- Global nickel surplus expected to persist into 2026

- Elevated inventories continue to cap price recovery

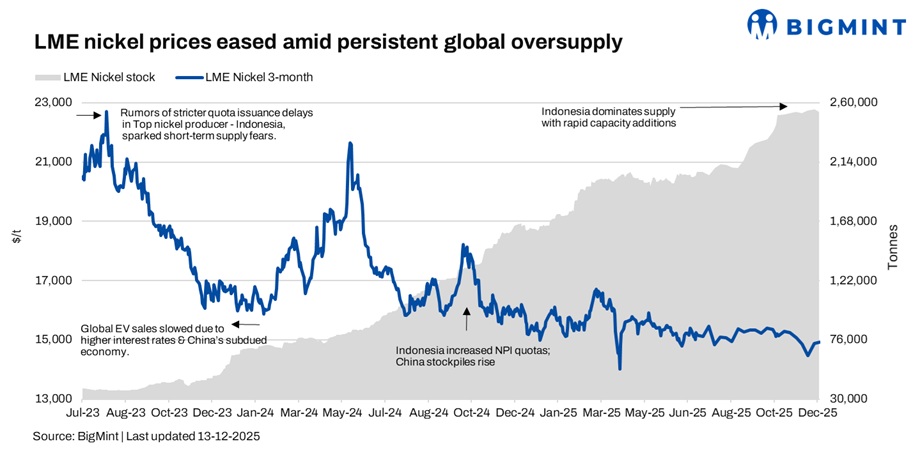

LME nickel prices edged lower this week, as persistent oversupply weighed heavily on sentiment. The benchmark three-month contract closed at $14,605/t on 12 December, down 2 % from $14,920/t last week.

LME nickel inventories were remained steady, ending the week at 253,032 t, range-bound compared to 253,116 t a week earlier, amid ample global availability that continues to suppress price recovery despite occasional short-covering

Market updates

Nickel prices remain capped by global surplus

Nickel prices remain capped by a persistent global surplus, which continues to be reflected in rising exchange inventories. LME-tracked stockpiles have been building steadily for nearly two years and are now at their highest levels in over four years, highlighting excess availability in the Class 1 nickel segment. Increased refining of surplus feedstock into deliverable Class 1 metal, supported by fast-track approval of new brands, has led to greater inflows into LME warehouses. China and Indonesia have emerged as key contributors, with China’s refined nickel exports rising sharply year-on-year and Indonesian cathode shipments surging, much of which has been absorbed by LME stocks. Combined with Indonesia accounting for around 60% of global nickel output through expanding NPI and HPAL capacities, the imbalance between supply growth and demand from stainless steel and batteries is expected to persist into 2026, limiting any meaningful upside in prices.

Nickel eases ahead of fed meeting

Nickel market sentiment turned cautious on 10 December ahead of the US Fed FOMC meeting, with bearish positioning dominating as SHFE drifted lower amid rangebound trading. Jinchuan premiums edged higher at RMB 5,050/t ($715/t) but broader tone stayed guarded on China-US trade discussions and rate path uncertainty, keeping short-term fluctuations contained within recent ranges.

Outlook

Nickel prices are expected to be unde, as the market continues to grapple with excess supply and subdued macroeconomic cues. While consumption from stainless steel and battery sectors remains intact, it is insufficient to absorb ongoing supply additions, particularly from Indonesia. Elevated exchange inventories and cautious investor sentiment are likely to prevent any sustained price recovery. However, potential policy interventions or supply-side disruptions in Indonesia could act as a key risk factor, limiting sharp downside movements.

Leave a Reply