- Exports attract sellers as domestic bids stay low

- Tsingshan lowers Jan’26 tender price by RMB 200/t ($29/t)

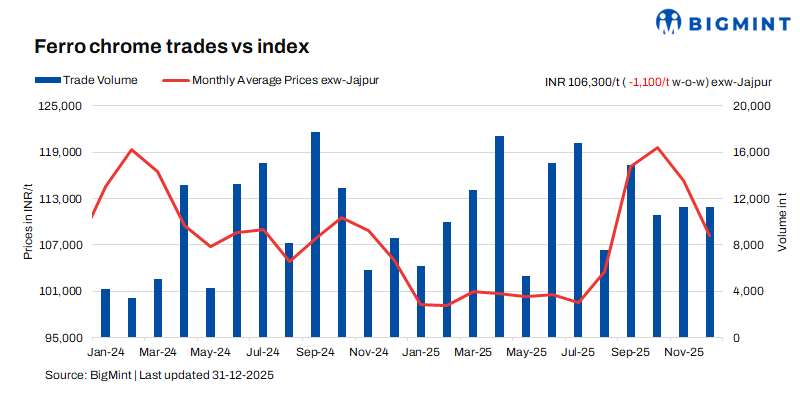

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices witnessed a drop of INR 1,100/t ($12/t) in comparison with the assessment on 24 December. Prices fell as buying activity stayed largely limited in the market, with many participants anticipating a further drop in prices.

As per BigMint’s assessment on 31 December, high-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 106,300/t ($1,181/t) exw-Jajpur. Around 2,300 t of deals were concluded last week in the price range of INR 105,000-106,500/t ($1,167-1,184/t) exw.

Low-silicon high-carbon ferro chrome prices dipped by INR 500/t ($6/t) w-o-w to INR 110,600/t ($1,229/t) exw-Jajpur. Around 800 t of trade was finalised for it in INR 110,000-112,000/t ($1,222-1,245/t) exw price bracket. Meanwhile, prices held stable w-o-w for low-carbon (C:0.1%) ferro chrome at INR 207,500/t ($2,306/t) exw-Durgapur.

Market recap (25-31 December)

Firm offers limit price correction: The Indian ferro chrome market remained cautious last week as key domestic buyers stayed away from the spot market. Limited buying interest was mainly driven by expectations of a price correction, largely due to unsold volumes in the recent auctions by Vedanta-FACOR and OMC. Despite this, sellers largely held firm to their offers and were unwilling to conclude deals below INR 106,000/t ($1,178/t) exw.

In the export market, slightly improved realisations were reported, prompting some producers to divert material overseas rather than accepting lower domestic bids. As a result, market activity remained subdued, with participants closely monitoring demand signals before taking fresh positions.

China market update: Tsingshan reduced its January 2026 ferro chrome tender price by RMB 200/t ($29/t) m-o-m to RMB 8,195/t ($1,172/t) DAP.

The chrome ore market stayed largely stable, underpinned by steady supply from major producers such as South Africa. However, volatility in freight rates added pressure on imports, while expectations around potential international carbon tariff adjustments led traders to optimise inventories without causing any immediate price impact. Firm coke prices continued to offer cost-side support, though easing domestic chrome ore availability reduced smelting cost pressure. Overall sentiment remained cautious on subdued trading activity.

On the demand side, steady stainless steel output and cautious buying limited price movements. Automotive steel demand supported low- and medium-carbon ferro chrome, while weak construction activity capped premiums for high-carbon grades. Although procurement from new energy battery producers increased, volumes remained insufficient to significantly influence market dynamics.

Indian stainless steel market trends: Stainless steel prices for 304 grade HRC edged up by INR 2,000/t ($22/t) w-o-w to INR 184,000/t ($2,045/t) exw-Mumbai. The market showed mixed trends across flats and longs. Flat products strengthened, supported by firm global cues, rising nickel prices, and higher raw material costs, with prices nearing March 2025 levels. Supply constraints following Indonesian production curbs and a late-December price hike by a leading producer further supported sentiment.

In contrast, the finished longs segment remained subdued on weak domestic demand, prompting mills to focus on inventory liquidation rather than fresh output. Export activity stayed slow due to year-end holidays, though enquiries are expected to improve as markets reopen. Globally, cautious demand prevailed despite a sharp rally in LME nickel driven by Indonesian supply concerns. Flats are likely to stay firm, while longs may remain under pressure.

Outlook

Ferro chrome prices in the coming week are expected to stay largely stable.

Leave a Reply