- ADC12 import volumes fell 44% y-o-y in 2025

- Domestic scrap prices rose sharply in CY’25

- GST 2.0 reforms improved vehicle affordability, boosting demand

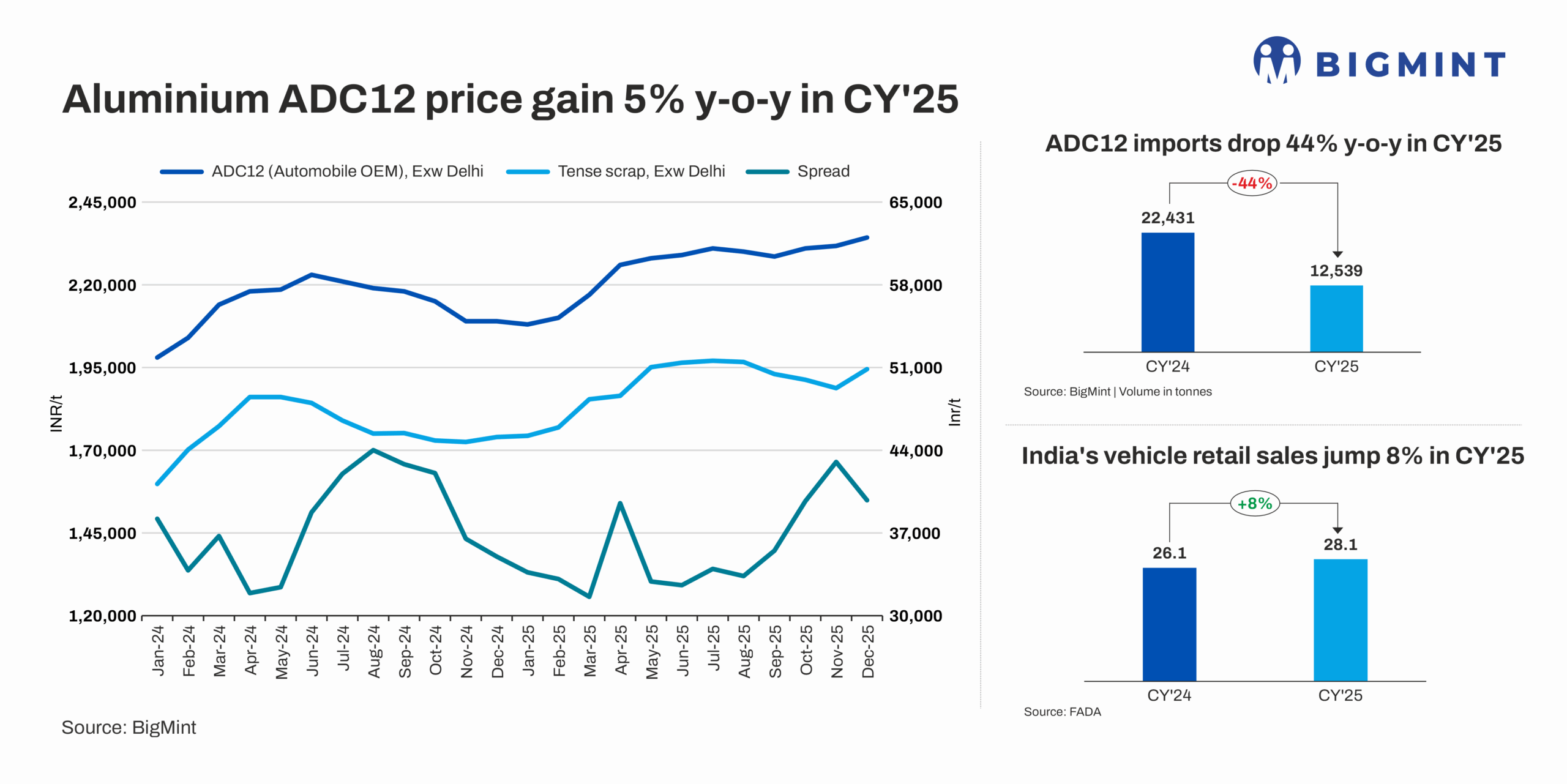

India’s ADC12 aluminium alloy ingot prices strengthened on a year-on-year (y-o-y) basis in calendar year (CY) 2025, supported by firmer domestic market fundamentals. Average OEM ADC12 prices in Delhi increased from INR 213,875/t in CY’24 to INR 225,375/t in CY’25, reflecting a 5.4% rise y-o-y.

