- Mid/high-CV coal stable; 3400 GAR pressured

- Inventories adequate; freight rates up

Indian portside prices of Indonesian thermal coal held largely unchanged w-o-w as of 05 December 2025, with firmer global benchmarks providing a clear price floor. The steady international outlook discouraged domestic sellers from offering heavy discounts, resulting in muted spot activity and controlled price movements across major ports.

Conflicting market signals: Demand caution vs. Overstock pressure

Market sentiment remained mixed. According to one market participant, China’s recent slowdown may open a window of opportunity for Indian buyers but only if domestic demand strengthens.

Conversely, another trader highlighted growing downside risk for 3400 GAR coal, driven by high port inventories and a noticeable shift toward cheaper lignite. With a lignite auction scheduled for 10 December expected to open at lower price levels buyers are increasingly cautious about committing to fresh Indonesian low-grade cargoes.

Major grades hold firm across Indian ports

BigMint’s assessments showed stable pricing across key Indonesian thermal coal grades, supported by adequate inventories and subdued trading activity. The 5000 GAR grade held at INR 7,200/t in Kandla and INR 7,100/t in Vizag, while 4200 GAR remained unchanged at INR 5,850/t and INR 5,750/t, respectively. The 3400 GAR grade also stayed steady at INR 4,600/t in Navlakhi, with ample stocks limiting any upward movement. Overall, balanced arrivals and weak spot demand kept portside prices firmly range-bound.

Freight rates rise slightly on key Indonesia-India route

Supramax freight rates on the East Kalimantan-Navlakhi route increased by $0.20/dmt to $14.70/dmt, reflecting firmer vessel demand and tightening cargo schedules in the Indian Ocean region.

Portside inventories tick up amid mixed vessel arrivals

Thermal coal inventories at Indian ports edged up to 12.94 mnt in Week 48, from 12.88 mnt a week earlier. Inland-linked ports witnessed strong replenishment, while major coastal discharge ports experienced marginal drawdowns. A mix of uneven vessel arrivals and shifting dispatch patterns shaped the weekly inventory movement.

Power plant stocks improve but critical units persist

Coal inventories at Indian power plants rose to 53.89 mnt as of 04 December, offering around 18 days of consumption cover. Despite this improvement, 13 plants remain in the critical category including units dependent on domestic coal, imported coal, and washery rejects highlighting persistent logistical challenges in the supply chain.

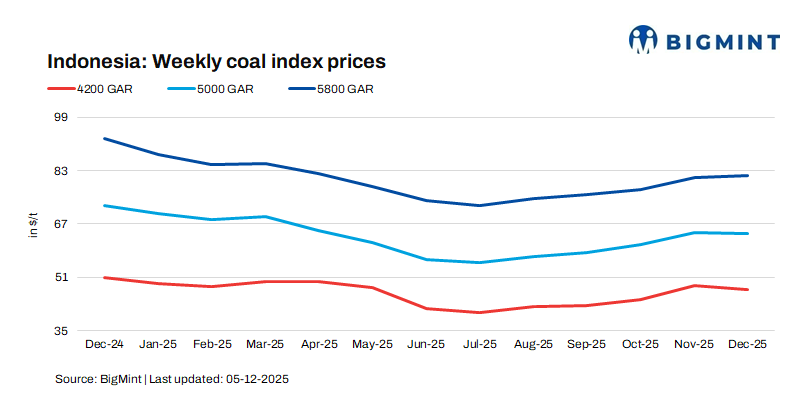

Indonesian seaborne prices slip on softer demand

Indonesian seaborne coal prices registered a week-on-week decline as exporters reduced offers to expedite stock clearance amid weakening buying interest. The 5800 GAR grade dipped marginally by $0.07/t, while the 4200 GAR and 3400 GAR grades saw comparatively sharper decreases of $1.55/t and $0.34/t, respectively. The more pronounced correction in lower GAR grades reflects softer demand from key markets and increased pricing flexibility from suppliers seeking to manage inventories under constrained logistical conditions.

Market outlook: Stability with a downward bias for lower grades

Indian portside prices for mid- and higher-grade Indonesian coal are expected to remain stable, while 3400 GAR may soften due to stronger lignite preference, high stocks, and the upcoming lignite auction. Pricing direction will depend on domestic demand, with subdued Chinese buying and flexible exporter offers improving Indian buyers’ negotiating position.

Leave a Reply