- Pacific basin freight rates drop on fixtures at lower levels

- China’s BHP iron ore restrictions cloud outlook

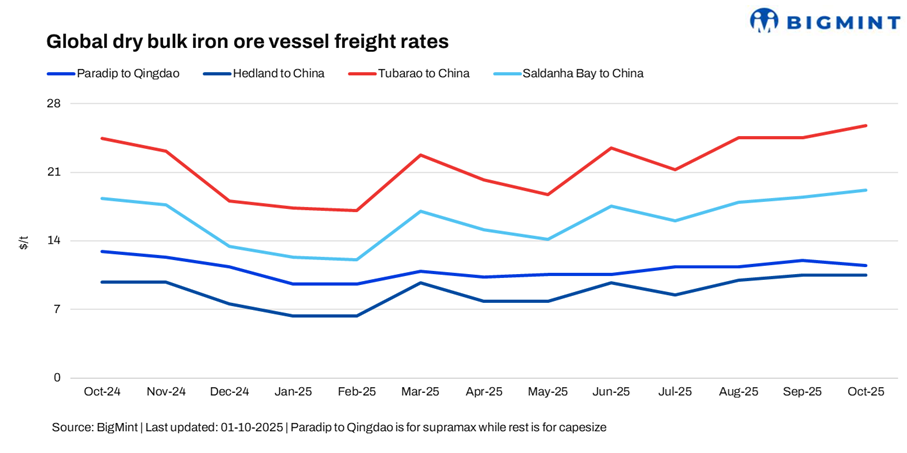

Dry bulk iron ore freight rates rose this week on the Brazil-China and South Africa-China routes, supported by a handful of fixtures from Brazil, while activity out of South Africa remained subdued. In contrast, India-China and Australia-China rates eased, with the latter seeing a sharper correction amid softer market activity compared with the previous week.

Capesize freight rates softened in the Pacific basin, as the Australia-China market faced weaker sentiment. Lower offers emerged, but demand remained limited, with scarce bidding activity observed ahead of the close of Asian trading hours. The lack of fresh fixtures highlighted cautious charterer activity and contributed to the downward pressure on rates.

Meanwhile, Supramax freight rates on the India-China route extended their decline, weighed down by market uncertainty over a potential export duty. However, some sources noted that the speculation is likely unfounded, as the duty is unlikely to be imposed.

In the Pacific, Rio Tinto was the sole major charterer active on the Australia-China iron ore route, with inquiries placed at lower freight levels.

In the Atlantic, activity stayed largely muted during Asian trading hours, particularly on the South Africa-China route where fixtures were minimal. BigMint data shows that only three fixtures were recorded on the Brazil-China lane this week.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed a w-o-w decrease of $0.25/dry metric tonne (dmt) to $11.47/dmt. India-China freight rates have come under pressure as limited iron ore export demand and uncertainty over a possible duty kept charterers cautious, while a build-up of open tonnage in Indian ports further weighed on sentiment. Softer Chinese buying interest and increased vessel availability in the region have added to the downside momentum, pushing rates lower this week.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China dropped by $0.29/dmt w-o-w to $10.50/dmt. With market fundamentals shifting in favor of buyers, bids and offers slipped to around $10.55/dmt, down from about $11/dmt at the start of the week.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments witnessed an increase of $0.4/dmt w-o-w, settling at $25.80/dmt. On the Tubarao-Qingdao route, three fixtures were reported this week at around $25.75-25.85/dmt. Brazil-China freight rates edged higher this week, supported by an improvement in fixtures that helped lift sentiment, even as overall Atlantic activity remained relatively subdued.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao followed the suit and edged higher by $0.71/dmt w-o-w, settling at $19.21/dmt. South Africa-China freight rates also inched up this week, despite the absence of fresh fixtures, reflecting lingering market optimism and tight vessel availability in the region.

Market highlights

- Baltic index hits two-week low: The Baltic Exchange’s main dry bulk sea freight index fell w-o-w on 30 September driven by drop in rates across all vessel segments. The overall index decreased around 66 points w-o-w to 2,134, with the Capesize index falling sharply by around 164 points w-o-w to 3,305. Meanwhile, the Supramax segment decreased by 13 points w-o-w to 1,473.

- DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract decreased by around RMB 23/t ($3/t) to RMB 780.5/t ($109.63/t) on 01 October, 2025. This decrease was attributed to weak manufacturing data from China, which dampened market sentiment.

- Brent crude oil futures inch down w-o-w: Brent crude oil futures fell marginally by around $0.88/barrel (bbl) w-o-w to $65.62/bbl, influenced by factors such as expectations of increased output from OPEC+, the resumption of crude oil exports from Middle East region, and concerns over tepid global demand amid economic uncertainties.

Outlook

The near-term outlook for dry bulk iron ore freight is showing a mixed and somewhat uncertain picture across key routes. On the Brazil-China, rates have stabilized supported by steady demand and fewer ballast vessels, while the South Africa-China route holds relatively steady amid balanced supply-demand dynamics. In contrast, the India-China route has seen softer rates due to limited fixtures and reduced demand, reflecting challenges that could influence broader freight market trends.

Adding to this uncertainty, as per reports, China’s state-run China Mineral Resources Group (CMRG) has reportedly instructed steelmakers and traders to pause purchases of dollar-denominated iron ore cargoes from BHP amid ongoing price negotiations. While market participants view this as a temporary negotiating tactic, the move has already disrupted markets. If the pause extends, it could create headwinds for dry bulk shipping, potentially pushing freight rates higher as buyers seek alternative sources, leaving the market closely watching developments.

Leave a Reply