Likewise, average OEM prices in Chennai climbed from INR 215,450/t to INR 226,021/t, marking a 5% increase y-o-y.

The average price spread between ADC12 and tense scrap narrowed slightly to INR 35,000-36,000/t in 2025, compared with INR 37,000-38,000/t in 2024. This compression was primarily driven by a sharp rise in raw material costs, while ADC12 prices increased at a comparatively slower pace.

What supported the rise in ADC12 prices in 2025?

Raw material pricing trends

Benchmark aluminium prices on the London Metal Exchange (LME) recorded a firm y-o-y increase in CY’25, rising by 6.3% to average $2,635/t, compared with $2,457/t in CY’24. The price uptrend was supported by tighter global supply, as LME aluminium stocks declined by around 6% y-o-y, easing to 0.48 mnt from 0.51 mnt, signalling reduced visible inventories.

In line with the stronger LME aluminium prices, both imported and domestic aluminium scrap prices increased y-o-y in CY’25. As per BigMint’s assessment, UK origin Zorba 95/5 scrap rose 5% y-o-y to $2,160/t CFR India, up from $2,062/t in CY’24. Similarly, other grades like US Tense (6-7%) also saw an increase of 5% y-o-y in CY’25 reaching $1,960/t from the previous year’s levels of $1,865/t, reflecting higher global aluminium prices and firm overseas offers.

On the domestic front, Tense scrap prices climbed 10% y-o-y to INR 191,044/t ex-Delhi, compared with INR 174,252/t in CY’24, tracking the rise in primary aluminium prices and improved market sentiment. Despite the rise in domestic prices, buyers continued to favour imported scrap as landed cost remained more competitive–lower by INR 4,000-5,000/t. This price advantage supported higher arrivals of imported material during CY’25.

India’s aluminium scrap imports are expected to nearly reach 2 million tonnes (mnt) in 2025, marking a 15% increase from 2024 levels of 1.75 mnt, largely driven by the imposition of US tariffs. The rise reflects a significant realignment in global scrap trade flows following reduced shipments from the US, traditionally India’s largest supplier.

Higher US tariffs, coupled with stronger domestic demand, sharply curtailed US export availability, creating a supply gap for Indian buyers and accelerating a shift toward alternative sourcing regions. The US tariff regime–introduced at 25% and later raised to 50% from 4 June 2025–also prompted US buyers to increase scrap imports from Canada and the EU, where scrap remained tariff-exempt, further tightening global supply.

To offset this shortfall, India expanded procurement from the UK, broader Europe, the UAE, Saudi Arabia, and Australia.

ADC12 imports drop in CY’25

India’s ADC12 alloy market saw a sharp decline in imports in CY’25, with inbound volumes falling 44% y-o-y. Total ADC12 ingot imports dropped to 12,539 t in CY’25, compared with 22,431 t in CY’24, this was majorly due to the BIS certification issues in the initial months of 2025 despite of having FTA advantage with major supplying countries like Malaysia.

Malaysia, traditionally India’s largest supplier of ADC12 alloy, witnessed a notable fall in shipments in CY’25, emerging as the key reason behind the overall decline in ADC12 imports during the year.

Imports from Malaysia dropped by 39% y-o-y to 9,539 t in CY’25, compared with 15,627 t in CY’24. The decline was largely driven by delays in securing Bureau of Indian Standards (BIS) certification, despite the existence of a Free Trade Agreement (FTA) between India and Malaysia.

Although several Malaysian producers had applied for BIS approval, the lengthy and stringent certification process continued to restrict export volumes. As a result, shipments remained constrained throughout the year, with most Malaysian ADC12 supplies primarily directed to southern India, supported by proximity and established buyer relationships.

