, rather than a sudden improvement in underlying demand.

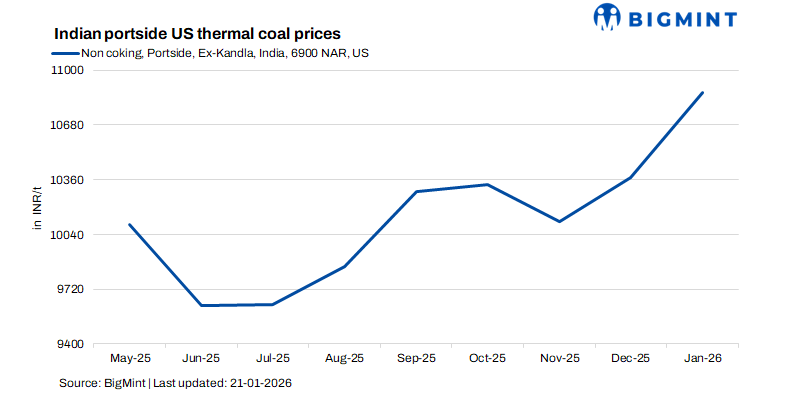

According to BigMint’s assessments, prices of 6,900 NAR US coal at Kandla was recorded at an eight-month high of INR 10,900/t, primarily due to subdued demand.

The rally reflects a convergence of three factors: forward selling by retail traders without physical cover, an unexpected surge in industrial buying following the rise in petcoke prices, and short-term logistical disruptions at key west coast ports.

Forward selling meets a demand shock

For much of 2025, the prevailing assumption in the retail non-coking coal market was that supply would remain comfortable. Imports earlier in the year were robust, prices were largely range-bound, and spot availability at Kandla and Tuna appeared adequate. Against this backdrop, many small and mid-sized traders sold coal forward – particularly for January to March delivery – without securing physical inventory at the time of sale.

Forward prices in early January reflected this confidence. Market quotes indicate January-March arrival material was offered at around INR 10,300-10,375/t, broadly in line with spot levels. Traders expected to procure material later at similar or lower prices.

That assumption unraveled in the fourth quarter.

Petcoke economics force fuel substitution

International petcoke prices rose sharply from October onward, reducing petcoke affordability for cement producers. Import data shows a pronounced fall in petcoke arrivals into India during November and December. Faced with higher costs and reduced availability, cement manufacturers pivoted toward alternative fuels, with US high-NAR non-coking coal emerging as the preferred substitute due to its consistent calorific value and operational compatibility.

This shift led to a sharp increase in direct industrial procurement of US coal during October-December, absorbing volumes that might otherwise have flowed into the open retail market. By the time January arrived, much of the forward material had already been committed to industrial users, leaving limited unallocated tonnage for retail buyers.

Port stocks tighten as despatches surge

The impact became visible at the ports in early January. Market data shows combined stocks at Kandla and Tuna of around 360,000 t in mid-January. At the same time, despatches surged. In the 10 days prior to 17 January, daily despatches of US high-CV coal averaged 14,000-15,000 t per day, according to market participants. Weekly lifting in week-2 alone exceeded 100,000 t, implying less than four weeks of effective cover at prevailing offtake rates.

Floating cargoes provided pipeline replenishment but did not create surplus, as much of this material was already committed.

Logistics disruptions exacerbate squeeze

Short-term logistical issues further amplified the price spike. Market participants report slower truck turnaround times at Kandla – stretching to three to four days per trip – leading to congestion and delayed lifting. These issues escalated into a temporary truck-union stoppage at both Kandla and Tuna in mid-January, effectively freezing physical movement even as prices continued to rise.

With Kandla facing loading constraints and concerns over quality consistency in certain stockpiles, buyers increasingly favoured Tuna-based material. This divergence allowed sellers with available Tuna stocks to command a premium, pushing Tuna prices toward INR 12,000/t while Kandla prices lagged.

Prices reprice as shorts scramble

As availability tightened, prices moved rapidly. Spot prices climbed first, followed by a sharp upward adjustment in forward quotes. February-March arrival material was raised to INR 10,600-10,850 plus taxes within days. The premium for “guaranteed” parcels widened significantly, underscoring that certainty of supply – not demand optimism – was driving the rally.

Traders who had sold forward without physical cover were forced back into the market to meet commitments. With limited spot availability and industrial buyers already covered, this triggered a classic short-covering squeeze.

Outlook: Tight but not broken

Market participants expect some price normalisation once logistical issues ease and lifting resumes, particularly for February onward deliveries. However, structurally, the market remains tight. Port stocks are low, the peak brick-kiln season is approaching, and the retail market remains sensitive to any mismatch between forward commitments and physical availability.

The January episode serves as a reminder that in a market with concentrated upstream supply and fragmented retail distribution, price volatility can be extreme when positioning and logistics collide.

Leave a Reply