- Output curbs fail to rebalance oversupply

- Weak domestic demand drives record high exports

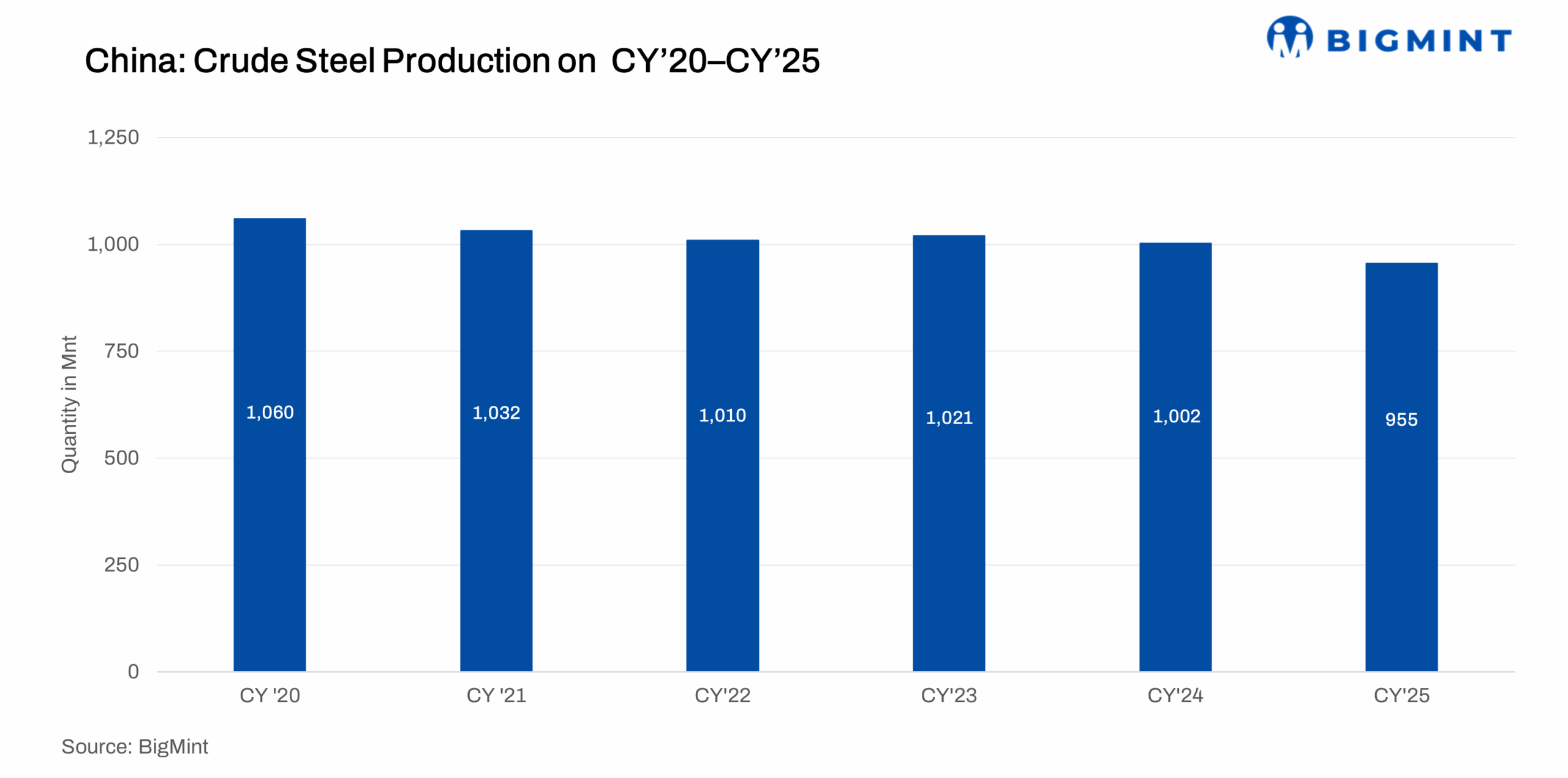

China’s crude steel production reached 960.81 million tonnes (mnt) in 2025, marking a 4.4% y-o-y decline, from 1002.32 mnt in 2024, according to data from the National Bureau of Statistics (NBS). Moreover, crude steel output in December 2025 stood at 68.18 mnt, down by 10.3% y-o-y from 75.97 mnt in December 2024.

This decline in crude steel production is mainly due to weaker domestic demand in China, particularly from the property sector, with softer consumption prompting mills to scale back output. Meanwhile, rising exports highlight growing reliance on overseas markets, reinforcing concerns over oversupply, despite production curbs.

Factors affecting crude steel output

Weak domestic demand: China’s domestic steel demand remained subdued, with weak consumption continuing to limit any upward price momentum. According to the China Iron and Steel Association (CISA), total steel inventories at key Chinese enterprises increased by 290,000 t, or 2% m-o-m, to 15.04 mnt in early January, up from 14.75 mnt in early December. Y-o-y, inventories surged by 2.45 mnt, or 19.5%, from 12.59 mnt in early January 2025.

Although supportive monetary policies and targeted economic measures offered limited price support, demand fundamentals remained weak. As a result, persistent oversupply in the domestic market prompted producers to channel more volumes into export markets to alleviate inventory pressure, further widening the supply-demand imbalance.

Increase in steel exports: China’s steel exports reached an all-time high of 119.01 mnt in 2025, up by 7.5% y-o-y from 111.01 mnt a year earlier, according to the General Administration of Customs. Weak domestic demand has prompted producers to channel more volumes into overseas market, to ease inventory pressure and maintain production rates. In December 2025, steel exports reached 11.30 mnt, the highest monthly level of the year, registering a 16.2% y-o-y increase from 9.72 mnt in December 2024. Exports also rose 13.2% m-o-m from 9.98 mnt in November 2025.

This surge in exports was supported by China’s highly competitive pricing, which continued to exert pressure on other exporters. Average Chinese hot-rolled coil (HRC) export offers fell by $52/t y-o-y to $466/t FOB in 2025, compared with $518/t in 2024. Although Indian HRC export offers to the Middle East and Southeast Asia declined more sharply, down $89/t y-o-y to an average of $492/t FOB from $581/t in 2024, they still remained above Chinese levels, reinforcing China’s export competitiveness and supporting higher shipment volumes. Meanwhile, Japanese HRC export offers dropped by $73/t to $470/t FOB in 2025 from $543/t in 2024, while South Korean offers declined by $52/t y-o-y to $493/t from $545/t in the previous year.

Outlook

The increase in steel inventories in early January underscores the continued softness in China’s domestic demand. Persistently weak consumption and elevated stock levels are expected to prompt mills to channel a larger share of output toward exports. Backed by competitive pricing, this export-oriented trend is likely to extend into the first quarter of CY’26. While the recently introduced export licensing system could moderate shipment volumes in the near term, China’s steel exports are expected to remain robust in the absence of a sustained recovery in domestic end-user demand.

Leave a Reply