- DRC peace deal in early-Dec’25 offers limited supply relief

- Disruptions in Myanmar, Nigeria further squeeze supply

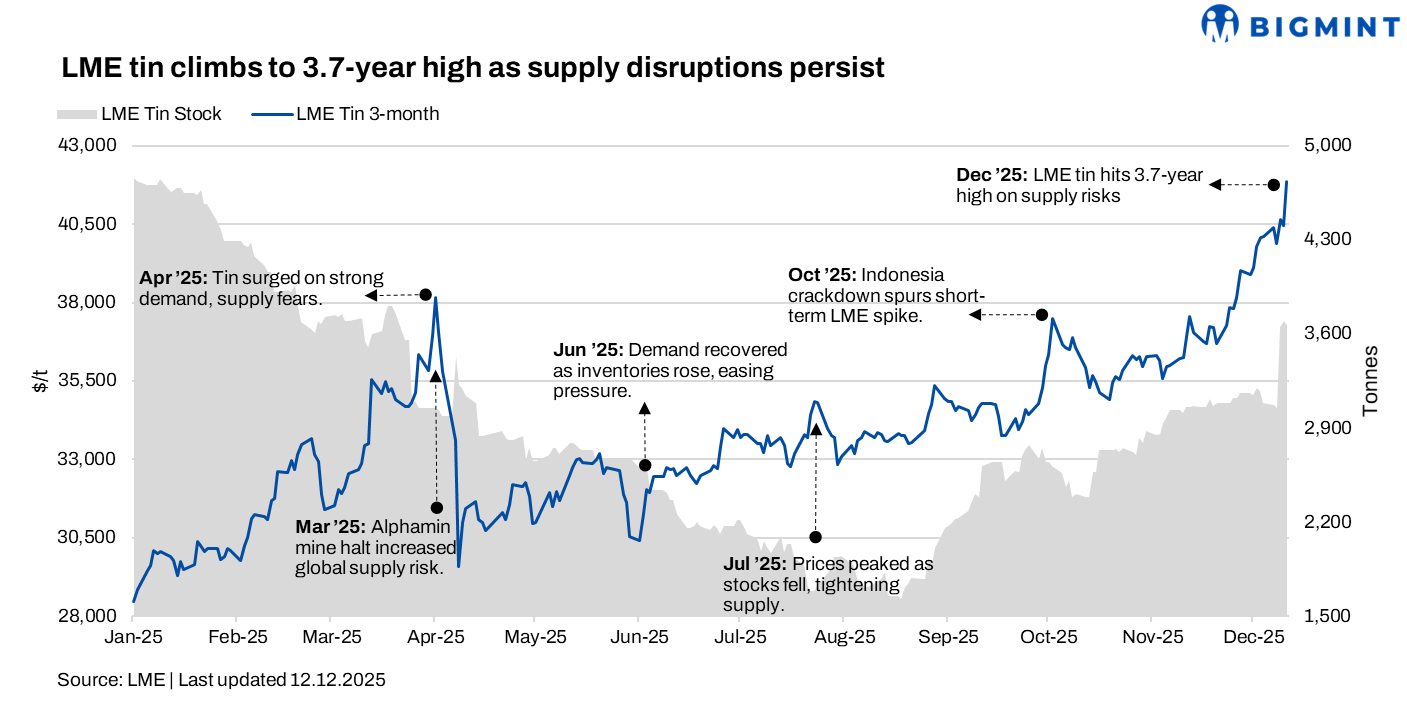

Tin prices on the London Metal Exchange (LME) surged to a 3.7-year high level in the week ended 12 December (week 50), supported by the tight supply, low inventories, and geopolitical risks in key producing regions such as DRC, Nigeria, and Myanmar. Operational disruptions, coupled with cautious downstream demand and strong speculative interest, amplified price gains, while new-demand sectors provided additional support.

Pricing, inventory trends

LME tin prices averaged $40,652/tonne (t) in the week ended 12 December, marking an $1,050/t or 2.7% rise w-o-w from the previous week. The week began with prices at $40,410/t, which inched up to around $40,650/t mid-week and then closed higher at $41,850/t.

Meanwhile, tin inventories at LME-registered warehouses rose 9% to 3,429 t from 3,152 t in the previous week.

What impacted prices?

LME tin surged to a 3.7-year high, last seen in May 2022, driven by persistent supply-side constraints and heightened market speculation. Geopolitical tensions in key producing regions, particularly the Bisie mine in eastern DRC, spurred supply concerns. Although a peace agreement was signed in early December between DRC President Tshisekedi and Rwandan President Kagame, the incomplete disarmament of armed groups and disputes over mineral resource benefits limited its effectiveness. Combined with security risks in Nigeria, operational disruptions at Myanmar’s Wa State mine, and historically low LME and domestic inventories, availability tightened further, pushing up prices.

On the demand side, growth was mixed. Emerging sectors such as AI, semiconductors, and new energy vehicles supported tin consumption, while traditional demand from electronics and home appliances weakened. Low restocking activity and cautious downstream sentiment meant that demand provided only limited support.

Overall, tin prices climbed up, as supply disruptions and low inventories dominated market dynamics, while speculative trading and macro tailwinds amplified gains. Despite surging prices, the market remains sensitive, with potential volatility if supply conditions stabilise or capital exits the market.

Outlook

LME tin is expected to remain supported near multi-year highs due to tight supply, low inventories, and geopolitical risks in DRC, Nigeria, and Myanmar. However, weak traditional demand, cautious downstream restocking, and potential stabilisation after the DRC peace deal may cap further gains. Any easing of disruptions or reduced speculative interest could trigger short-term corrections.

Leave a Reply