- Lower Chinese exports tighten global supply

- Capacity expansions in Indonesia face delays

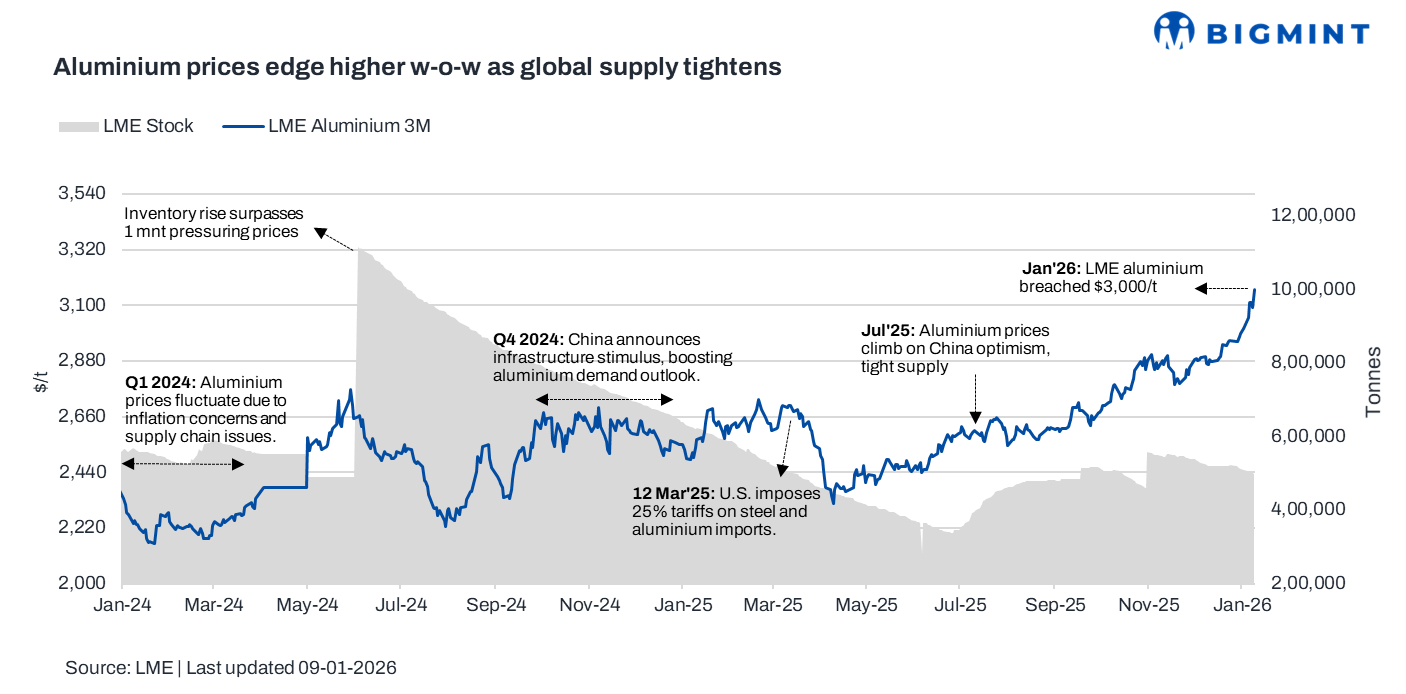

Benchmark aluminium prices on the London Metal Exchange (LME) edged higher by 4% during the week ended 09 January 2026, driven by tightening supply conditions, China’s capacity restrictions and lower exports, and signs of regional inventory tightness supporting market sentiment.

Pricing, inventory trends

LME aluminium prices averaged $3,106/t in the week ended 09 January, up $122/t or 4% w-o-w. Prices opened the week at around $3,051/t and strengthened mid-week, reaching $3,112/t, and closed the week at $3,163/t.

Meanwhile, LME aluminium inventories dropped 2.3%, settling at 502,065 t w-o-w from 513,625 t in week 2.

Factors impacting prices

Aluminium prices gained w-o-w as supply-side tightness outweighed mixed demand signals. Market sentiment was supported by China’s strict enforcement of its 45 mnt smelting capacity cap, limiting incremental supply amid improving domestic consumption. Reduced Chinese exports, down sharply y-o-y, further tightened global availability. Delays and higher costs in overseas capacity expansion, particularly in Indonesia, added to supply concerns. Regionally, falling inventories at Japanese ports signalled physical tightness, reinforcing bullish momentum despite a modest rise in SHFE stocks.

Outlook

LME aluminium prices are likely to stay supported as global supply remains constrained by China’s capacity limits and slower overseas expansions. Declining inventories and reduced export availability may offset demand uncertainties, keeping prices firm with upside bias in the near term.

Leave a Reply