- Ample inventories and muted demand are capping price upside

- Easing freight are sustaining a weak market tone

Indian portside prices of Indonesian thermal coal remained unchanged week-on-week in the week ended 19 December, despite a recent increase in Indonesia’s benchmark HBA prices. The stability reflects ample inventories across calorific segments, subdued spot buying, and a lack of urgency among end-users. As a result, upstream benchmark gains failed to transmit into portside realisations.

Price assessment and trading activity

According to BigMint’s latest assessments, prices across key grades were unchanged due to muted market participation. Prices of 5,000 GAR was reported at INR 7,200/t at Kandla and INR 7,100/t at Vizag, 4,200 GAR grade was reported at INR 5,800/t (Kandla) and INR 5,700/t (Vizag), while 3,400 GAR was unchanged at INR 4,500/t at Navlakhi. Market participants reported limited deal flow, with bids consistently trailing offers.

As per market participant, demand remained soft, driven by slower procurement from Indian buyers and the near absence of Chinese buying interest. Indian consumers, supported by comfortable stock positions, continued to adopt a wait-and-watch approach. Consequently, bid levels weakened across grades, particularly for lower-CV material.

FOB pricing and seller behavior

FOB East Kalimantan prices reflected the softer sentiment. As per market sources for 3,400 GAR, prior-week deals were concluded at $31.5-32/t, while current bids declined to $30-31/t. In the 4,200 GAR segment, offers hovered at $46-47/t, but bids were lower at $44-45/t, highlighting buyer resistance. Indonesian miners, who had earlier withheld supply due to uncertainty around RKAB approvals, have resumed selling, adding near-term supply pressure.

Additionally, uncertainty surrounding a potential Indonesian export tax continues to weigh on sentiment, as no formal decision has been announced, prompting cautious positioning by both sellers and buyers.

Freight market developments

Freight rates softened further, easing landed cost pressures. BigMint assessed Supramax East Kalimantan Navlakhi freight at $13.76/dmt down by $0.24/dmt w-o-w, supporting portside price stability despite softer FOB levels.

Inventory position: Adequate but uneven

India’s portside thermal coal inventories rose marginally to 13.07 mnt in the Week 50, from 13.05 mnt in the previous weekend. While overall stocks remained broadly stable, movements were uneven across ports, with rebuilds at select West Coast ports offset by drawdowns on parts of the East Coast.

Coal inventories at Indian power plants increased to 55.16 mnt as of 16 December, providing around 18 days of consumption cover. However, 15 power plants remain in the critical category, reflecting logistical and supply-quality constraints rather than absolute scarcity.

Seaborne market trend

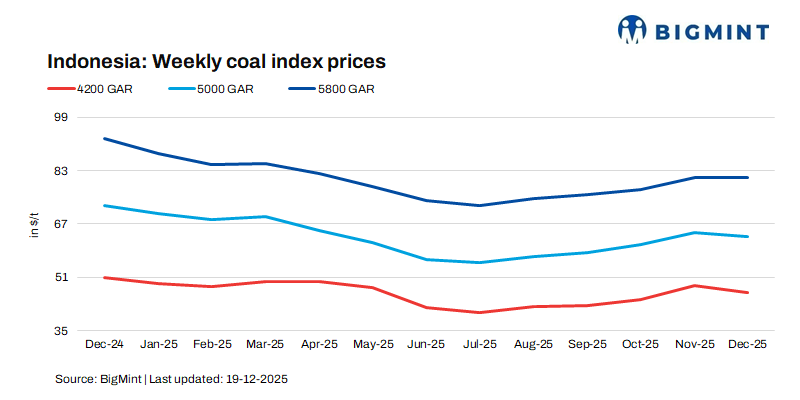

In the broader seaborne market, Indonesian thermal coal prices declined week-on-week as exporters reduced offers to accelerate stock liquidation amid weakening demand from key Asian buyers. Prices fell by $0.98/t for 5,800 GAR, and $0.33/t each for 4,200 GAR and 3,400 GAR, reinforcing the prevailing bearish undertone.

Outlook

Indian portside Indonesian thermal coal prices are likely to stay rangebound with a soft bias. Elevated inventories, subdued Indian and Chinese demand, and lower freight rates should cap upside, while any volatility from Indonesian policy developments or pre-summer restocking is expected to be short-lived in the absence of a clear demand revival or supply shock. Indonesia is planning to impose export taxes to the extent of 1-5% in 2026. Market awaits further clarity and impact on global trade flow.

Leave a Reply