- Demand weakens ahead of year-end

- BDI declines by 223 points w-o-w

Dry bulk freights across key iron ore routes showed mixed trends w-o-w on 19 December, reflecting uneven cargo demand, ample tonnage availability, and cautious chartering activity as the year-end approaches.

Activity softened across most segments, with slower trading and muted vessel demand. The conclusion of some forward freight agreements (FFAs) signalled optimism for early 2026, though ongoing fundamentals still face risks from fleet growth and subdued cargo volumes.

Supramax freights eased due to slower iron ore and minor bulk enquiries from the Indian east coast, coupled with comfortable vessel availability in the Indian Ocean. Charterers adopted a wait-and-watch approach amid softer steel demand in China, limiting fresh fixtures and keeping downward pressure on rates.

Capesize freight sentiment remained cautious, as steady but unaggressive iron ore shipments in the Pacific met improving tonnage availability, limiting rate upside amid muted Chinese mill restocking. In contrast, Atlantic freights received moderate support from tighter vessel supply and ongoing long-haul cargoes, though overall gains were capped by cautious chartering activity.

China’s steel output slumped in November, hitting multi-year lows even as iron ore imports surged to potentially record levels — a paradox indicating stockpiling and restocking behaviour rather than immediate steel demand growth.

Notably, some commercial disputes have affected iron ore shipping, with some vessels stuck at Chinese ports due to paperwork/timing issues. This can temporarily disrupt freight patterns and port turnaround times.

Route-wise updates

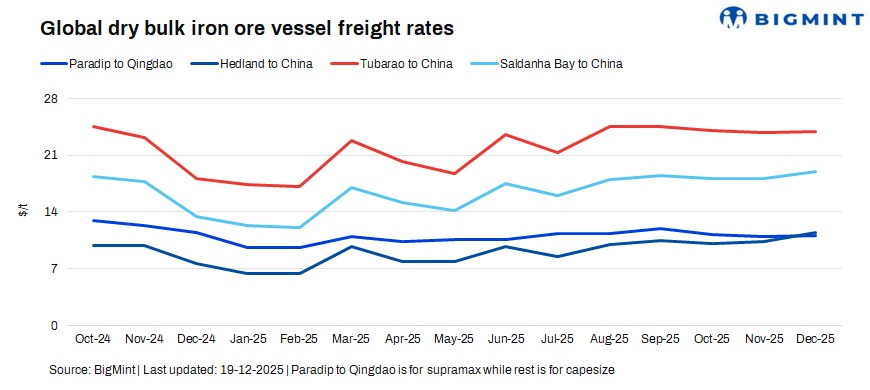

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China fell by $0.4/dry metric tonne (dmt) w-o-w to $10.6/dmt on 19 December.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched down by $0.5/dmt w-o-w to $10.5/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments inched up by $0.1/dmt w-o-w to $23.1/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao decreased by $0.28/dmt w-o-w to $17.72/dmt.

Market highlights

- Baltic index drops w-o-w: The Baltic Exchange’s dry bulk index (BDI) declined by 223 points this week to 2,071 as of 18 December. The Capesize segment slipped 252 points to 3,675, while the Panamax index dropped 335 points to 1,389, and the Supramax index inched down 129 points to 1,258. The BDI declined w-o-w due to broad-based weakness across vessel segments, led by Panamax and Supramax losses amid slower coal and grain cargo demand, easing seasonal trade activity, and rising vessel availability. Capesize rates also softened on reduced iron ore chartering and cautious buying from Chinese steel mills, collectively weighing on overall freight sentiment.

- Brent crude futures fall w-o-w: Brent crude oil futures declined by around $1.48/barrel (bbl) w-o-w to $60.2/bbl for February 2026 contract on 19 December 2025 from $61.68/bbl on 12 December. Brent crude futures fell w-o-w on concerns over slowing global demand growth, particularly from China, alongside expectations of ample supply. Production discipline showed signs of easing, and inventories remained comfortable, keeping downward pressure on prices.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange closed at RMB 784/t ($111/t) on 19 December, down by RMB 20/t ($2.8/t) w-o-w. DCE iron ore futures declined w-o-w amid a weaker steel demand outlook in China, as falling steel margins and subdued downstream consumption weighed on mill buying interest, while ample port inventories and cautious market sentiment added further pressure on prices.

Outlook

Iron ore freights are expected to remain stable or soften slightly, as the year-end slowdown, subdued Chinese steel demand, and comfortable vessel availability continue to cap upside across most routes.

Leave a Reply