- Leading steel mills reduce HRC, CRC prices by INR 750-1,500/t

- Rebar market downtrend continues despite price hike by Tier-1 mills

- Domestic market faces inventory pressure amid festive slowdown

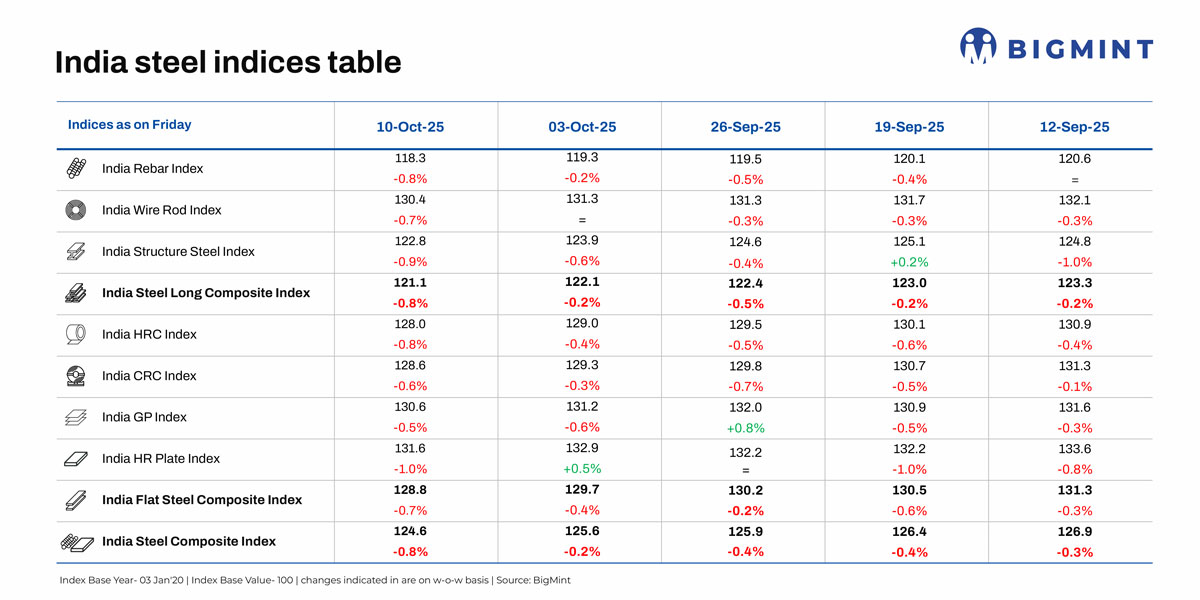

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, edged down by 0.8% w-o-w, as assessed on 10 October 2025. The continued downtrend, with steel prices dropping to 5-year lows, points to the combined impact of an extended monsoon, festive slowdown and inventory pressure in the domestic market.

While the flats composite index inched down by 0.7% w-o-w, the longs index fell 0.8%.

Highlights of price movements

Mills cut HRC, CRC prices: The leading steel manufacturers decreased prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-17/t) for October sales as compared to the list prices of early-September. However, from the net sales prices of end-September, prices were raised by INR 500/t ($6/t) for October.

BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 200/t ($2/t) w-o-w to INR 48,300/t ($544/t) on 7 October against INR 48,500 ($546/t) on 30 September. CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 200/t ($2/t) w-o-w to INR 55,700/t ($628/t) on Tuesday against INR 55,900/t ($630/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

The HRC market remained sluggish as slow demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings. Thin margins, heavy stocks, and the Navratri and Durga Puja holidays further dampened trading activity and delayed recovery prospects.

Mixed trends in rebar market: On a weekly basis, rebar prices in the IF steel market fell in the range of INR 200-1,000/t across regions, as per BigMint assessment. Finished long steel prices experienced a decline w-o-w, primarily driven by selling pressure due to high inventory levels and subdued demand. Sluggish offtake led to an accumulation of stocks, compelling manufacturers to opt for production cuts in various regions. Trade remained confined to fulfillment of immediate needs as buyers stayed cautious amid weak demand.

However, the primary mills increased rebar prices by up to INR 1,000/t $11/t) for early-October deliveries as against levels prevailing in end-September. Post-revision, list prices stood at INR 47,000-48,500/t ($530-546/t) on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month.

In the projects segment, prices opened at INR 46,500-47,500/t ($524-535/t) FOR Mumbai basis for early-October dispatches. Rebar inventories at Tier-1 mills increased by 4% m-o-m in early-October as against inventories in early-September, sources informed.

The BF-IF rebar monthly average price gap stood at around INR 4,000-4,500/t ($45-51/t) in Mumbai. IF rebar holds a dominant 65-70% market share in India.

Outlook

The recent hike in construction steel prices by the Tier-1 mills has extended some support to the trade market. However, volatility is likely to persist. The festive demand recovery in early October has been sluggish, with buyers remaining cautious due to high inventory levels and muted trading sentiment. These factors are weighing on price movements.

However, towards the end of October, a demand revival can be expected as market activity gathers pace after the festive holidays.

Leave a Reply