- Pre-GST stockpiling causes demand vacuum

- Onset of winter halts operations at brick kilns

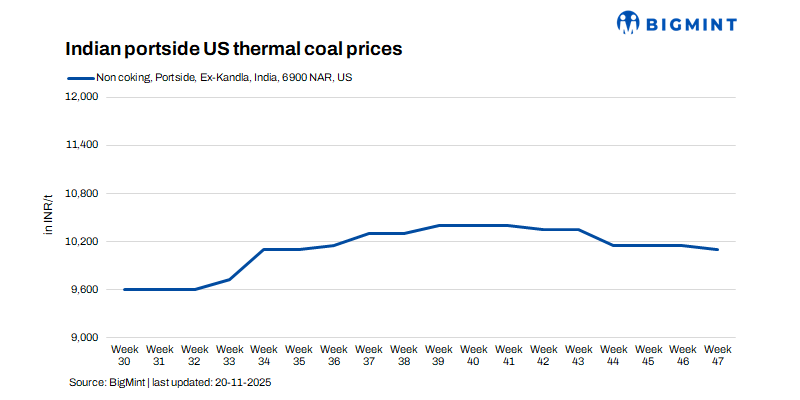

Traders of US thermal coal at India’s Kandla and Tuna ports are staring at severe financial losses, caught in a perfect storm of slowing demand and elevated inventories. This is in stark contrast to the recent bullishness in global prices of US thermal coal, with traders trapped in a localised crisis.

Factors driving demand slowdown, supply glut

- Pre-GST stockpiling: Downstream buyers and brick kilns front-loaded their purchases before the GST on coal was raised to 18%, creating an immediate and severe demand vacuum upon implementation.

- Seasonal shutdown: The onset of winter has halted operations at brick kilns, a key consumer segment, with significant restocking not expected until late February.

- Cement sector independence: The cement industry’s strategic pivot to cheaper, stable alternatives such as Indonesian coal has removed a major potential demand source that traders were counting on to clear inventories.

Traders’ plight reflects global demand slowdown

The situation at the ports is dire, with market participants reporting a staggering 600,000 tonnes (t) of US NAPP coal inventory, with daily offtake rates as low as 4,000 t. This portside paralysis is a reflection of a broader issue, also seen in rising stockpiles elsewhere, such as the 6% y-o-y increase in inventories at South Africa’s RBCT. It demonstrates that underlying physical demand is weak in many regions, and the recent price rally in US thermal coal was narrowly focused on specific grades and origins.

Traders holding high-cost inventory are facing catastrophic losses, caught between their purchase prices and the current market reality. “Short sellers” have emerged, offering material at much lower levels. As per BigMint’s assessment of US thermal coal, older stocks are currently being offered at INR 10,100/t, while fresh stocks are observed to be quoted in the INR 10,300-10,400/t range, which indicates a firming trend in market offers has created an unsustainable pricing environment for those who bought at market peaks.

The impending need to liquidate stock to pay off Letters of Credit (LCs) threatens a wave of distress sales that could wipe out smaller trading firms, a clear sign of a deeply distressed and oversupplied local market. This stand-off highlights the extreme risks faced by merchants when localised demand collapses, even amid seemingly bullish global headlines.

Leave a Reply