- Coal India posts y-o-y drop in Sep production, dispatches

- Outlook stays pressured by weak industrial demand

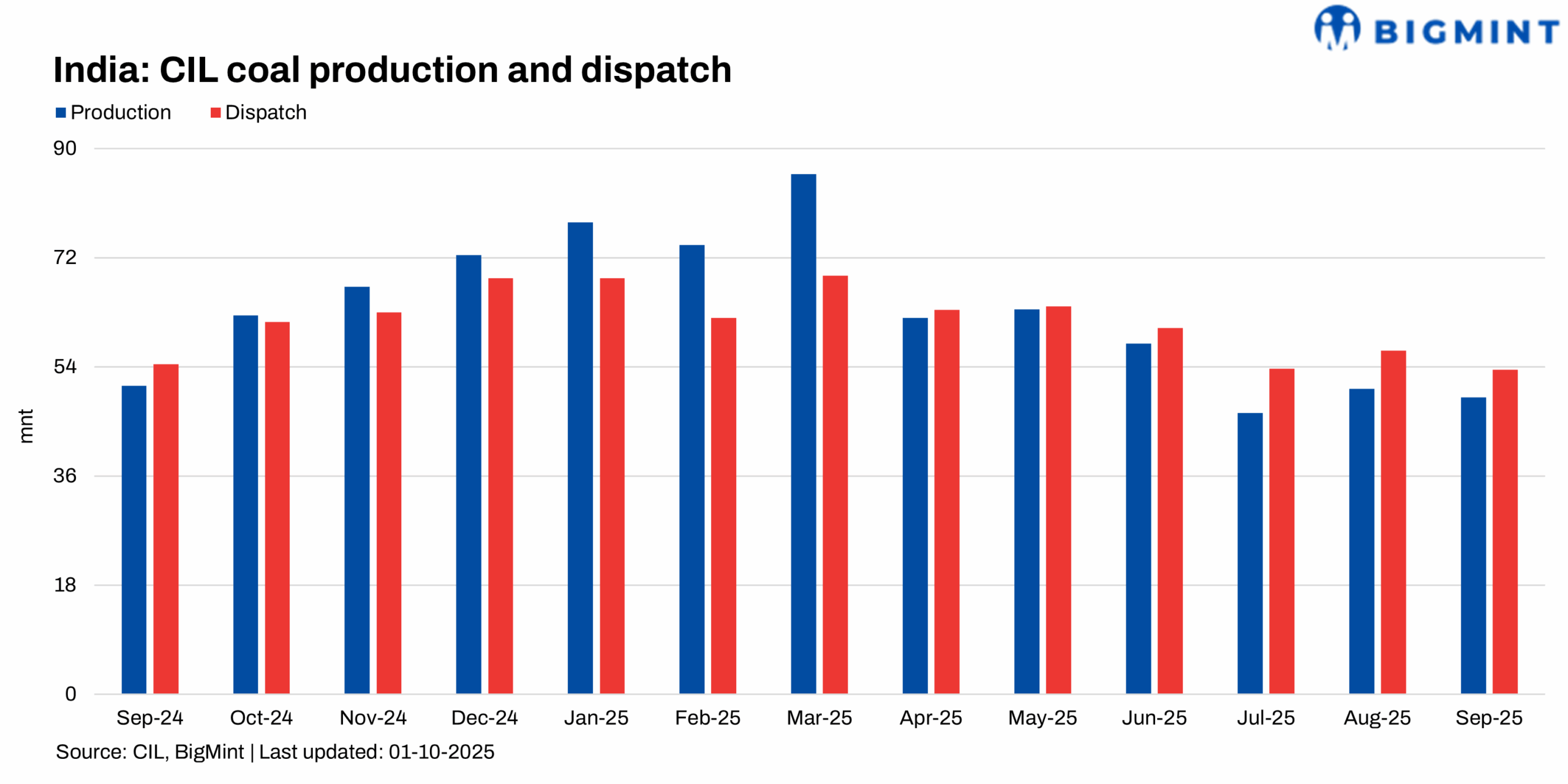

Coal India Limited (CIL), the Maharatna public sector enterprise under the Ministry of Coal, has released its provisional production and dispatch data for September 2025, along with cumulative figures for April-September 2025. The data reflects a year-on-year decline in both monthly and half-yearly volumes, highlighting persistent operational and demand-side challenges.

Production slips 3.9% in Sep’25

CIL’s coal production for September 2025 stood at 48.97 million tonnes (mnt), down 3.9% y-o-y from 50.94 mnt in September 2024. The sharpest decline came from Mahanadi Coalfields Limited (MCL), which registered a 12.8% y-o-y drop at 14.43 mnt. In contrast, Northern Coalfields Limited (NCL) and South Eastern Coalfields Limited (SECL) provided some relief with production growth of 11.3% (11.53 mnt) and 6.5% (10.75 mnt), respectively.

The uneven subsidiary performance indicates the impact of regional mining constraints, infrastructure bottlenecks, and weather-related disruptions on output.

Half-year production reflects persistent weakness

During FY’26(Apr-Sep’25, CIL’s total coal production was reported at 329.14 mnt, down 3.6% from 341.35 mnt in the same period last year. This sustained weakness highlights structural hurdles in scaling up mining operations, along with logistical challenges in ensuring consistent supply during peak demand months.

Dispatches record marginal dip in September

Coal offtake in September 2025 reached 53.56 mnt, reflecting a 1.1% decline from 54.16 mnt in September 2024. MCL led dispatches with 16.63 mnt, though down 1.4% y-o-y. Meanwhile, SECL recorded a robust 10.9% growth in dispatches at 12.08 mnt, and NCL posted a 7.3% increase to 10.91 mnt.

The divergence in subsidiary dispatches suggests that industrial demand and non-regulated sector consumption provided stability, even as power sector demand softened amid adequate stock availability at plants.

Half-year offtake contracts by 2.1%

CIL reported a total offtake of 356.16 mnt during FY’26 (Apr-Sep’25), reflecting a 2.1% decline from 363.66 mnt in the corresponding period of the previous year. The reduction was largely attributed to subdued demand from the power sector, supported by adequate plant inventories, along with weaker industrial consumption.

Outlook

CIL’s outlook is stable but demand-driven. Growth prospects rest on winter power needs and an industrial rebound, while consistent output from NCL and SECL offsets MCL’s weakness. Renewable energy expansion may cap demand, but any spike in electricity consumption or supply-chain disruption could provide short-term support.

Leave a Reply