- January scrap price rises expected for higher grades

- Deep-sea US-origin HMS 80:20 falls to $341/t

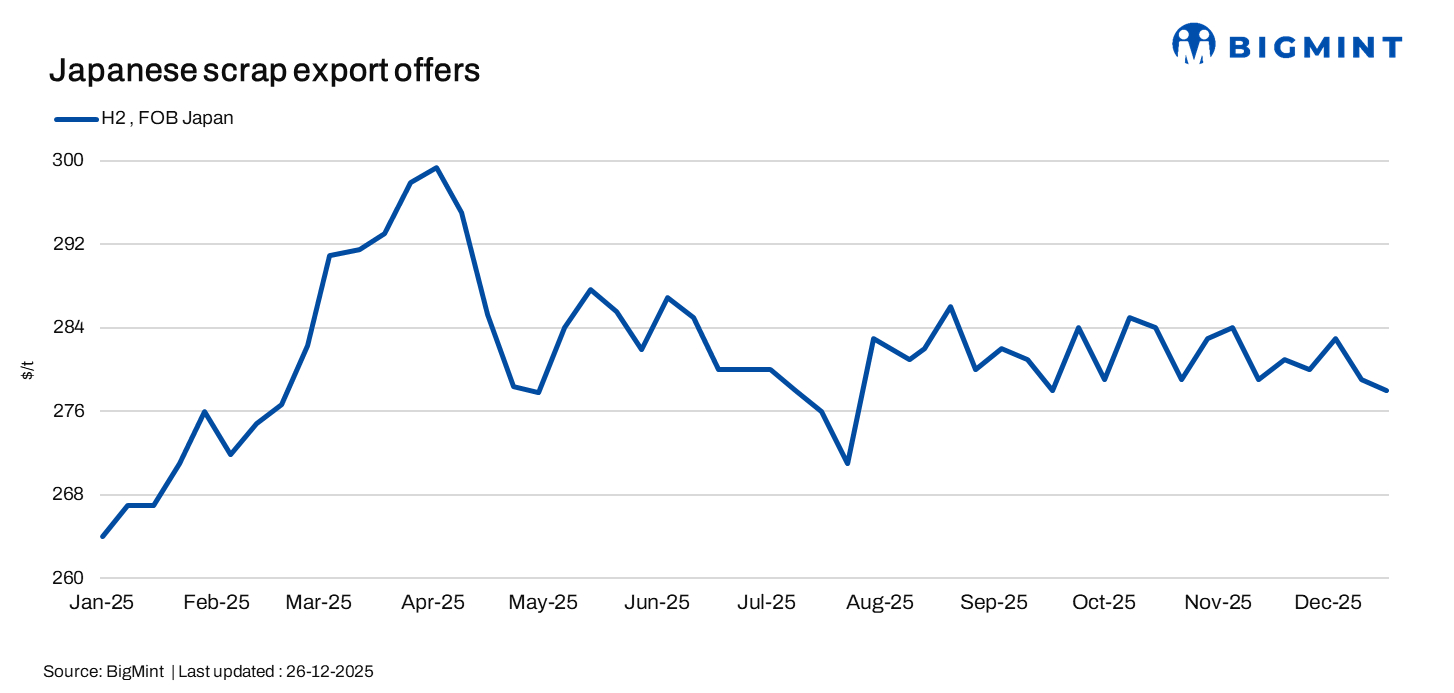

Japan’s H2 scrap prices eased ahead of year-end holidays, with limited activity and stable offers, while Tokyo Steel cut rates at select plants. In contrast, US domestic and export scrap markets strengthened, with January price rises expected amid tight supply and restocking.

Japan scrap prices ease amid year-end slowdown

BigMint assessed Japan’s H2 scrap at JPY 43,600/t ($279/t) FOB Tokyo Bay, down JPY 250/t w-o-w. H2 offers to Vietnam were $325-335/t CFR, with bids below $320/t, as market activity remained limited ahead of year-end holidays.

A mill participant commented, “There isn’t much movement before the holidays. Offer levels are mostly unchanged, though deals done at lower levels.”

Tokyo Steel revised its scrap purchase prices effective 25 December 2025, cutting rates at Tahara and Okayama while keeping other plants unchanged. Post-revision, H2 scrap prices range from JPY 39,500/t to JPY 44,500/t across its facilities.

Deep-sea bulk scrap prices fell, with US-origin HMS 80:20 at $341/t CFR East Asia, down $5/t w-o-w, as the market remained slow ahead of the holidays.

US scrap dealers push for January price hikes amid tightening supply

The US scrap market strengthened as exporters prepared for January restocking, supported by tight domestic supply and rising global demand for high-quality grades. Recent buying from Turkiye further boosted US-origin scrap prices, particularly for bulk HMS 80:20 and shredded grades, adding upward pressure on offers.

FOB assessments (US East Coast, bulk)

HMS 80:20 – $343/t, up by $4/t w-o-w.

Shredded – $363/t, up by $4/t w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

Turkiye – up by ($2/t) w-o-w at $370/t.

Vietnam – stable w-o-w at $344/t.

Bangladesh – up by ($4/t) w-o-w at $360/t

Outlook

Japan’s scrap market is expected to remain quiet and rangebound during the year-end holidays, with limited activity and stable offers. In contrast, the US market is likely to stay firm into January, driven by strong export demand, ongoing supply tightness, and anticipated mill restocking, which could push prime grades higher by $10-20/t and lower-quality grades by $20-30/t.

Leave a Reply