- Wide bid-offer gaps, muted sponge iron buying limit trade

- Vessel shortage, strong Chinese buying support FOB values

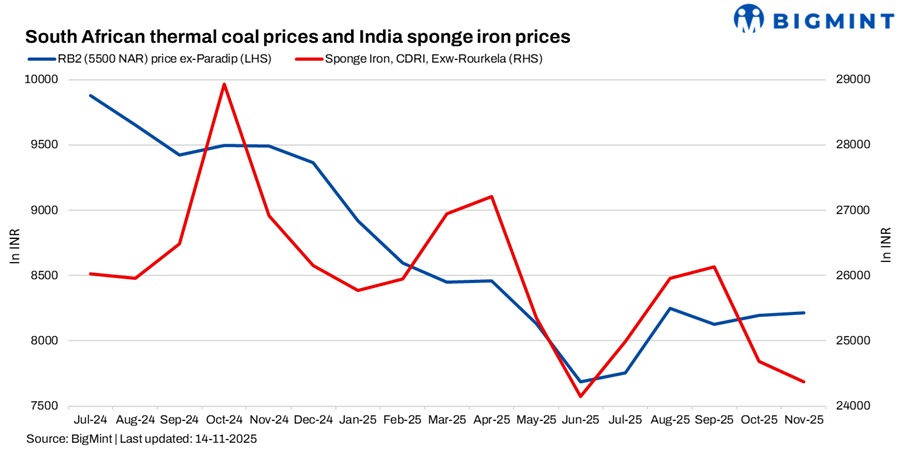

South African RB2 (5500 NAR) portside prices in India rose w-o-w to INR 8,300/tonne (t) at Paradip, INR 8,350/t at Vizag and INR 8,400/t at Gangavaram, up from INR 8,200/t last week. RB3 (4800 NAR) also rose to around INR 7,200/t across major east coast ports. The increase was driven by higher export offers, vessel shortages, elevated February-March forward freights, and stronger Chinese buying. Indonesian export prices firmed up to $75-76/t FOB for RB2 and $60-61/t FOB for RB3, with November-December shipments booked out.

Market sentiment, buying interest

Despite firmer offers, Indian demand remained weak due to a wide bid-offer gap and muted sponge iron procurement. Traders said that there were no major deals, as buyers resisted higher levels. Lower portside inventories — down 3.2% w-o-w to 12.57 mnt — supported offer strength but did not translate into improved buying.

Domestic market signals

BigMint’s C-DRI index (ex-Rourkela) increased by INR 250/t w-o-w to INR 24,500/t. Sentiment improved after anti-dumping duties were imposed on Vietnamese HRC imports, prompting restocking in the semi-finished and finished steel markets.

Domestic coal prices were stable, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. In SECL’s recent auction, limited offered volumes led to active buying and lifted bids by INR 100-200/t as most traders held low stocks.

Outlook

South African portside prices may remain firm in the near term, supported by strong export benchmarks, vessel tightness, and limited near-term availability for November-December loadings. However, Indian buying is likely to stay subdued unless sponge iron demand improves or the bid-offer gap narrows. Any easing in freight or FOB values could stabilise offers through late November.

Leave a Reply