- Chinese market players look to capitalise on potential tariff shifts

- Cheaper coal alternatives, bid-offer gaps weigh on Indian trade

The global fuel-grade pet coke market this week was a story of dramatic divergence, driven by geopolitics, speculative capital and brutal economics. While a major buying spree from China reshaped global sentiment, the Indian market — typically a pillar of demand — found itself frozen in a stalemate, sidelined by soaring costs and price-sensitive buyers.

Chinese gambit: Buying today for a tariff-free tomorrow

The headline story was the aggressive return of Chinese buyers. In a flurry of deals that reset global price expectations, Chinese traders and end-users snapped up multiple cargoes at levels that defied current economics. Transactions for US and Mexican high-sulphur pet coke were concluded at $125-125.50/tonne (t) CFR China, while a cargo of premium low-shot material from the US Gulf Coast fetched a staggering $132/t CFR China. Even anode-grade material from Europe found its way to China at levels around $220/t, demonstrating the breadth and intensity of the demand.

This buying spree is particularly striking because the punitive ~28% import duty on US-origin pet coke remains officially in place. The motivation is not immediate consumption needs but a strategic, forward-looking bet. Key players are gambling that a thaw in US-China trade relations will lead to the removal of these tariffs. By securing supply now, they are positioning themselves ahead of a potential price surge if and when the duties disappear. This sentiment is reinforced by industry intelligence that a major US refiner is building stocks specifically for sale to China, indicating a shared belief in this bullish market direction.

Ripple effects: Freight, global sentiment soar

China’s fervent activity had immediate and severe knock-on effects across the supply chain.

Freights skyrocket: The sudden demand for vessels to load and ship these cargoes pushed ocean freights to multi-month highs. Key routes in Asia saw fixtures concluded at $47-50/t. This created a critical choke point, with shipbrokers warning of a severe shortage of available vessels for November loadings and advising clients to revise freight assumptions daily.

Trader sentiment hardens globally: With China paying $125-132 CFR, sellers’ expectations for all destinations were reset upwards. The market braced for a “quite dramatic” jump in key price benchmarks for December, with talk of increases of “$10 or more.”

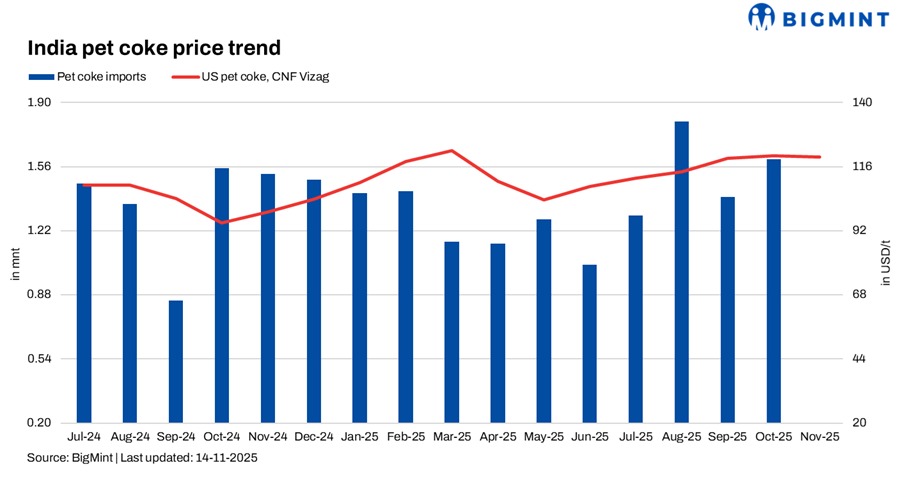

India sees stalemate, with firm offers, weak bids

While the global tide rose, the Indian market was left stranded. The core issue was a fundamental and stubborn mismatch between sellers’ offers and buyers’ bids, exacerbated by the very freights China’s buying had inflated.

Offer side: Bolstered by the high China prints, international traders maintained firm offers to India. Market surveys showed consistent offers in the range of $116-117/t CFR West Coast India (WCI) and $118-119/t CFR East Coast India (ECI). Domestic trading desks also reported firm price ideas, even as underlying indices suggested weaker conditions.

Bid side: Major Indian cement manufacturers, the primary consumers, held an unmovable line. At the start of the week, their bids were firmly lodged at $108-109/t CFR India. This gap of nearly $10/t made a deal impossible. However, after the flurry of Chinese activity, Indian bids improved to $116-117/t levels, but the futility of the situation was highlighted when a bid of $119.50/t from an east coast buyer — a level that would typically clear — was promptly rejected by a seller who had a more profitable outlet elsewhere.

Why Indian buyers will budge

Freight stranglehold: The economics were simply unworkable. Traders said that the all-in cost to ship a cargo to a key Indian port was already $115/t, leaving zero margin at the local bids. The high freight meant the landed cost of cargoes was structurally elevated.

Cheaper coal alternatives: The pressure was compounded by the competing coal market. US coal was offered at a premium, but Indian buyers could source comparable material from other regions in the low $90s. This made pet coke, even at discounted bids, a less attractive option for their energy needs.

Domestic weakness: The sentiment on the ground was uniformly described as “extremely weak,” “subdued,” and “muted.” Feedback from all major cement players confirmed a “wait-and-watch” approach, with no sense of urgency to secure seaborne supply despite the firming global market.

Bottom line, outlook

The week concluded with a clear schism. One major market was buying the future, while India was stuck in the present.

For India, the outlook for November shipments appears bleak. The consensus was that unless local buyers significantly revise their market views, it is doubtful any major November-loading cargoes will be destined for Indian shores. Sellers have no incentive to reduce prices, while alternative markets in China and Southeast Asia offer cleaner, more profitable outlets.

What to watch next?

China’s tariff policy: Any official hint of a relaxation will supercharge Chinese buying, pulling more material away from India. A lack of progress could cool the frenzy.

Freights: Any softening in freights is the most likely key to unlocking Indian parity.

Indian domestic dynamics: A rebound in domestic demand or a shift in the competitive coal market could empower buyers to raise their bids before the global market moves completely out of their reach.

Leave a Reply