India’s stainless steel flats and longs market remained muted this week, with stable price levels but persistent demand weakness across both categories.

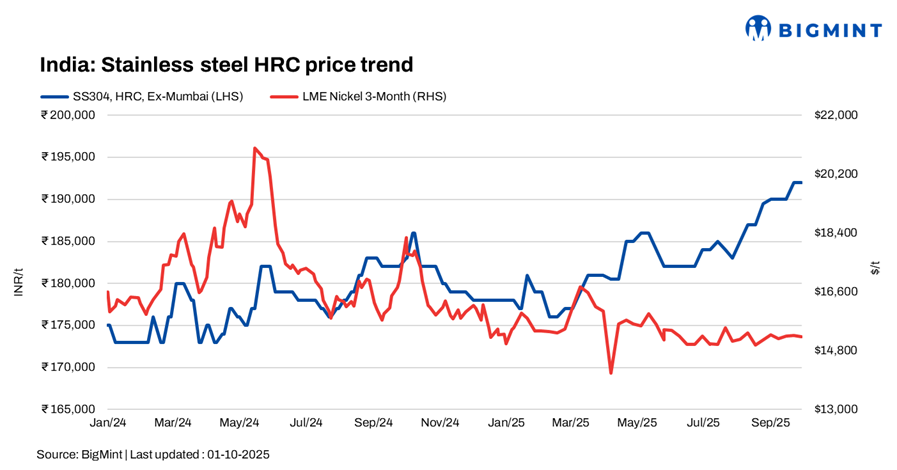

BigMint’s assessed 304-series hot rolled coils (HRCs) at INR 192,000/t ex-Mumbai, remained unchanged. While 304L black round bars (25-100mm) also remained stable stood at INR 160,000/t. In contrast, 316-series HRCs stood steady at INR 345,000/t and cold-rolled coils (CRCs) edged up by INR 1,000/t to INR 351,000/t w-o-w.

Despite this, downstream demand across utensils, cutlery, hinges, and tubes stayed weak. Non-tariff barriers in export destinations further restricted momentum, while domestically, rising prices of finished stainless steel products like pipes and tubes discouraged fresh buying.

Demand in longs segment was especially slow due to seasonal factors-monsoon disruptions, festive holidays, and the Diwali lull-limiting fresh inquiries. Export prospects for longs were also hampered, with buyers citing reduced overseas orders owing to US tariffs and ongoing currency fluctuations. Traders and mills noted that current prices were moderate but there was insufficient buying appetite to support any upward trend.

LME nickel tags remain largely stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,235/t, down slightly by $40/t compared to last week’s $15,275/t. Nickel stocks at LME-registered warehouses stood at 231,312 t, up 0.37% compared to 230,454 t t in the previous week.

Chinese stainless steel, NPI prices largely stable on the week

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,750/t ($1,931/t) exw, while FOB tags of 304-grade CRCs were firm at $1,930/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) remained firm w-o-w at RMB 955/t ($134/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $118.59/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed largely stable last week, going down slightly by INR 16,000/t ($180/t) as compared to the assessment on 24 September. Regular trades in the domestic market along with minimal market movement kept the prices steady.

Ferro molybdenum prices in India were INR 3,068,000/t ($34,602/t) exw-India, as per BigMints assessment on 1 October. Approximately 70 t of trades were reported to BigMint last week within the price range of INR 3,065,000-3,150,000/t ($34,568-35,526/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 600/t w-o-w to INR 118,700/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices stayed largely stable last week, moving down marginally by INR 100/t ($1/t) as compared to the assessment on 22 September. With the month about to conclude, the market was mostly quiet as people were looking forward to next months price announcement.

As per BigMint’s assessment on 29 September, ferro silicon prices in India were INR 88,300/t ($995/t) exw-Guwahati. In Bhutan, prices inched down by INR 400/t ($5/t) w-o-w to INR 88,000/t ($992/t) exw. With key sellers in both India and Bhutan already sold out, not many deals were concluded last week.

Ferrous scrap: India’s imported scrap market stayed subdued, with offers holding steady but failing to draw strong buying interest. Shredded scrap was quoted around $355-360/t, HMS 80:20 at $325-330/t, busheling near $370-375/t, and PNS at $365-370/t CFR. Domestic scrap remained cheaper by INR 1,500-1,800/t, further discouraging imports. Seasonal rains, sponge iron trials, and festive season slowdowns weighed on demand, while workable bids lagged below offers, keeping buyers cautious and fresh bookings limited.

Outlook

India’s stainless steel market is likely to stay under pressure in the near term, with weak domestic offtake and cautious sentiment weighing on both flats and longs. The anti-dumping investigation on flat products from China, Indonesia, and Vietnam could gradually realign trade flows, potentially offering long-term support to domestic producers. However, in the short run, uncertainty continues to dominate as muted end-use demand, subdued exports, and macro challenges-including currency volatility and global trade headwinds-keep buyers on the sidelines. Some improvement may emerge in October-November with seasonal export demand, but recovery is expected to be limited and uneven, leaving the overall outlook subdued.

Leave a Reply