- Early rally fades on profit-taking despite tight concentrate signals

- Stocks stable on LME, SHFE/LME ratio fluctuates close to 7.6

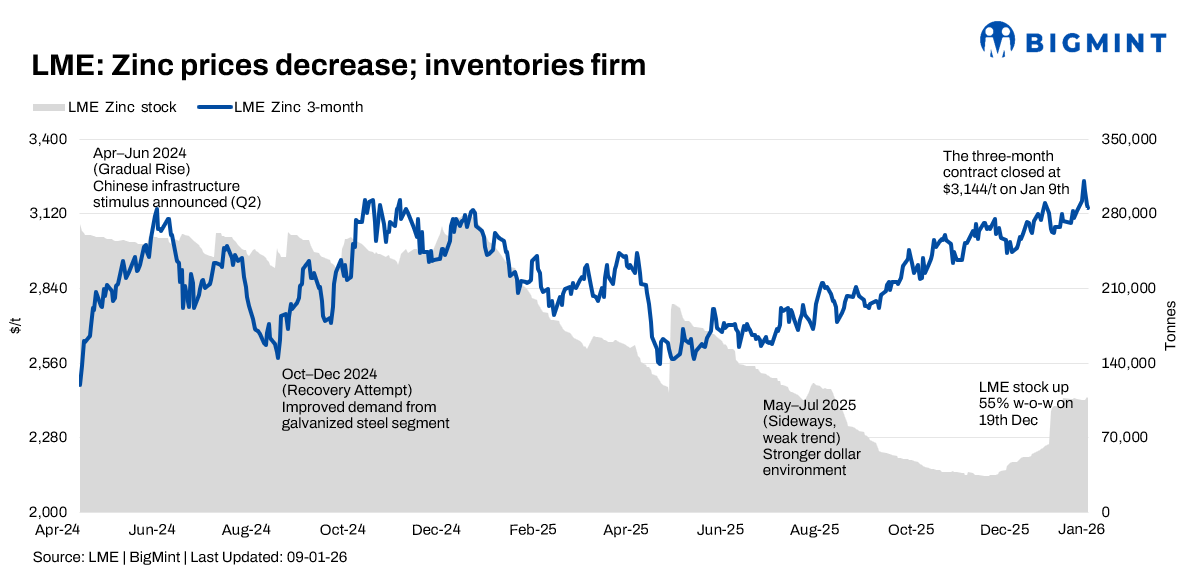

LME zinc prices ended the first full trading week of January on a weaker note after an early rally ran out of steam, as stable inventories and a closed import arbitrage limited fresh upside. The cash contract opened around $3,128/t on 5 January, consolidated near $3,165/t in the early part of the week, and briefly touched $3,208/t on 7 January before sliding to close at $3,101/t on 9 January, marking a weekly decline of 0.8%. The three-month contract mirrored the move, easing to $3,144/t after peaking at $3,242/t, with prices holding just above recent technical support.

LME performance and market sentiment

Market participants attributed the mid-week pullback to profit-taking after the contract tested multi-week highs.

A zinc trader said the rally lacked follow-through buying as “physical premiums remain steady and there is no clear drawdown signal from exchange stocks yet.” Despite the dip, sentiment stayed broadly constructive, underpinned by ongoing concentrate tightness and stable treatment charges.

Inventory trends remain benign

LME zinc inventories showed limited movement through the week, rising marginally from 105,850 t on 5 January to 107,450 t by 9 January, a weekly increase of about 1.5%. In China, social inventories were reported near 125,000 t, while SHFE stocks hovered around 81,000 t, reinforcing the view of a balanced refined market rather than an acute shortage.

China and arbitrage dynamics

On the SHFE, the February 2026 zinc contract traded around CNY 23,100/t, up 1.2% w-o-w. The SHFE/LME ratio fluctuated close to 7.6, keeping import arbitrage firmly closed. Domestic treatment charges remained flat near CNY 1,500/t, signalling persistent concentrate tightness that continues to lend underlying support to prices.

Short-term outlook

In the near term, zinc prices are expected to trade sideways with a soft bias, with support seen near the $3,080-3,100/t range on the LME. Any meaningful upside would likely require a visible drawdown in inventories or a stronger recovery in downstream galvanising demand.

Leave a Reply