- Softening freights fail to boost trading activity

- Weak demand, ample stocks keep prices stagnant

Indian portside prices of Indonesian thermal coal remained largely unchanged w-o-w as of 28 November 2025. The stability was primarily driven by firmness in global coal benchmarks, which provided a pricing floor and discouraged aggressive discounting in domestic spot transactions.

According to a market participant, price shifts were limited throughout the week, as vessel diversions to China and improved buying activity prevented any meaningful downward correction. However, attempts by domestic traders to lift offers met limited success due to subdued procurement interest, ultimately curbing transaction volumes at higher prices.

Indonesian coal prices stable amid limited trade volumes

BigMint’s assessments reflected consistent price trends across major thermal coal grades at key Indian ports. The 5000 GAR grade held steady at INR 7,200/t in Kandla and INR 7,100/t in Vizag, supported by balanced arrivals and no significant supply shocks.

Similarly, the 4200 GAR grade remained unchanged at INR 5,850/t in Kandla and INR 5,750/t in Vizag, while the 3400 GAR grade was stable at INR 4,600/t at Navlakhi. The absence of aggressive spot buying and the availability of adequate stocks ensured that prices did not deviate from prior levels.

Softening freights fail to boost trading

Freights on the Indonesia (East Kalimantan)-India (Navlakhi) Supramax route declined by $0.40/dmt w-o-w to $14.50/dmt. The continued softening reflects ample vessel supply and muted chartering interest. Lower freight costs typically incentivise imports; however, the benefit was offset by limited demand enthusiasm and trader caution, keeping spot market activity contained despite reduced logistics costs.

Inventory dynamics show regional divergence

India’s portside thermal coal inventories inched up 0.3% w-o-w to 12.88 mnt in Week 47 from 12.84 mnt in Week 46. While stocks were stable overall, the regional distribution was uneven. Select east coast terminals witnessed gains due to improved last-mile movement, whereas several west coast ports saw drawdowns as steady dispatches outpaced arrivals. Notably, strong receipts at Mundra cushioned the aggregate inventory position, masking weakness elsewhere.

Power plant stocks improve but vulnerabilities persist

Coal stocks at Indian power plants rose to 53.72 mnt as of 26 November from 52.89 mnt a week earlier, equating to roughly 18 days of consumption cover. Despite the improvement, 14 plants continue to operate in the critical stock range, with six dependent on domestic coal, six reliant on imported coal, and two consuming washery rejects. This persistent imbalance indicates uneven replenishment pace and underlines structural dependence on both domestic and seaborne supply channels.

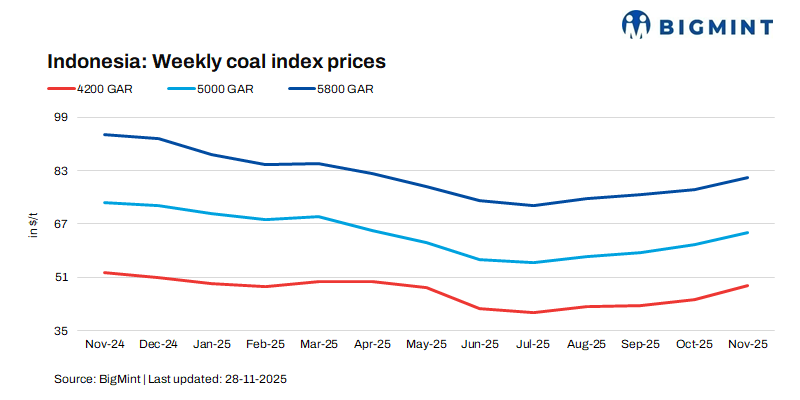

Global market drivers influence Indonesian seaborne prices

Indonesian seaborne coal prices displayed a mixed trend. The 5800 GAR grade edged up by $0.30/t w-o-w, supported by moderate Chinese tenders and weather-related output disruptions in Kalimantan, which constrained supply. In contrast, the 4200 GAR and 3400 GAR grades dipped by $0.48/t and $0.42/t, respectively, reflecting softer demand for lower-calorific coal and exporter flexibility to clear existing stockpiles amid logistical constraints.

Outlook

The Indian portside coal market maintained price stability this week, underpinned by firm global benchmarks and comfortable inventory levels. Nonetheless, the current equilibrium remains susceptible to disruption. Heightened freight volatility, uneven coal procurement by power utilities, fluctuating Chinese buying interest, and the risk of Indonesian supply constraints collectively underline the market’s fragility. Consequently, any significant change in supply conditions or demand momentum could prompt a rapid price adjustment.

Leave a Reply