- Exports drop to 0.83 mnt in Aug, lowest since Nov’22

- Weak China market fundamentals weigh on India’s exports

- Govt mulling export duty on iron ore amid shrinking domestic supplies

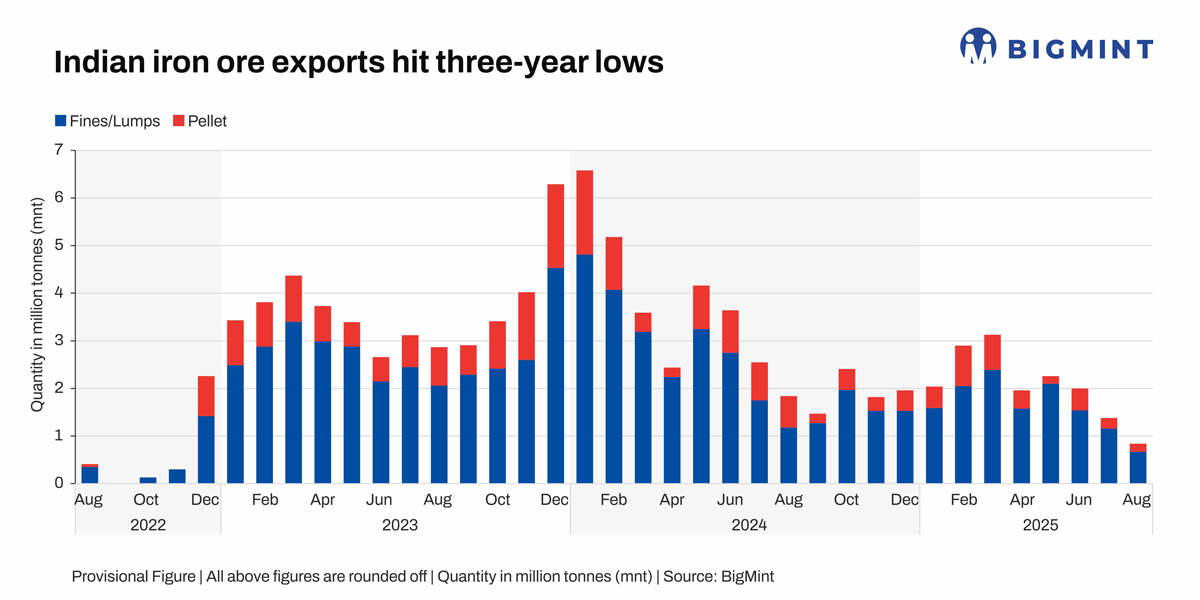

Morning Brief: India’s total exports of iron ore, both fines and lumps, and pellets were recorded at 0.83 million tonnes (mnt) in August 2025. Out of 0.83 mnt, 0.67 mnt were fines/lumps and the rest 0.17 mnt pellets.

Exports dropped to a three-year low on weak demand from China as well as supply pressure in the domestic iron ore market.

The top iron ore exporters in August were Rungta Mines, Vedanta and OCL, while the major pellet exporter was KIOCL/NMDC.

China was the largest importer at 0.54 mnt followed by Malaysia at 0.12 mnt.

Reasons behind drop in exports

- Weaker Chinese market fundamentals: After a brief uptick in July, iron ore demand in China seems to have again dissipated, with weaker steel market fundamentals weighing on iron ore demand. The ongoing summer lull in steel consumption, together with potential environmental protection measures which have led to restrictions being imposed on production took a toll on hot metal output at Chinese mills.

Moreover, China’s steel exports are expected to shrink in August, as rapid increases in steel prices last month dampened the buying appetite of some overseas buyers. Lower export orders prompted mills to make additional production cuts, further depressing iron ore demand.

- Discussions on imposing export duty on iron ore: At a recent inter-ministerial meeting in the national capital the domestic supply issue of iron ore was taken up and the government has underlined certain priorities for increasing iron ore supply. Imposition of a uniform export duty on export of iron ore across grades from 2 October’25 has been mulled if there is no increase in domestic iron ore production and subsequent decrease in iron ore prices.

It was announced in the meeting that exports of iron ore will be permitted only after ensuring domestic requirements are fully met. Non-operationalisation of most of the auctioned mines has created a supply pressure in the domestic iron ore market due to which iron ore prices have remained firm over the past year even though steel prices have slackened.

- Drop in iron ore production: India’s iron ore production fell to the lowest point in a year in July’25 at 18.7 mnt due to heavy monsoon showers disrupting production and dispatches, railway movement and overall logistics. Lower domestic production and logistical disruptions discouraged exports.

- Domestic pellet realisations higher than exports: Major producers who were once active in the export segment have shifted their focus towards domestic sales due to stronger realisations and widening bid-offer gaps in the export market.

As per BigMint’s assessment in the first week of September, domestic prices exceeded export offers by around INR 1,750/t ($19/t). Fe 63% pellet prices in Odisha’s Barbil were recorded at INR 8,350/t ($95/t) exw. Meanwhile, ex-plant realisations in exports from Barbil were at INR 6,600/t ($75/t) exw.

Outlook

Undoubtedly, the biggest threat to India’s iron ore export prospects comes from China where weakening demand may lead to mounting steel stocks while no production cuts are mandated by the central government authorities, causing the ferrous market to nosedive. Although such a situation seems unlikely, weak demand from China seems to have become the new normal.

Another threat is, of course, the potential export duty on iron ore which, if implemented, will surely have the same impact as in 2022 when the government had imposed duty across iron ore grades, as well as on pellet exports. With domestic supply tightening, such a prospect doesn’t look unlikely.

Leave a Reply