- Steel prices face pressure, weigh on coking coal tags

- Improved supply may lead to further price corrections

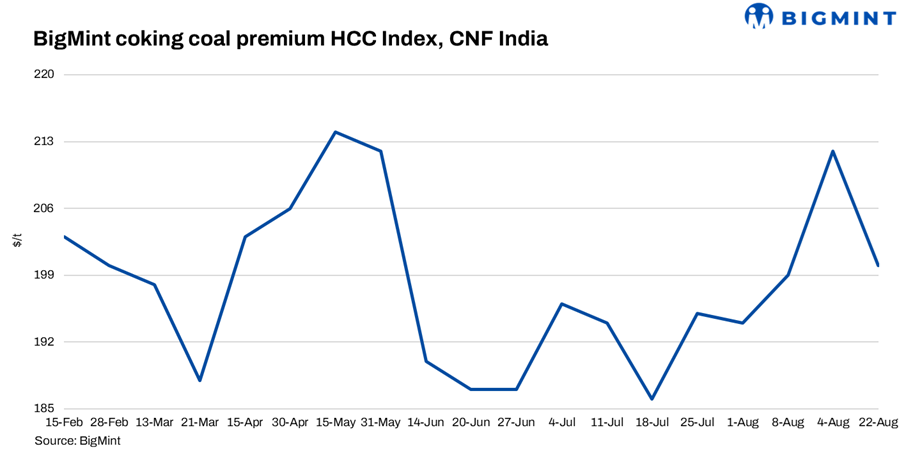

BigMint’s premium hard coking coal (PHCC) index was assessed at $200/tonne (t) CNF Paradip, India, on 22 August 2025, down by $12/t against the previous assessment on 14 August 2025.

Prices showed signs of easing, with expectations of further softening driven by improved availability. Offers for Australian-origin material were at around $205-210/t CFR India, though buyer interest appeared limited. Bids emerged on the lower end, possibly in the $198-200/t CFR India range, reflecting subdued demand.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

No deal was recorded during the publishing window. Hence, it was considered for index computation and given a weightage of 0%.

Eight (8) firm offers, bids, and indicative prices were heard. Out of these, six (6) were considered for price calculation and given 100% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Indian met coke prices hold steady w-o-w amid tight supply: The Indian metallurgical coke (met coke) market remained stable w-o-w during the week ending 22 August 2025, supported by constrained domestic availability and firm input costs.

In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 29,000/t ex-Jajpur, while in western India, ex-works Gandhidham prices held at INR 30,000/t. Market activity was largely steady, with trades beginning to pick up as consumers sought to secure volumes in expectations of limited supply in the near term.

2. Chinese met coke prices rise further: Regional met coke sentiment was also shaped by developments in China, the world’s largest coke consumer. On 20 August, Chinese producers attempted to implement a seventh consecutive round of price hikes, but steel mills showed resistance amid stable supply, adequate inventories, and weak finished steel margins.

Demand for coke remained underpinned by steady molten iron output, though procurement stayed cautious. Meanwhile, coking coal markets in China displayed mixed trends: gas coal prices in Shaanxi softened on weak buying, while a mine accident in Shanxi curtailed high-sulphur coal output, tightening supply and lending localised price support.

3. Indian steel prices remain under pressure: India’s trade-level blast furnace (BF) rebar prices declined w-o-w across major domestic markets amid a demand slowdown due to rains. Some primary mills reduced rebar list prices by INR 1,000/t ($12/t), while others offered discounts due to slow lifting of material.

Trade-level BF rebar prices dropped by INR 500/t ($6/t) w-o-w to INR 47,900/t ($548/t) exy-Mumbai, as per BigMint’s assessment on 22 August 2025. Prices are exclusive of GST at 18%.

Meanwhile, trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w at INR 49,500-51,200/t ($568-588/t). Moreover, cold-rolled coil (CRC) prices were stable w-o-w, ranging within INR 55,200-59,100/t ($634-679/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) held stable w-o-w at INR 50,000/t ($574/t) on 19 August 2025.

Leave a Reply