- Mills continue to seek cargoes for late Jan, early Feb deliveries

- Sellers hold bullish stance on tighter supply, high collection costs

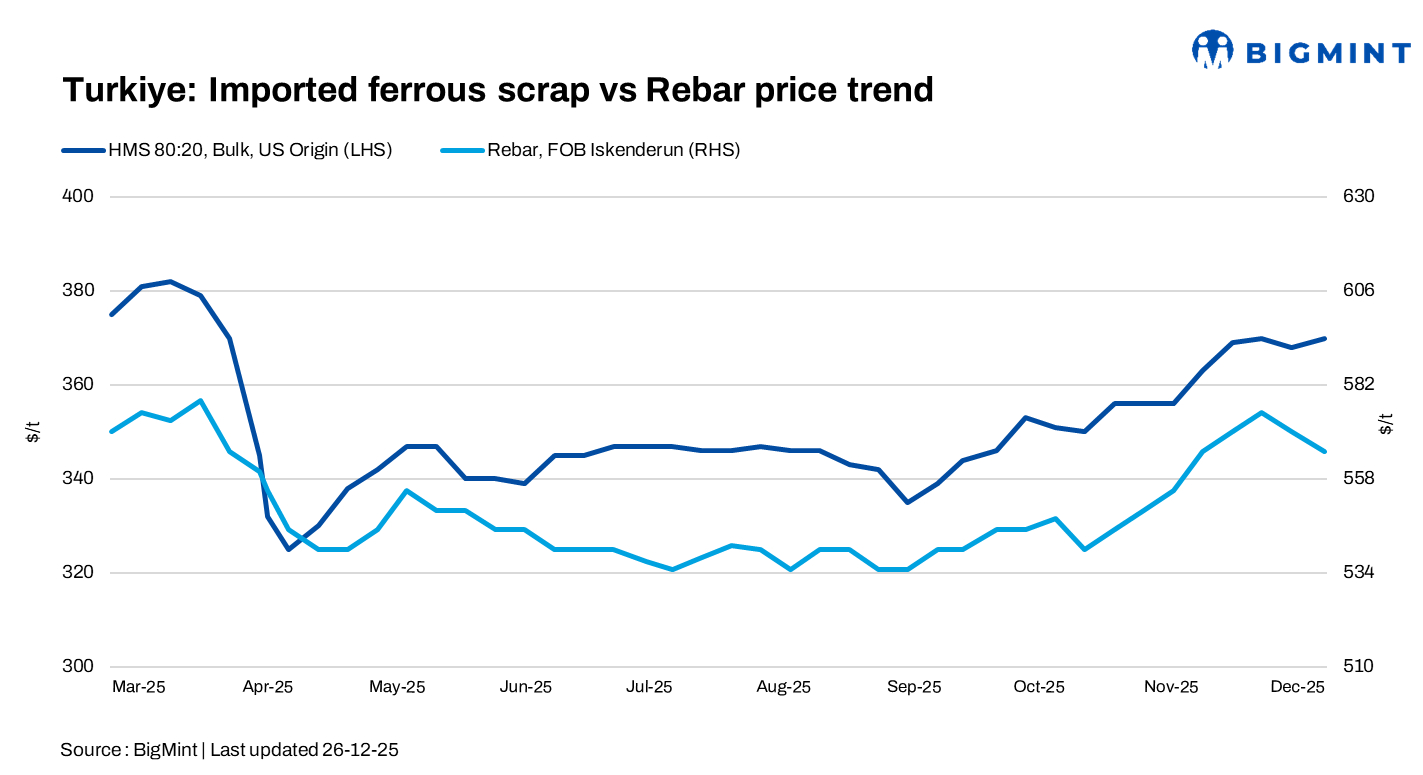

Turkish deep-sea imported scrap prices increased marginally w-o-w on 26 December. Despite overall quiet market conditions, participants highlighted that deal activity increased ahead of the Christmas holiday period, with several transactions reportedly concluded earlier in the week. Additionally, sellers kept offers firm amid limited scrap availability during the winter.

Price assessments

- US-origin bulk HMS 80:20 was assessed at $370/t CFR Turkiye, up $2/t w-o-w.

- HMS 80:20 from the US East Coast was assessed at $343/t FOB, up $5/t w-o-w.

The scrap-to-rebar spread hovered around $190-195/t, with rebar export offers at $560-565/t FOB.

Market commentary

Market sentiment in Turkiye remained mixed. Sellers maintained a bullish stance amid tighter supply and elevated collection costs in Europe, reportedly at EUR 270/t ($318/t) against EUR 260-265/t ($306-$312/t) at the start of December. EU sellers closely monitored the strengthening euro, which supported higher offers, while Turkish mills continued to seek cargoes for late January and early February shipments.

A market participant noted that demand was relatively low due to winter conditions, but downward pressure on prices was limited. Imported scrap cargoes remained attractive to Turkish mills amid elevated billet prices from China and Indonesia. However, mills remained cautious, hesitant to commit amid weak downstream demand and limited activity in the rebar market.

Domestic market updates

In the downstream market, some Turkish mills reportedly pushed up rebar offers despite seasonally weak demand, reflecting a cautious attempt to offset rising costs.

Outlook

Imported scrap prices in Turkey are expected to remain largely stable near $370/t CFR in the rest of the month and in early January, supported by tight supply, firm collection costs, and cautious buying from mills. Seasonal factors and ongoing winter conditions may limit immediate demand, though interest is likely to pick up toward late January as mills prepare for early-year shipments. Participants will continue to monitor exchange rate movements, global billet prices, and European supply conditions for potential price direction.

Leave a Reply