- Sponge iron prices increase by INR 290/t w-o-w, pig iron jumps INR 1,100/t

- Semis, finished steel prices increase by INR 750-800/t w-o-w

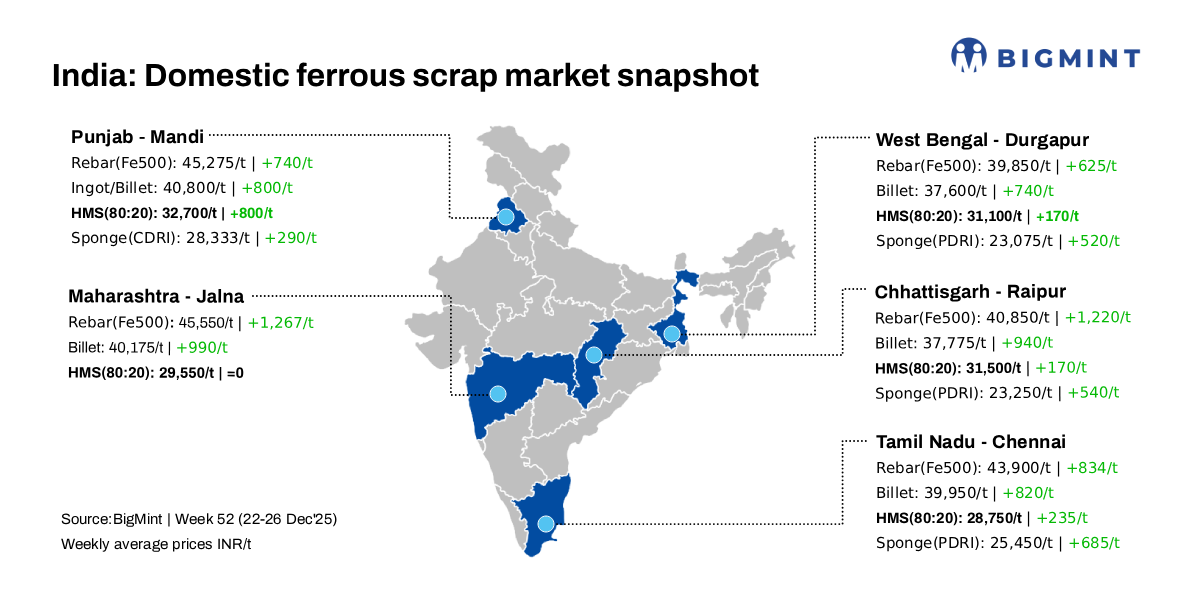

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 200/tonne (t) d-o-d to INR 36,000/t DAP on 26 December 2025.However, the index surged by INR 800/t w-o-w as steel demand improved.

Scrap prices in Mandi Gobindgarh, India’s leading secondary steel hub, recorded a sharp weekly rise, supported by improved buying activity from local mills. Prices of semi-finished and finished steel products increased by around INR 750-800/t during the week, reflecting stronger market sentiment.

The uptrend was further reinforced by reports of an anti-dumping duty imposed on imported Chinese electrical steel and a fresh finished steel price hike announced by a major primary producer. These developments have lifted price expectations among market participants and spurred active procurement in the raw material segment.

According to local steelmakers, market sentiment for the coming month appears moderately positive, contingent on sustained steel demand and stable buying momentum in the secondary sector.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained flat d-o-d at INR 28,600/t (DAP). Meanwhile, prices increased by INR 290/t on a weekly basis in the region.

Similarly, steel-grade pig iron prices in Ludhiana rose by INR 300/t d-o-d to INR 36,500/t (DAP), while weekly prices significantly increased by INR 1,134/t amid improved buying activity in the region.

Steel market

Semi-finished steel prices in Mandi Gobindgarh rose by INR 200/t d-o-d to INR 41,000/t (DAP), while ingot prices across major production hubs strengthened by INR 100-400/t over the same period. Ingot prices in Jaipur jumped by INR 400/t today, marking the largest single-day increase observed across India.

Rebar (Fe 500) prices in Mandi Gobindgarh improved by INR 200/t d-o-d to INR 45,500/t ex-works, supported by moderate-to-strong buying interest and a steady demand trend in today’s trading session. On a weekly basis, rebar prices have risen by around INR 750/t in the region.

Overview of others market

Hyderabad: IF-route 500Fe rebar prices remained marginally supported, mainly due to an increase in semi-finished steel prices, particularly billets. However, buying activity stayed moderate amid cautious demand. Prices hovered in the range of INR 42,000-42,500/t ex-works. Meanwhile, sponge iron and scrap prices were supported by positive sentiments and firm pricing in neighbouring markets.

Alang: As per BigMint’s assessment, Alang’s ship-breaking melting scrap prices rose INR 100/t d-o-d on 26 Dec’25 to INR 31,600/t ($352/t) ex-yard for HMS (80:20). Improved buying from Bhavnagar mills and steady demand in the semi-finished and finished steel segments supported the uptick. As per weekly basis HMS(80:20) scrap prices in Alang rose by INR 425/t.

The majority of ships currently stationed at the Alang yard comprise oil tankers and LNG vessels, with an estimated total of around 30-35 vessels.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,700-5,100/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $318/t, approximately INR 30,890/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 31,000/t DAP. Indicative prices of shredded from Europe stood at $347-$348/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,550/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply