- Pacific routes supported by tighter tonnage

- Atlantic momentum softens amid weaker demand

Dry bulk coal freight rates to India improved across key Pacific routes, supported by tighter vessel availability, despite a notable drop in fixtures from last week. Conversely, the rates in the Atlantic basin faced downward pressure, with subdued activity and a lack of meaningful fixtures curbing price rises and dampening market sentiment.

“Spot rates have risen due to tight tonnage in the Pacific,” a shipbroker said, noting that charterers with prompt cargoes from Western Australia and Indonesia have had to meet higher offer levels to secure vessels.

Coal freight rates on the Australia-India route firmed this week, although activity remained thin, with just a single reported fixture – significantly fewer than in the previous week, and largely driven by SAIL as the only active charterer. In the domestic steel market, sentiment stayed weak, with prices edging lower amid minimal signs of recovery. Market participants noted that abundant inventories continue to cap demand, limiting any meaningful upside, while buyers remain on the sidelines ahead of mills’ upcoming price announcements.

After a period of firm gains, freight rates on the South Africa-India route fell this week, reflecting a shift in market sentiment. The downturn was partly driven by subdued demand and a growing list of open tonnage, which removed the tightness that previously supported prices. With charterers adopting a more cautious approach, owners were forced to lower expectations, resulting in a noticeable softening of the market.

Although Supramax rates on the Indonesia-India route ticked up this week, activity remained quiet, with no major fixtures and minimal fresh interest from Indian charterers. A Mumbai-based shipbroker noted that “market sentiment remains firm, hire rates are high, and there’s no indication of offer levels easing,” adding that trading visibility on the Indonesia-China route was limited.

Another source told BigMint, “Asia-Pacific Supramax freight rates were mixed, with the Pacific market remaining supported by tight prompt tonnage and nomination pressure on charterers. In contrast, activity in the Indian Ocean stayed relatively sluggish due to muted enquiry and limited fresh fixtures.”

Rising fuel costs add upward pressure to freight rates: Bunker prices have risen recently, adding upward pressure on vessel operating costs and contributing to firmer freight market sentiment. Higher fuel costs typically prompt owners to lift their rate ideas, especially on longer voyages, while some also reduce operating speeds to manage consumption, tightening effective tonnage supply. As a result, even in markets with modest demand, rising bunkers can support or accelerate freight rate increases, particularly on fuel-sensitive trades.

Demand-supply dynamics show tighter tonnage & stabilizing market: Demand-supply dynamics in the vessel freight market saw a shift this week – tighter tonnage availability in the Pacific – especially for prompt cargoes loading from Australia and Indonesia – lent support to rates, even though enquiry remained modest. In the Atlantic, tonnage lists remained relatively balanced and export activity kept a steady pace, helping to sustain freight levels. Overall, the market appeared more stable than recent weeks, with both basins showing only moderate softening despite uneven demand.

Route-wise updates

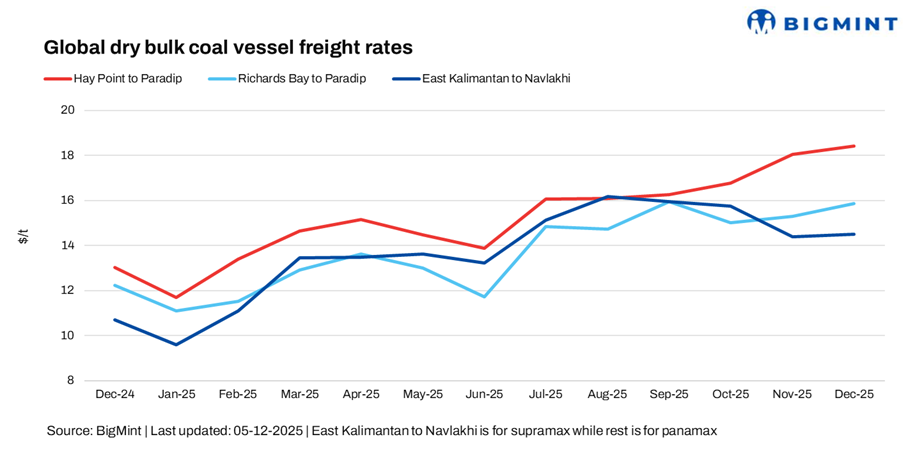

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India rose w-o-w by around 0.37/dry metric tonne (dmt) to $18.44/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged down w-o-w by $0.39/dmt to $15.64/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $14.70/dmt, an increase of $0.20/dmt, w-o-w.

Meanwhile, the Baltic Exchange’s dry bulk index for Panamax and Supramax vessels remained under pressure this week, with the Panamax index falling sharply by around 99 points w-o-w to 1,863 and the Supramax index increasing marginally by 4 points to 1,441. The drop in the Panamax index likely reflects softer demand and abundant vessel availability in key routes, which forced owners to lower rates to secure employment. In contrast, the slight uptick in the Supramax index suggests limited prompt tonnage combined with modest demand for smaller shipments – enough to support rates modestly even as broader dry-bulk sentiment remains subdued.

Outlook

In the coming weeks, freight rates to India are likely to remain stable to modestly firm. The most recent firming of rates has been supported by tighter vessel availability in Pacific supply zones – particularly for prompt tonnage from Australia and Indonesia – along with elevated bunker fuel costs boosting owners’ incentive to fix at higher levels.

Leave a Reply