- Muted demand keeps prices steady despite softer seaborne cues

- International market weakness continues to weigh on sentiment

Indian portside prices of Indonesian thermal coal remained largely stable on a week-on-week basis in the week ended 26 December, as subdued spot buying activity limited price discovery across major grades. According to BigMint’s latest assessments, 5,000 GAR coal was unchanged at INR 7,200/t at Kandla and INR 7,100/t at Vizag. Prices for 4,200 GAR softened marginally by INR 100/t, assessed at INR 5,700/t at Kandla and INR 5,600/t at Vizag, while 3,400 GAR coal remained steady at INR 4,500/t at Navlakhi. The broadly flat trend reflects cautious procurement strategies adopted by buyers amid comfortable supply availability.

Freight market dynamics

Freight rates declined further during the week, helping ease landed cost pressures and lending support to portside prices despite weaker international coal benchmarks. BigMint assessed Supramax East Kalimantan-Navlakhi freight at $12.91/dmt, down $0.85/dmt w-o-w. Softer freight partially offset the decline in FOB prices, preventing sharper corrections in Indian portside valuations.

Portside inventory situation

India’s portside thermal coal inventories increased 1.8% w-o-w to 13.31 mnt in the week ended 19 December, compared with 13.07 mnt in the previous week. However, the rise in aggregate stocks masked significant internal movements, as stock build-ups at select ports were counterbalanced by sharp drawdowns at others. This indicates inventory redistribution rather than net accumulation, driven by uneven vessel arrivals and active evacuation at ports with elevated stock levels.

Power sector stock position

Coal inventories at Indian power plants declined to 54.67 mnt as of 25 December, from 55.16 mnt in the prior week, translating to around 18 days of consumption cover. While overall stock levels remain adequate, 14 power plants continue to operate in the critical category, largely due to logistical bottlenecks and coal quality constraints rather than an absolute shortage of fuel.

Seaborne market trends

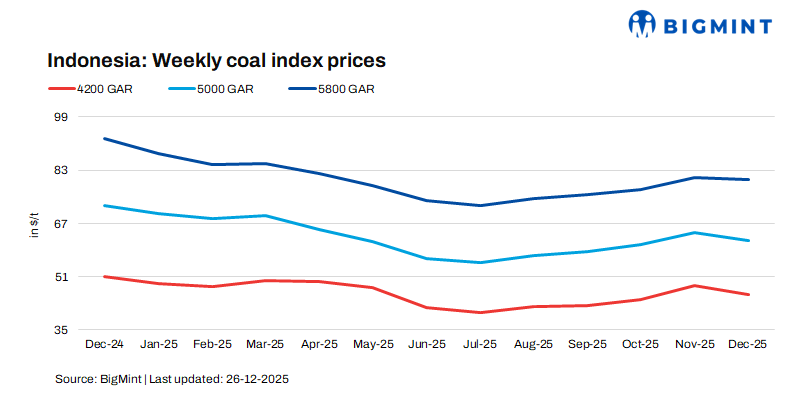

In the wider seaborne market, Indonesian thermal coal prices softened on a week-on-week basis, as exporters lowered offers to accelerate inventory liquidation amid weakening demand from key Asian importers. Prices edged up marginally by $0.03/t for 5,800 GAR, while 4,200 GAR declined by $0.44/t and 3,400 GAR by $0.55/t, reinforcing the bearish undertone prevailing in the international market.

Market outlook

Indian portside prices are expected to remain muted, as ample inventories and weak seaborne sentiment cap upside, while lower freight rates and steady evacuation provide support. Near-term direction will hinge on inventory normalization, Indonesian FOB price trends, and post-year-end demand recovery.

Leave a Reply