Rise in auto demand post GST cuts

Retail sales of vehicles in India grew nearly 8% in 2025 to 28.16 million units, compared with 26.15 million in 2024, according to the Federation of Automobile Dealers Associations (FADA).

FADA President CS Vigneshwar said 2025 started subdued due to selective financing and cautious consumer sentiment. However, the landmark GST 2.0 rate rationalisation from September onwards, which included meaningful tax reductions for small cars, two-wheelers, three-wheelers, and key commercial segments, improved affordability and lifted demand.

Additional factors supporting growth included festive-season and year-end buying, stronger rural cash flows from better crop forecasts, favorable financing conditions with the RBI repo rate at 5.25%, and positive consumer sentiment.

EV adoption and increased use of CNG also contributed to a more diversified mobility mix, further supporting retail sales growth. FADA expects demand to remain strong in early 2026, supported by post-GST sentiment, festivals, and disciplined inventory management.

India’s leading automaker’s ADC12 settlements

India’s leading automaker reported higher settlement prices for ADC12 in 2025, reflecting rising input costs and strengthening demand. Average ADC12 settlement prices stood at INR 222,959/t in 2025, up 5% y-o-y from INR 212,346/t in 2024. Notably, January settlement prices hit a 4-year high levels.

The upward trend extended into early 2026, with January settlements increasing by INR 3,300/t to INR 235,900/t, compared with INR 232,600/t in December 2025. These settlement levels serve as a benchmark for other OEMs and automobile manufacturers in their monthly pricing negotiations.

The increase in settlement prices aligned with higher raw material costs, improving automotive demand, and exchange-rate pressures. Overall, the rise in ADC12 settlements has set a firmer pricing tone for the early part of 2026.

How did ADC12 exports perform in 2025?

India’s ADC12 export volumes showed only marginal growth in 2025, as a large share of ADC12 alloy production was absorbed by strong domestic automotive demand, limiting surplus availability for overseas markets. Total ADC12 exports increased by just 4% y-o-y to 9,850 t in CY’25, compared with 9,470 t in CY’24, highlighting that export growth remained subdued despite stable trade flows.

Japan continued to dominate India’s ADC12 export basket, accounting for the majority of shipments. Exports to Japan rose modestly by 4% y-o-y to 8,810 t in CY’25, up from 8,489 t in CY’24. However, market feedback suggests that this increase was largely incremental rather than demand-led, as Japanese automotive demand remained soft through much of 2025, limiting fresh contract volumes despite continued export offers from Indian suppliers.

At the same time, robust domestic automobile production and steady OEM procurement pulled more ADC12 into local consumption, reducing the incentive to aggressively push exports. While export offers to Japan remained available, shipments were slower to materialise, keeping overall export growth limited.

Overall, the data indicates that India’s ADC12 exports did not decline sharply but remained capped, with only low single-digit growth in CY’25, as strong domestic demand offset weak appetite from key export destinations such as Japan, preventing a stronger rebound in overseas shipments.

What may happen in 2026?

As of early January, offer levels for ADC12 across northern, southern, and western India have witnessed a significant increase, with prices hovering in the range of INR 245,000-250,000/t. However, market sources indicate that buyers are negotiating aggressively and limiting acceptance of higher offers, with bids reportedly placed INR 5,000-6,000/t below prevailing offer levels. Despite this resistance, most alloy ingot manufacturers expect prices to remain firm through Q1 CY’26.

ADC12 prices in India are likely to remain firm to mildly bullish over the next three months of 2026, supported by elevated aluminium scrap costs, a strong LME aluminium complex, and steady automotive demand. Tight domestic scrap availability, higher landed import costs due to currency pressures, and limited relief on global scrap supply will continue to underpin prices.

However, any upside in prices could be capped, as OEMs are expected to resist aggressive hikes after recent settlement increases. Post-festive demand normalisation and cautious procurement could also temper momentum. Overall, ADC12 prices are expected to rise marginally in the near term, closely tracking scrap price movements and LME aluminium trends through Q1 2026.

Leave a Reply