- South African coal offers rise

- Domestic coal prices show mixed trends

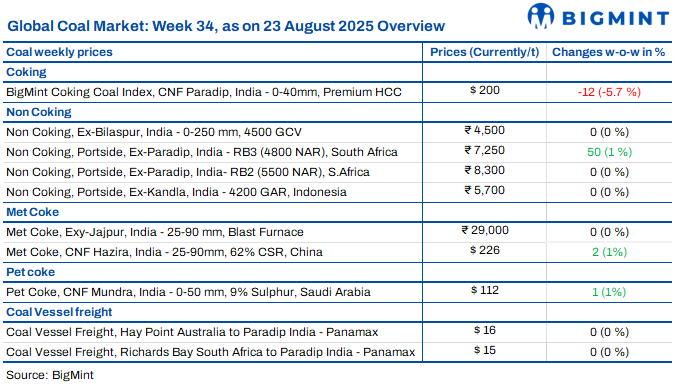

The Indian coal market remained largely stable this week, with prices edging higher in some segments due to firm freight rates and supply disruptions. Domestic coal saw mixed trends, while imported South African and Indonesian offers were supported by freight firmness despite weak demand. Coking coal prices softened on bid-offer gaps, though met coke held steady on tight supply. Overall, muted industrial activity and seasonal monsoon disruptions kept trading sentiment cautious.

Indonesian coal prices steady amid need-based demand

Portside Indonesian thermal coal prices in India stayed flat w-o-w in the week ending 22 Aug. BigMint assessed 5000 GAR at INR 7,150/t (Kandla) and INR 7,050/t (Vizag), while 4200 GAR held at INR 5,700/t and INR 5,600/t, respectively. The 3400 GAR grade at Navlakhi remained at INR 4,450/t. Need-based buying prevailed, as power plants maintained 51.89 mnt of stocks, sufficient for 17 days, though

South African coal offers rise, demand muted

South African coal prices in India moved slightly higher this week, with RB2 assessed at INR 8,300/t exw-Gangavaram, up INR 50/t, while RB3 increased INR 100/t to INR 7,200/t. Eastern port RB2 offers were heard at INR 8,300-8,350/t, but buyers stayed cautious as high levels restricted trades. Portside stocks rose 1.2% w-o-w to 13.86 mnt. Sponge iron demand stayed weak, with BigMint’s C-DRI index easing INR 200/t to INR 25,900/t. Export offers also edged up, RB2 at $74/t and RB3 at $62/t FOB.

Domestic coal prices steady amid mixed movements

Domestic coal prices in India showed mixed trends this week. BigMint assessed 5000 GCV at INR 5,250/t exw-Bilaspur, up INR 250/t w-o-w, while 4500 GCV stayed unchanged at INR 4,500/t. The rise in 5000 GCV was mainly due to mining disruptions during monsoon, while improving steel demand added support. Overall, sentiment stayed firm with the market expecting stability in the near term. SECL will auction 338,000 t on 23 August and 141,950 t on 28 August covering grades G6, G7, G8, G9, and G11.

BigMint’s PHCC index falls as bids stay weak

BigMint’s premium hard coking coal (PHCC) index was assessed at $200/t CNF Paradip on 22 August, down $12/t w-o-w. Offers for Australian coal stood at $205-210/t CFR India, but bids stayed lower at $198-200/t, reflecting subdued demand. Chinese coke hikes faced resistance, while Indian steel prices weakened, with BF rebar down INR 500/t to INR 47,900/t ex-Mumbai.

Met coke prices stable as tight supply offsets weak steel

Met coke prices in India stayed steady this week, with BF-grade (25-90 mm) assessed at INR 29,000/t ex-Jajpur and INR 30,000/t ex-Gandhidham. Tight domestic supply and firm coking coal costs supported stability, as Australian premium HCC edged up $3/t w-o-w to $188/t. However, weak pig iron and steel margins capped upside, leaving the market range-bound despite some pick up in trade activity.

Imported pet coke offers inch higher, trades limited

Imported pet coke offers in India edged up by about $1/t w-o-w, with US-origin at $114-115.5/t CFR India and Saudi-origin at $112-114/t, leaving both origins nearly aligned. The uptick followed firm vessel freights, but no trades materialised as buyers avoided high levels and awaited price stability. Demand is expected to recover gradually after the monsoon, supported by infrastructure activity resuming from October.

India’s dry bulk coal freights steady despite muted activity

Coal freights to India held steady w-o-w on key routes from Australia, South Africa, and Indonesia, though fixture activity stayed limited. Vessel demand remained weak as most Pacific cargoes had forward loadings and not for prompt shipment, keeping charterers cautious. Heavy monsoons also slowed port operations and dampened coal demand. Panamax rates stood at $16/dmt from Hay Point-Paradip and $15/dmt from Richards Bay-Paradip, while Supramax freights from East Kalimantan-Navlakhi stayed at $15.93/dmt. India’s portside stocks rose 1.2% to 13.86 mnt in Week 33.

Leave a Reply